The evolution of digitalization is changing how multinationals operate and relate with foreign governments. It is raising questions about taxation in the digital economy. There have been debates over the last few years about how the standard international tax system needs to properly capture the expanding reach of digitalization.

Hitherto, big tech firms like Netflix, Meta, Google, Microsoft, Spotify and a host of others did not pay taxes on revenues earned in countries other than the home country – typically the United States (US). This is so because, under the standard international tax rule, multinational firms paid corporate income taxes where production takes place (rather than where consumption occurs) or where there is a physical presence.

But the amount of revenue generated by these multinational companies leveraging digital technologies and platforms has shown that value can be created with little or no physical presence as long as there are consumers for these services. This scenario entitles foreign governments to impose varying taxes on revenues drawn by multinational companies from local consumers.

To address these concerns, the Organisation for Economic Co-operation and Development (OECD) and the G20 Inclusive Framework developed a two-pillar solution to settle the inherent challenges of taxation in the digital economy. Twenty-three African countries were part of the 136 countries worldwide that met to discuss the global tax reforms.

Pillar 1 focuses on the reallocation of (a portion of) the consolidated profit of a multinational enterprise to jurisdictions where sales arise as well as the standardization of the remuneration of routine marketing and distribution activities. By changing where/how companies pay taxes, Pillar 1 essentially expands a country’s authority to impose taxes on the profits of non-resident companies that make sales from local consumers in the country.

Effectively, more countries all over the world have imposed and are implementing value-added tax (VAT) and other service-level taxation on digital products and services. In 2019, the Minister for Finance in France, Bruno Le Maire approved a digital services tax (DST) of 3% on intermediary services and advertising services based on users’ data. The United Kingdom imposed a DST of 2%, while Italy and Spain imposed a DST of 3% among other countries in Europe. Some other countries like Slovakia, and Turkey applied withholding tax (WHT) of 5% and 15% respectively.

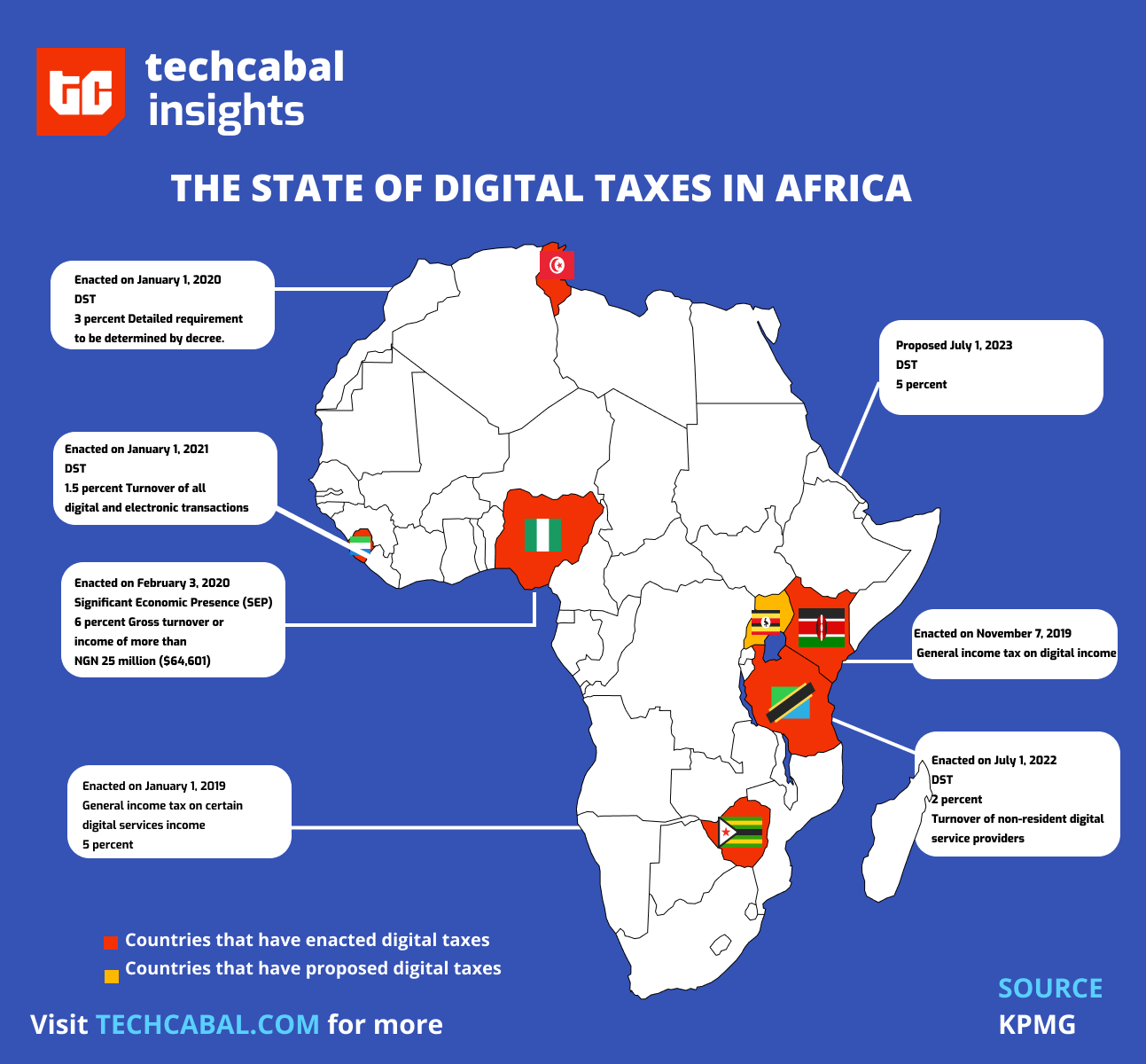

In Africa, DST has also been applied to revenues generated by digital services companies in market jurisdictions. In Nigeria, the Finance Act 2021 introduced a six (6%) digital service tax on non-resident companies with a significant economic presence estimated to be N25 million ($54,230) in annual revenue. Other African countries that imposed some form of taxes on digital services provided by non-resident companies include Zimbabwe (5%), Tunisia (3%), and Tanzania (2%); Sierra Leone and Kenya have DST of 1.5%. The latest is Uganda which proposed a DST of 5% to take effect in July 2023.

This map reports only DST. Even more countries have imposed VAT on digital services

Nonetheless, the varying rate of taxes across markets and the concentration of multinational companies in the United States implies that it would bear most of the taxes of digital service export. This scenario could have implications for retaliatory taxation and trade wars.

For instance, the United States Trade Representative (USTR) responded to France’s imposition of DST by proposing tariffs of up to 100% on certain French exports to the US, citing discriminatory practices against US-based digital service companies. France eventually suspended the collection of DST revenue.

Given the issues generated by DSTs, it became pertinent to review how the digital economy is taxed and work towards a fairer tax rule. As Pillar 1 focuses on changing where multinational companies are taxed (considering consumer location), Pillar 2 introduces a global minimum tax of Effective Tax Rate (ETR) through a system where multinational companies with consolidated revenue over €750m are subject to a minimum ETR of 15% on income arising in low-tax jurisdictions. Both Pillars 1 and 2 are of the OECD/G20 Inclusive Framework of Base Erosion and Profit Shifting (BEPS) 2.0 to address the tax challenges of the digital economy.

Pillar 2, also known as the Global Anti-Base Erosion Rules (GLoBE), streamlines international taxes rules to ensure that large multinational companies pay a minimum tax (of 15%) on the income arising in the jurisdiction where they operate. The OECD has recommended that the Pillar Two rules become effective in 2024, except the Undertaxed Profits Rule (UTPR) recommended to become effective in 2025. The UTPR allows a country to increase taxes on a business if that business is part of a larger company that pays less than the proposed global minimum tax of 15% in another jurisdiction.

According to the initial analysis of the original proposals, Pillar 1 and Pillar 2 would increase the effective average tax rate by around 0.7% across all jurisdictions. Pillar 1 is responsible for only 0.1% of this increase. So far, about 138 countries have signed up to be Pillar 2 compliant as of December 2022.

The Africa case: Spotlight on Kenya, Nigeria, and Uganda

Nonetheless, African countries have not entirely bought into the Two-Pillar framework. Though some African countries have segued to the idea of a framework, many are yet to join or enact domestic laws that are consistent with the BEPS 2.0 initiative.

Nigeria is one of four countries (Kenya, Pakistan and Sri Lanka) that did not endorse the agreement in October 2021. This article cites complex compliance frameworks and the high cost of implementation as some of the reasons the Nigerian government is sceptical about joining the agreement. In 2022, the Nigerian government enacted a DST of 6% on large corporations with significant economic presence.

In the first week of April 2023, the OECD sent a delegation to meet with representatives of the Nigerian government from the Federal Inland Revenue Service (FIRS) to discuss the maximization of the benefits of the framework for Nigeria and the need for Nigeria’s continued participation in developing the rules.

Interestingly, Kenyan President, William Ruto announced that Kenya will withdraw its objection to the OECD Pillar Two framework, and repeal the DST of 1.5% to align with the OECD framework. Uganda, on the other hand, recently proposed a DST of 5% on digital services of non-resident companies providing services in the country. Though this proposal was rejected by the members of parliament in May 2023, it did not seem like the argument was to align with the global minimum ETR.

In summary, whether the global minimum tax rate of 15% on digital services increases in many African countries is yet to be determined. It would depend on the number of multinational corporations in the country and the revenue derived from digital services consumers in the market jurisdictions. A global consensus on minimum tax on digital services would not crowd-out investments in Africa’s growing digital economy any more than would a national DST.