First published 17 September 2023

Smallscale modern retail in Africa will not completely replace open markets in Lagos, souks in Cairo, or storied markets like Karatina in central Kenya. But a subtle shift that can become a major marker of African retail is underway.

Warning. Long read ahead. Please find a comfy seat, some coffee and relaxing music. It’s Sunday after all!

The more I read the news, interact with people, and think through how urban food systems are organised, the more I realise how much Africa’s retail scene needs to defragment. Defragmentation means support for scale and efficiency. It also means that retail is then organised in a less chaotic manner. But it does not necessarily mean complete defragmentation à la the mall and retail industry structure of America. Japan has a high density of neighbourhood shops, but it also boasts one of Asia’s strongest modern retail markets, with everything from à la carte malls to specialty luxury shopping outlets. In many African countries, retail is beginning to take the same contours, but cheaper, of course.

Consultancies, enthusiastic entrepreneurs, freshly minted marketing executives and the big shots of African retail have expected or prophesied the coming of modern retail to Africa’s consumption habits. The consequent impact of an Africa with more modern retail is not a new conversation. What is clear after every round of discussion on modern retail in Africa is that the continent remains a tough place to run retail businesses, declining incomes are a challenge, and, as a result, the open market remains the strongest competitor.

It is true that the open market will remain a competitor for the foreseeable future. It is among other things, a cultural relic. It is also an economic mainstay that packs more economic punch than appearances suggest. But alongside the open market, African neighbourhoods are seeing the rise of modern retail channels. Branded multi-store retailers and single-store supermarkets are popping up all over towns, cities and villages. Most are just bigger versions of the regular convenience stores, and even the big malls are small compared to peers in developed countries. But I believe we are in the early stages of a modern retail boom, and the wave is slowly building up.

The first stages of a wave

Ripples on the Lifjord lake in in Øksnes, Norway. Photo by Blue Elf via Wikimedia Commons

When a light breeze blows across a smooth lake or ocean expanse, it creates small ripples that are called capillary waves. These ripples are the first stage of wave generation. As the ripples get larger, the wind is better able to “grip” it in a self-sustaining cycle that creates even bigger waves. These waves can become stronger the longer they travel over the ocean. Then they become groundswells—the type of waves that ocean surfers love because they are even spaced and powerful enough to ride. That initial capillary wave action is where Africa’s modern retail is at in several countries.

Excluding South Africa, this wave of modern retail across Africa looks just like how any other wave does, i.e. it is undulating, and not a smooth upswell across the continent. But it is definitely there and building up.

Because Next Wave is a pan-African business and tech commentary and not a country-by-country level research paper, our discussion will remain at the continental macro-level. I will leave you, the reader, to do the country analysis. If however, a lot of readers indicate a strong demand for country-by-country examples, I might be persuaded to highlight a few countries in a subsequent essay.

Loosely speaking the economics of retail is driven by aggregation. B2B, B2C, B2B2C ecommerce companies try to aggregate shoppers either directly or through retail points. FMCG manufacturers aggregate through distributors. And even savvy street corner shops try to aggregate the best and most recurring daily shoppers. The fewer the points that tie demand together into an efficient logistics chain, the better for manufacturers and sellers. Consumers however want convenience and worry about pricing. In our continent, with low purchasing power, low consumerism and high unemployment, a disjointed last-mile for consumer goods emerged to serve two needs. Get stuff to people in small packets, and create low-wage jobs. The result is aggregation upstream at the manufacturing level. And heavy fragmentation at the distribution level. Consumer goods makers, for example, can simply rely on large distribution operations in key locations. The distributors (digital or non-digital) move the goods downwards through whatever works—wholesalers, sales staff or road hawkers. This aggregation of chaos has somehow worked long enough that everyone has learned to respect the African traditional retail market.

And with good reason. FMCG players see no need to do the work (and face the economic consequence) of organising a consolidated retail market, and hence supply chain. Distributors are too busy moving goods at tiny margins and small commissions, and the capital requirements to build modern retail consolidation do not square with the economic realities in many African countries. There is simply little incentive to create formal modern retail and risk disturbing the waters of consumer trade too much.

But like I said, modern retail (with African characteristics) is happening anyway. It is not even across the continent. And it comes in different colours.

Modern retail in Africa is local and neo urbanist

Japan is one of the world’s largest retail markets with a strong large modern retailing sector with huge malls and millions of square feet of luxury shopping centers. But it is also host to exciting street markets and smaller modern retail outlets (both chain supermarkets and single store outlets). Japan’s konbini are small supermarkets that are open 24 hours every day of the week. They are a cultural and consumer staple in the Asian nation and play an important role in Japan’s retail market.

In many areas, Japan and African countries are poles apart, but Africa’s small but quickly growing modern retail market may just look more like Japan’s retail sector than Europe or the United States. That is, a mix of the traditional open market, dense street corner shops, and importantly, a bustling modern retail segment dominated by supermarkets.

The urban population boom in Africa is partly responsible. Aong with all the challenges it comes with, there are also tough opportunities in tow. Howard French describes the scale of this population growth better:

There is one place above all that should be seen as the centre of this urban transformation. It is a stretch of coastal west Africa that begins in the west with Abidjan, the economic capital of Ivory Coast, and extends 600 miles east – passing through the countries of Ghana, Togo and Benin – before finally arriving at Lagos. Recently, this has come to be seen by many experts as the world’s most rapidly urbanising region, a “megalopolis” in the making – that is, a large and densely clustered group of metropolitan centres. When its population surpassed 10 million people in the 1950s, the New York metropolitan area became the anchor of one of the first urban zones to be described this way – a region of almost continuous dense habitation that stretches 400 miles from Washington DC to Boston. Other regions, such as Japan’s Tokyo-Osaka corridor, soon gained the same distinction, and were later joined by other gigantic clusters in India, China and Europe.

Heavily populated metropolises do not in themselves mean the take off of modern retail. But they certainly do make it more likely.

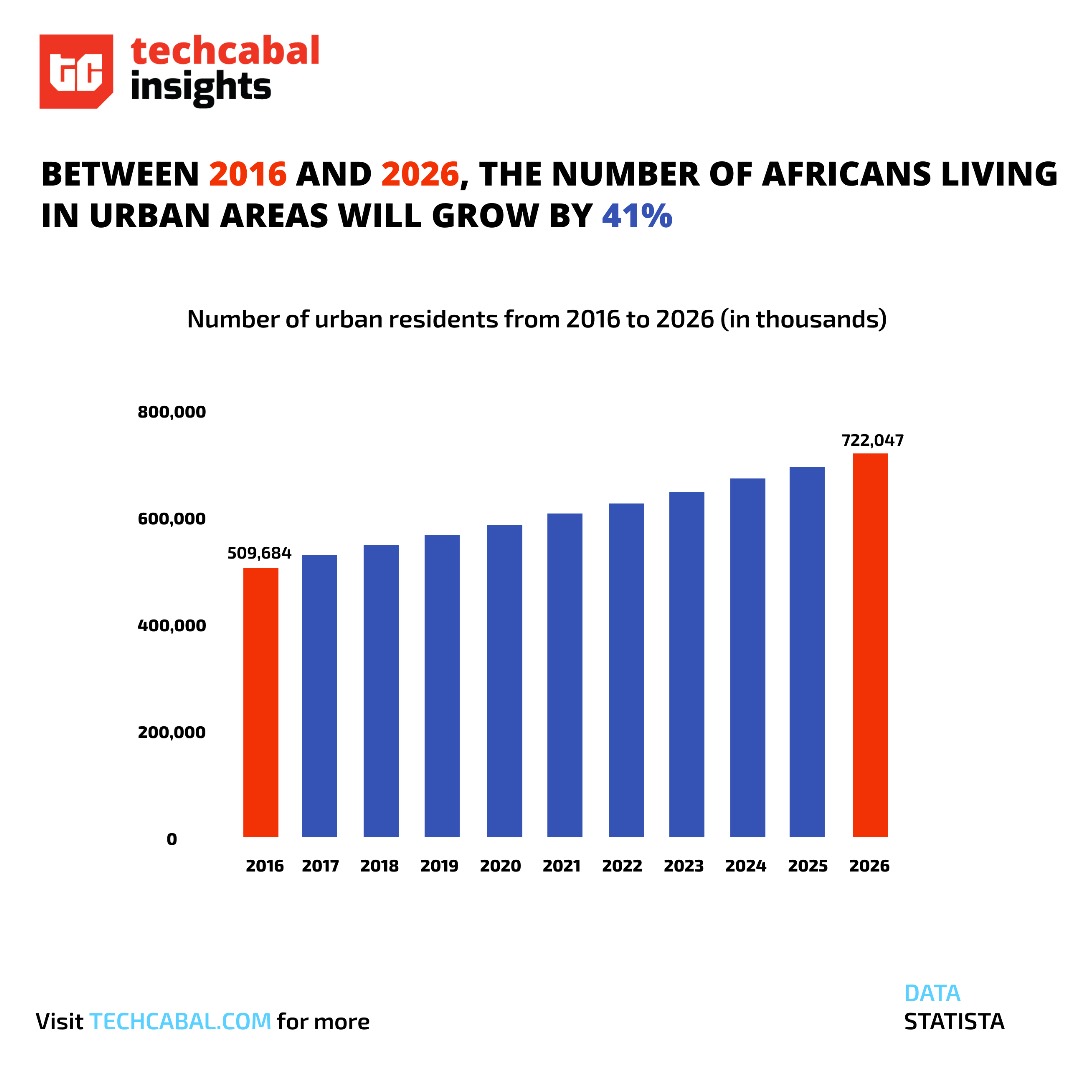

A growing population presents new (read: old i.e wellknown) sets of challenges. But also opportunities. | Chart by Mobolaji Adebayo, TC Insights

Besides population growth, the need for convenience and a growing class of working professionals that demand hassle free shopping is perhaps another reason why the modern retail that is beginning to take shape is local. People may not have time to officially “go shopping” but they also need to quickly pick out some items and want better or more exotic selections than what is available in the street shop beside the house. Retail has always been local, but the new explosion of supermarkets—some with or near other social spaces like restaurants are a notch more sophisticated than quick convenience stores.

And while they are not quite the public squares, they also quickly become a defining feature of the town. You see this in how Quickmart is opening its malls across Kenya. And how Nigeria’s Sundry Markets is spawning MarketSquare supermarkets across the country. You also see it in Zimbabwe’s thriving modern retail space and how the OGs like OK Zimbabwe that have held the fort for decades are beginning to finally expand outside of Harare—after 80 years of existence!

Partner Content:

Tap into the future of contactless payments with Swwipe

Modern retail in Africa is branded

For the better part of the last decade, Port Harcourt’s (a city in southern Nigeria) most popular local tourist attraction was a mall. I’ve been told it’s the same in some Abuja malls, especially during religious festivals. People love when modern retail comes to town. It is a treat. What is worth noting is that the emergence of smaller, well run and organised supermarkets, and small malls is still treated as an experience by locals.

Port Harcourt’s Spar mall is part of the Dutch international retail franchise. It’s popularity as a local attraction has waned. Maybe partly due to controls on non-shopping visits. But in my book, part of this is due to the emergence of more local and accessible options that deliver a lite-version of the mall-going experience, but as a supermarket. And because they are supermarkets, not malls, vistors are more likely to be shoppers than sight seers. And Nigeria is not even a big part of where this supermarket wave is building up from

Article continues after this ad

By saying “modern retail is branded,” I mean that it is not just no-brand small-time convenience stores that are rapidly growing, but local branded options are coming into the game and presenting an opportunity for their communities to experience more options, less hassle and the warm fuzzy feeling of “going shopping.”

It is a similar story in north Africa. The big malls in Cairo, Alexandria, Rabat, Casablanca, and Tangiers are not the only places seeing positive if variable growth. Small convenience stores in small towns and sections of the big cities are having their own growth stories too and even managing to attract malls to these outskirts.

Modern retail in Africa needs technology

SurpriseI Surprise!! Of course not. No surprises there. Everyone knows commerce of any sort needs technology. Fintechs are beginning to focus on brick-and-mortar merchant payment processing as consumer payment growth slows.

But the technology modern retail needs is more than just shopping your PoS system around. And it doesn’t have to be “e-commerce tech” even though that is an expanding segment. Instead the growth of Africa’s modern retail sector may hold pockets of opportunities to help with simple modular systems that simplify backroom operations and ERP systems. It is not the most attractive startuppy thing to do. The small modern retailers do not want a lot of overhead and complex systems. And solving their problems means immersing yourself in the chaotic world of African retail, not just to sell a few contracts. But to sell standardisation. People are already taking early notice of the growing pockets of opportunity here as the ripple of Africa’s evolving modern retail spreads out.

This is the koko of the matter. The inspiration for today’s long Next Wave was this Victor Asemota tweet (see embed below), my hastly typed quote tweet of it, and his reply here, of this opportunity for simple, user friendly and modular software for this class of modern retail.

While very few are getting YC/VC money to execute ideas, there are many still hustling in the streets to build and implement payroll or inventory management for that Supermarket, SME, or factory. Standardization and scale in enterprise have not reached most African streets yet.

— Osaretin Victor Asemota (@asemota) September 14, 2023

Everything said earlier boils down to this. That Modern retail in Africa will not look like the highway malls of the US. That it also will not forever be the super fragmented dukas, spazas, and ojas that B2B ecommerce mostly currently targets. And that for these smaller modern retail outlets caught in between the need to be efficient and not being big enough to handle complex ERP systems among other troubles, a skilled entrepreneur might find space to build strong businesses. Whether it is venture scalable is another matter outside the scope of this essay.

“Beware the turbulent eddies!” Or nothing is guaranteed

If we are in the initial stages of modern retail formation across Africa (excluding South Africa) that is something to be excited for and keep watch to see and guide how it shapes up in the long run. As capillary waves travel they form turbulent eddies—also called gravity waves. These waves develop private vortices as they get bigger and gravity becomes the main driver of the wave motion instead of wind. Eventually, the wind and gravity start working together and the energy of the wind is limited or white capped.

An African vision for modern retail that brings the benefit of consolidation and efficiency while retaining the magic of corner shops and open markets will need a lot of help. Especially at the level of organised local government provision of infrastructure and streamlining oversight (not through thugs). This early stage is a perfect opportunity to bring intentionality both as an industry, and in policymaking. It does not necessarily mean new laws. Consumer retail is a notoriously organic space. But it will benefit from a government that understands urban organisation and a recognition—from all stakeholders—of what is possible with more modern retail. As much as I may want it, that the modern retail this essay describes will inevitably become a feature of retail across much of Africa is not guaranteed.

Abraham Augustine,

Senior Reporter, TechCabal.

We’d love to hear from you

Psst! Down here!

Thanks for reading today’s Next Wave. Please share. Or subscribe if someone shared it to you here for free to get fresh perspectives on the progress of digital innovation in Africa every Sunday.

As always feel free to email a reply or response to this essay. I enjoy reading those emails a lot.

TC Daily newsletter is out daily (Mon – Fri) brief of all the technology and business stories you need to know. Get it in your inbox each weekday at 7 AM (WAT).

Follow TechCabal on Twitter, Instagram, Facebook, and LinkedIn to stay engaged in our real-time conversations on tech and innovation in Africa.

|

|

|

|

|

18, Nnobi Street, Surulere, Lagos, Nigeria |

View in Map |

| You received this email because you signed up on our website or made purchase from us.If you know longer wish to recieve these emails, please unsubscribe |

{kind=link}