Back in April 2024, the Central Bank of Nigeria (CBN) directed certain fintechs to halt onboarding new customers due to what was perceived as lax Know Your Customer (KYC) efforts. This came as a surprise to many, as KYC has been a high priority across fintechs of all sizes in recent years. Yet, it appears that this effort is not sufficient.

As technology and financial innovation continue to evolve, compliance requirements are becoming increasingly complex. Financial institutions need to adapt to these changes because it’s clear that compliance expectations will grow alongside technological advancements.

Let’s break down some of the current elements that underpin transactions:

- Government Databases: Key identifiers like BVN (Bank Verification Number) and NIN (National Identification Number) are integral to KYC processes. These databases should, in theory, support robust KYC practices and help mitigate fraud.

- Rule-Based Systems: These systems, designed to flag potentially fraudulent transactions, have long been in place. However, they are typically instruction-based and may lack the flexibility required to adapt to today’s rapidly changing transaction landscape.

The downside to these measures is twofold: First, they often fall short of the dynamism needed to keep pace with evolving transaction patterns. Second, there is lack of a mechanism to ensure they consistently align with compliance standards, especially in situations like chargeback resolutions, where additional oversight may be required.

Reports shows how fintechs have increased their compliance manpower to stay compliant, However, the question remains, will increased manpower alone ever be enough to handle the continually evolving compliance landscape?

What we can do differently?

To truly address these challenges, we need to reimagine the compliance approach not simply by increasing resources, but by building a smarter, more holistic system where compliance functions as an integral arm of operations.

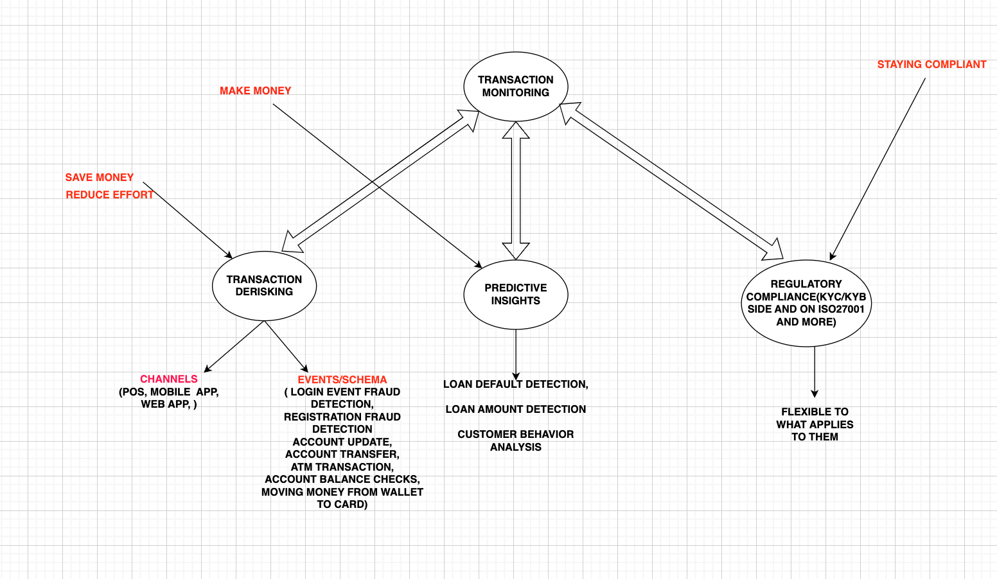

In the chart below, you can see the different components of this system, with compliance seamlessly integrated to support and enhance each function. Now, let’s break down these components in detail:

Transaction Monitoring: By combining KYC and rule-based systems, transaction monitoring can evolve into a real-time, proactive approach. This system would operate across all channels (e.g., mobile, web, ATM), triggering KYC checks not only at onboarding but also throughout each transaction where verification may be necessary. This makes KYC an ongoing process rather than a one-time event, ensuring continuous protection.

Transaction Derisking: With extended, instance-based KYC, the potential to proactively de-risk transactions grows. Continuous monitoring and verification at critical points within each transaction lifecycle could substantially reduce fraud and improve customer safety.

Predictive Insights: To keep up with evolving customer behavior, artificial intelligence (AI) is essential. Rather than relying solely on pre-trained models, AI systems can use self-learning algorithms that adapt in real time as customer patterns change.

Customer behavior isn’t static, why should their models be? – Bolu Ashimolowo COO Autogon AI

Regulatory Compliance Tracking: A dedicated compliance monitoring arm ensures that your business remains compliant with all regulatory requirements. This structure should be flexible, accommodating any changes in regulatory standards as compliance strength grows also as the authority roll out more compliance rules. In each de-risking instance, compliance reports should be generated, providing evidence of due diligence if authorities require it.

By embracing this integrated, four-pronged approach—continuous transaction monitoring, proactive derisking, AI-powered predictive insights, and dedicated compliance oversight—fintechs can create a resilient and responsive compliance framework. This approach not only meets today’s regulatory demands, but also positions fintechs to adapt as regulatory landscapes evolve, fostering both regulatory confidence and customer trust.

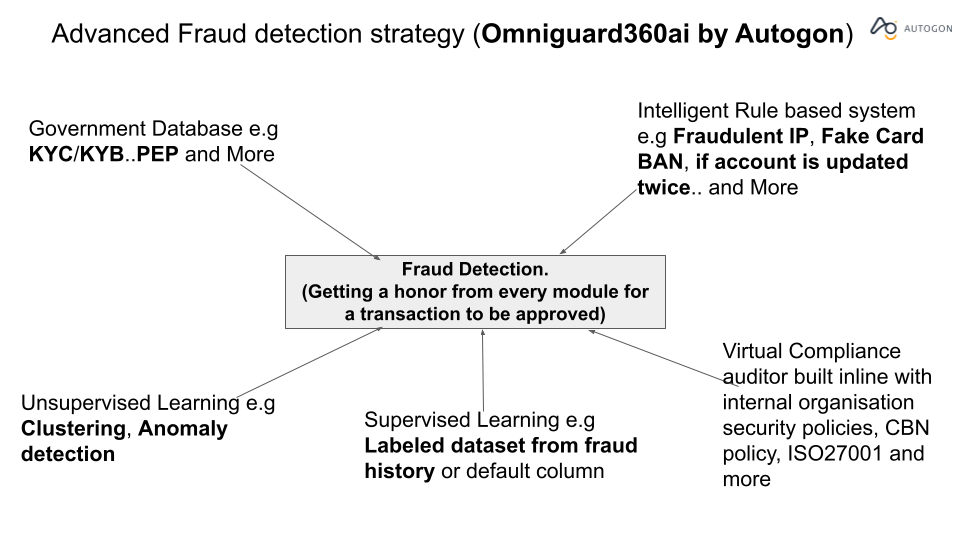

Omniguard 360 in the mix

Omniguard 360 is an advanced AI-powered transaction monitoring system designed to seamlessly integrate all critical components of an effective compliance strategy. From real-time transaction monitoring and derisking measures to predictive, self-learning AI insights, Omniguard 360 sets a new standard for transaction monitoring systems in line with compliance.

One standout feature is its persona report, which provides detailed insights for each transaction. This report aligns with compliance standards across various transaction levels, making Omniguard 360 a game changer in the realm of compliance and risk management.

Omniguard 360 empowers fintechs and corporate banks to meet and surpass compliance expectations by offering a dynamic, all-encompassing approach. It ensures your business remains protected and in alignment with evolving regulatory standards.

To learn more about how Omniguard 360 visit : Omniguard 360.