This guest post was contributed by Lavanya Anand, principal at VestedWorld, an early-stage investment fund manager.

Packing suitcases full of Amazon products on every trip to the continent. Working with Somali companies in Kenya to import Amazon products on a pay-per-kg basis. Buying and selling second-hand products on online marketplaces and informal markets. Wondering if Jumia or Jiji is going to deliver what they promised this time. Waiting in traffic or long lines at supermarkets like Carrefour. This is the reality for many middle- and high-income consumers in Africa.

As a result, we’ve been patiently waiting for the entrance of the e-commerce giant Amazon to disrupt the retail sector in Africa. They’ve already dipped their toes with their AWS data centre infrastructure in South Africa and the acquisition of the Souq online marketplace in Egypt over the past few years. However, recently, they finally announced their plans to enter the Nigeria and South Africa markets with their core marketplace offering during 2023. The big question is will it be successful and, if yes, how?

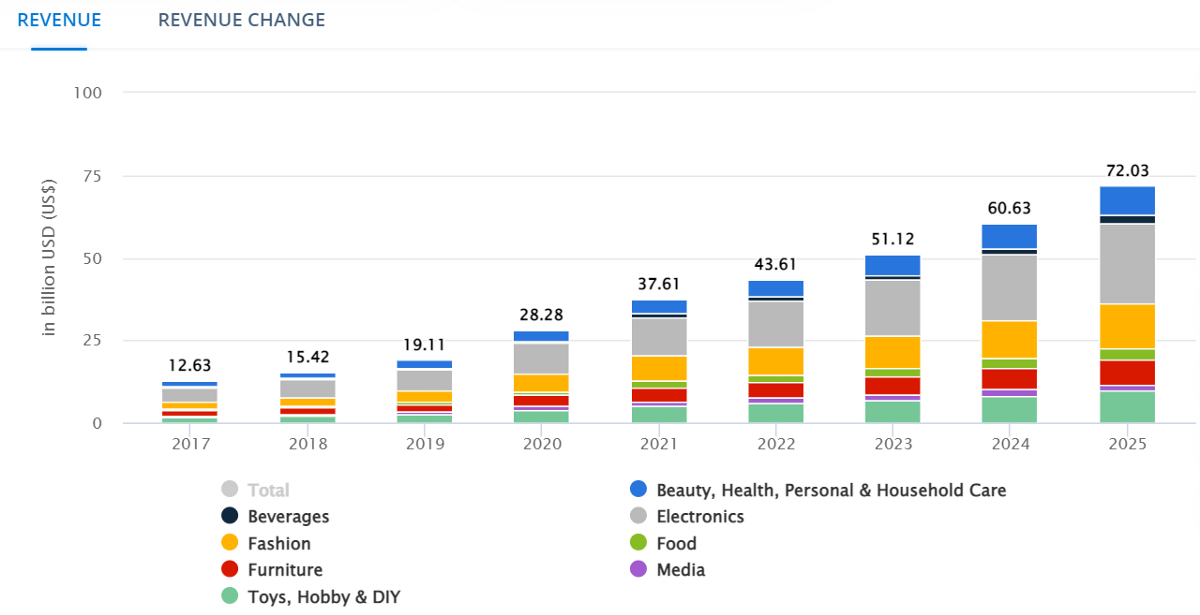

First, let’s share some market data about the e-commerce outlook in Africa. According to Statista, the African e-commerce market in 2021 was worth $38B and is projected to grow to $72B by 2025. This market is dominated by South Africa, Nigeria, Egypt, and Kenya (61% of the total). Within e-commerce, the largest categories are electronics, followed by fashion, toys, and personal care.

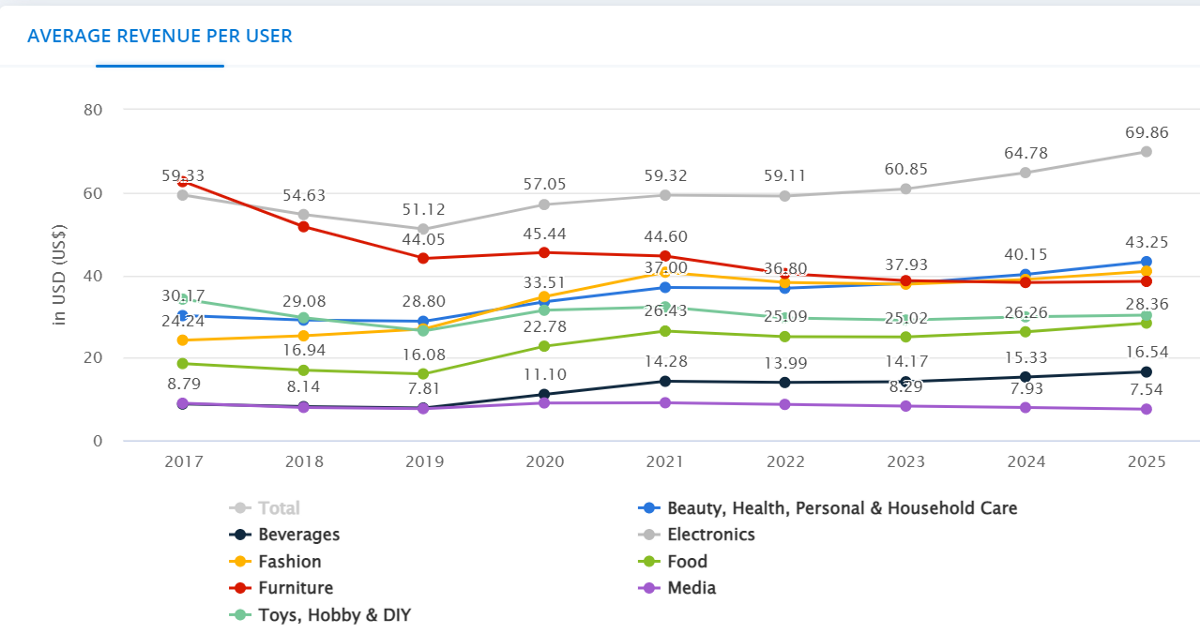

Figure 2: ARPU in Africa by Product Category

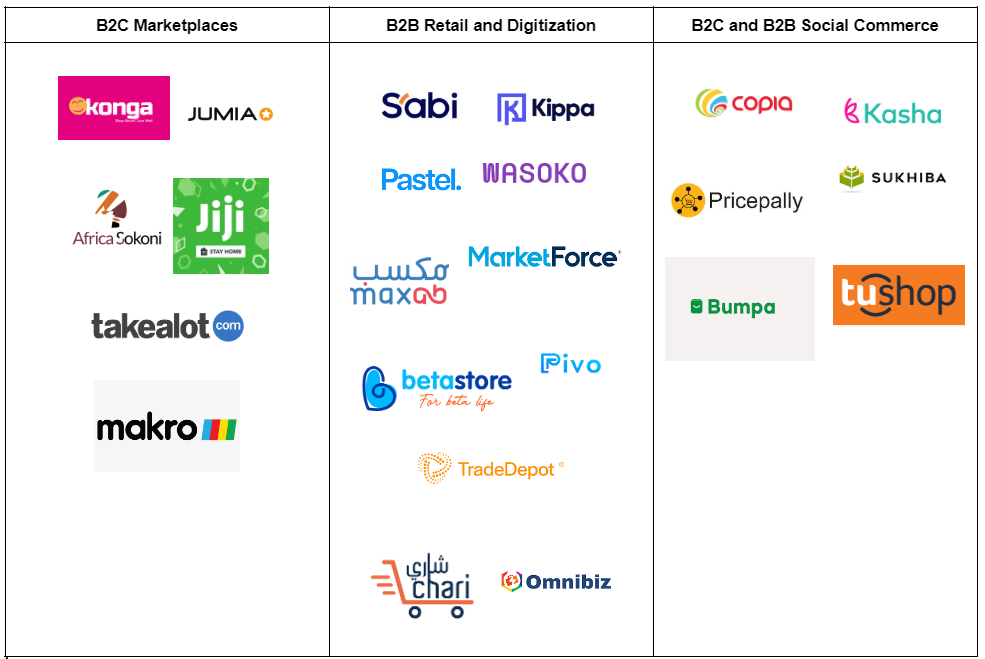

To date, Jumia, Jiji, and Konga in East and West Africa and Takealot and Makro in South Africa have dominated the rising e-commerce market. For reference, Jumia generated approximately $1B in platform sales in FY2021. It’s worth noting that Jumia has had its fair share of challenges since it launched in 2012, as they had to build logistics and payments infrastructure in addition to consumer education from the ground up. A company like Amazon can actually benefit from a second-mover advantage.

Let’s compare Africa to market trends in other emerging markets that Amazon has entered in the past decade. Latin America is a $100B e-commerce market, dominated by Brazil at $34B and Mexico at $23B in 2021. Amazon generated approximately $1.5B sales from Brazil and $1.4B from Mexico in 2021, where they’re behind competitors like Mercado Libre, with only a 4–6% market share. Similarly, the Indian e-commerce market is worth $63B, where Amazon generated $2.6B in 2021. For more background, see Amazon’s evolution in India here and in Brazil here.

While Africa currently represents a much smaller market compared to Latin America and South Asia, the macroeconomic trends indicate a readiness for e-commerce to grow significantly in the next 10 years.

- Almost 1 billion people (or 70% of the African population) are under the age of 35 and 650M people are under the age of 17.

- As a result of this youth bulge and improvement in technology adoption, there has been increasing penetration of smartphone and internet usage. According to Statista, there are currently 570M internet users on the continent. Although trust is still low, there is a rising familiarity with e-commerce.

- The technology ecosystem has been growing steadily over the past decade, with startups raising over $5B in 2022. Many of these innovations have been in the infrastructure that allows e-commerce to flourish, including logistics and warehousing, digital payments, accurate addressing, technology talent, and online/offline customer acquisition.

Now let’s break this down further into the key pieces of a successful B2C e-commerce marketplace and how Amazon can win in Africa.

1. Consumer trust

- The biggest barrier to success may be consumer education and trust. E-commerce is still relatively new to most Africans who typically visit their local corner shop for everyday essentials. Those who have used e-commerce have often faced various issues like fraud, poor quality or counterfeit products, late deliveries, lack of return options, etc. However, as elsewhere in the world, Covid-19 has accelerated digital commerce in Africa as well.

- There is seemingly a lack of satisfaction with existing options like Jumia and Konga, which is a double-edged sword. On one hand, Amazon faces less direct competition (unlike in Latin America and India), but on the other hand, they have to prove they’ll actually be better instead of a replica. For example, after Amazon acquired Souq in Egypt, customers still supposedly complained about long delivery times, poor packaging, and customer service issues.

- Recommendation — Amazon will have to ensure quality and affordable products and timely delivery to earn the trust of its customers. When the experience is sub-optimal, customers should have the ability to return the product and receive refund or credit for this value. They could also benefit from investment into brand awareness (e.g. billboards) and possibly a few brick and mortar customer service hubs.

2. Procurement

- The next thing they’ll need to get right is their internal operations, starting with procurement. Amazon will need to decide if it will launch with a first-party (Amazon-controlled inventory) or third-party (supplier-controlled inventory) approach. For context, Jumia started with a third party marketplace which still dominates its overall platform sales, but they’ve recently been prioritizing a shift to first-party sales.

- Either way, Amazon will need to develop strong relationships with importers, manufacturers, distributors, and resellers. Given the prevalence of counterfeit products in the market, they’ll need to find ways to verify sellers or the authenticity of products or go the private label route.

- Amazon will also need to decide which categories to launch with. For context, Jumia started with electronics (higher AOV, higher margin, lower volume) but has since been increasing its focus on FMCG and Grocery (lower AOV, lower margin, higher volume). In Brazil, Amazon launched with Kindles and books and then gradually expanded to electronics and household goods. In Africa, Amazon would benefit from offering a variety of categories and higher AOV items to justify delivery fees (unless they offer free shipping).

- If Amazon takes a first party approach and imports supplies themselves, they can maintain a higher margin but they’ll need to manage FX risk either through hedging or country diversification, given the volatility and devaluation experienced by many African countries in recent years.

- Recommendation — To control quality from the outset, Amazon should take a first-party approach across 2–3 key categories (electronics, fashion, personal care), working directly with manufacturers and importers. For the longer tail of product categories, they can consider a third-party marketplace approach. This will also allow them to retain higher margins to possibly subsidise delivery costs.

3. Fulfilment

- Next comes the actual fulfilment of deliveries to customers. Amazon will need to decide whether to buy their own fleet and warehouses or work with (or acquire) 3PL partners. Ultimately, that might depend on how committed they are to Africa for the longer-term and how quickly their competitors are moving.

- For storage of inventory, I would expect a central warehouse in addition to smaller fulfilment centres in closer proximity to customers. They’ll also need to cost-effectively deliver to the last-mile through a combination of trucks, 3-wheelers, and motorcycles. Customers are especially sensitive to delivery fees, which Amazon may need to absorb to remain competitive.

- Potential tech-enabled 3PL partners include Sendy, Glovo, Max.ng, or Gokada for transport and Gobeba and Haul247 for micro-warehousing. There’s also more traditional 3PLs like Africa Logistics Properties. Ultimately Amazon will need to compare the cost per square metre, delivery cost, delivery rate, and delivery speed between these 3PLs vs. Fulfilment by Amazon (FBA).

- Another challenge for Jumia initially was adequate addressing to enable accurate and efficient delivery. However, this has been improving in recent years due to Google Maps and startups like OkHi which are currently being used by the likes of Uber and Bolt.

- Africa is still largely a cash-based economy but since the launch of MPesa, Flutterwave, and a wave of cross-border payments startups, online payment acceptance (mobile money, local and international cards, crypto / stablecoin wallets) has become much easier. This can decrease cart abandonment and fraud, while improving the speed and conversion rate of transactions. Amazon may also want to consider creating a digital wallet for customer payments.

- Other fulfilment considerations include the durability of their packaging and return processing and logistics.

- Recommendation — To scale quickly, Amazon should initially partner with 3PLs like Sendy and Gobeba. If it proves to be cost-effective, then an acquisition could make sense to eventually become Amazon’s in-house FBA.

4. Talent and other operations

- Often overlooked is the need for quality talent to scale a B2C e-commerce marketplace across multiple markets. This is often the largest bottleneck for high-growth startups in Africa, forcing many to pay very high salaries to compete for local talent or seek remote talent abroad.

- Companies like Andela have supported the local ecosystem of skilled software engineers. Similarly, Zindi is generating a strong pool of data science talent. When it comes to marketing and operations talent, tech startups are often poaching from Jumia.

- Then there’s also customer experience talent, where existing call centre options like iSON and Dial Afrika exist.

- Because it didn’t fit elsewhere, I also wanted to emphasise the importance of fair regulation and tax treatment for a thriving e-commerce market. Depending on the market, Amazon may need to co-create more business-friendly laws alongside the regulators.

- Recommendation — Amazon will likely need to recruit a mix of local and international talent, which will require poaching from other African marketplaces. They should also build a robust in-house training program for longer-term sustainability.

5. Customer acquisition and retention

- The sustainability of Amazon in Africa will ultimately depend on its unit economics, particularly its LTV, AOV, and CAC.

- As mentioned above, the AOV will be critical to make fulfilment cost-efficient. The customer segments that can afford to make significant purchases at one time are primarily high-income populations and gradually the rising middle class. Some startups like LipaLater and CredPal, are focused on BNPL offerings to enable instalment-based payments. Others like Tushop, Sukhiba, and Pricepally are enabling group-buying to increase the AOV.

- Mobile-first advertising has been growing through channels like SMS, Whatsapp, and Instagram. You’re even seeing a significant amount of commerce being done on these platforms via Whatsapp chatbots and the rising influencer community on Instagram and TikTok. Companies that are enabling this acquisition and retention include the likes of Terragon, Ajua, Beem, and Wowzi and will be key to decreasing CAC over time.

- Offline customer acquisition channels also continue to thrive in Africa. In addition to standard billboards and showrooms (which increase trust and familiarity with a brand), many B2C e-commerce startups have leveraged community agents (paid a commission on sales) to educate and acquire customers and also support last-mile delivery, especially in more remote areas. Examples include Kasha, Copia, and Jumia’s JForce.

- Recommendation — The middle and high-income urban consumer is a highly sought after segment and Amazon will need to invest in truly understanding their behavior and needs through focus groups, consumer data analytics, and influencer marketing. They should also partner with the relevant BNPL partners in each market to increase AOV.

6. Alternative business models

- If Amazon struggles with the traditional B2C model that has worked in other markets, they may need to consider adapting to models that are better suited for frontier markets.

- Over the past 5 years, we’ve seen the rise of B2B e-commerce marketplaces like Sabi, TradeDepot, and Betastore in West Africa, Wasoko and Marketforce in East Africa, and Chari and MaxAB in North Africa. These companies are enabling the existing infrastructure of small retailers and resellers with reliable and convenient access to stock, credit, and better pricing.

- Others like Kippa, Anka, Pivo, Pastel, and Bumpa are also supporting the digitization of these MSMEs with digital bookkeeping, working capital, social commerce, and other merchant tools.

- Similarly, Amazon could also serve these informal retailers or even partner with them as micro-fulfillment centres or pick-up points. They’ve already taken this approach in emerging markets like India. They could also partner with more formal retailers like Carrefour, Shoprite, Naivas, and Quickmart to provide a hybrid offering (a la Whole Foods in the US). This is the approach WalMart has taken in South Africa with their MassMart and subsequent OneCart and Wumdrop acquisitions.

- Recommendation — I expect Amazon to launch with its bread and butter B2C marketplace approach in key markets like Nigeria and South Africa. For smaller, less developed markets, they should strongly consider a hybrid approach serving and/or partnering with retailers as well.

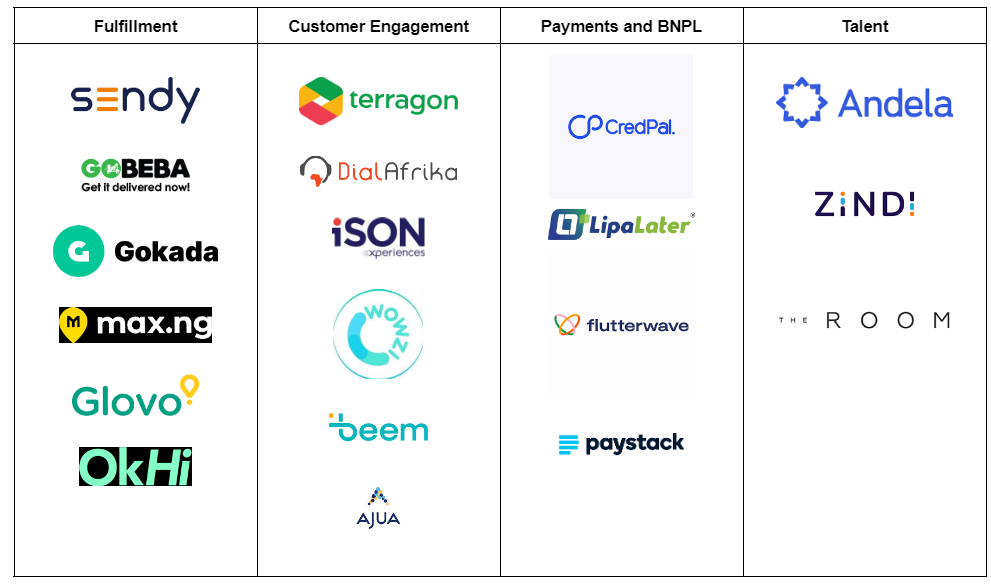

Figure 3: Sample of e-commerce enablement companies active in Africa

Figure 4: Sample of e-commerce alternatives active in Africa

Many questions remain about the approach Amazon will take in Africa but I’m excited to see what happens with their initial launch in 2023 and their evolution over the subsequent months and years. With increased competition and options in the market, hopefully the consumer ultimately wins with higher quality products, better customer service, more affordable prices, and increased access. I hope you found this analysis helpful, please leave comments, suggestions, and questions below so we can keep the conversation going.