As the CBN struggles to solve Nigeria’s FX problems, it will receive a $3bn boost. The jury is out on whether this will bring short-term stability.

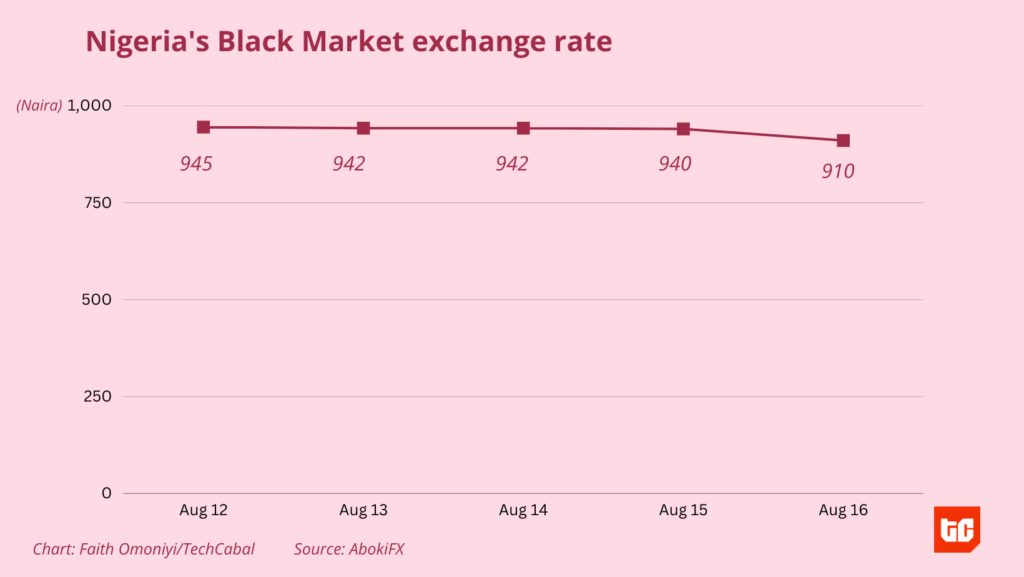

A day after the acting CBN governor Folashodun Shonubi told reporters about plans to stabilise Nigeria’s recently volatile FX market, the Naira gained N30, exchanging for N910/$1 on the parallel market after closing at N940/$1 on Tuesday. After a meeting with President Tinubu on Tuesday, Shonubi said the CBN would roll out new measures; “Some of the plans and strategies, which I am not at liberty to share with you, means sooner rather than later, the speculators should be careful because we believe the things we’re doing, when they come to fruition, may result in significant losses to them.”

After an attempt to unify rates began with optimism in June, it became clear that the CBN did not have the resources to settle the FX backlog. This inability to meet demand meant that the parallel market continued to be the viable source of supply, creating sharp differences in price from the official I&E window. At the time of this report, the I&E window quoted a price of N785/$1, presenting an arbitrage opportunity that the CBN is desperate to eliminate.

While the markets moved quickly today, many observers remained at a loss about what drove the gains. NNPC Limited confirmed today that it secured a $3 billion emergency crude repayment loan from Afrexim Bank. The loan to the NNPC is upfront cash for future proceeds from some crude oil production; with the money, the NNPC will be able to settle its taxes and royalties to the Federal Government, providing much-needed FX. The thinking is that the loan will clear the current FX backlog, which some sources earlier estimated to be between $2.5 billion.

Yet, things could turn out differently. With an actual backlog of FX demand of $10 billion (8 Trillion), the loan from Afrexim may be incapable of solving the liquidity problem in the medium or long term. Some observers have suggested that an IMF loan is inevitable, given the country’s finances. In the end, loans, wherever they’re from, are only temporary solutions to get the house in order. Nigeria must deepen its FX and monetary reforms and improve its oil production.