This article was contributed to TechCabal by Leslie Ossete, through The Realistic Optimist, a paid newsletter covering the globalised startup scene.

A tale of two cities

Africa has seen a schism between its francophone and anglophone startup ecosystems. The latter have vastly outperformed the former, carried by Nigeria and Kenya. Francophone Africa has had a late start to the race, despite ecosystems like Tunisia becoming legislative pioneers in the field.

Multiple factors explain the dichotomy, each of them linked.

First, anglophone Africa implemented foundational infrastructure such as mobile money earlier than its francophone counterparts. M-Pesa, widely recognized as mobile money’s paragon, hails from Kenya.

Mobile money has been the cornerstone of many African startups’ strategies, representing a convenient halfway between burdensome but prevalent cash and efficient but rare online payments.

This infrastructure fomented startup creation, putting pressure on the local job market to form startup-ready talent, such as developers. This gave rise to companies like Nigeria’s Andela, tasked with pumping out that tech-literate workforce. A similar trend is picking up pace in francophone Africa through companies like GoMyCode, but the initial infrastructure delay has retarded subsequent steps.

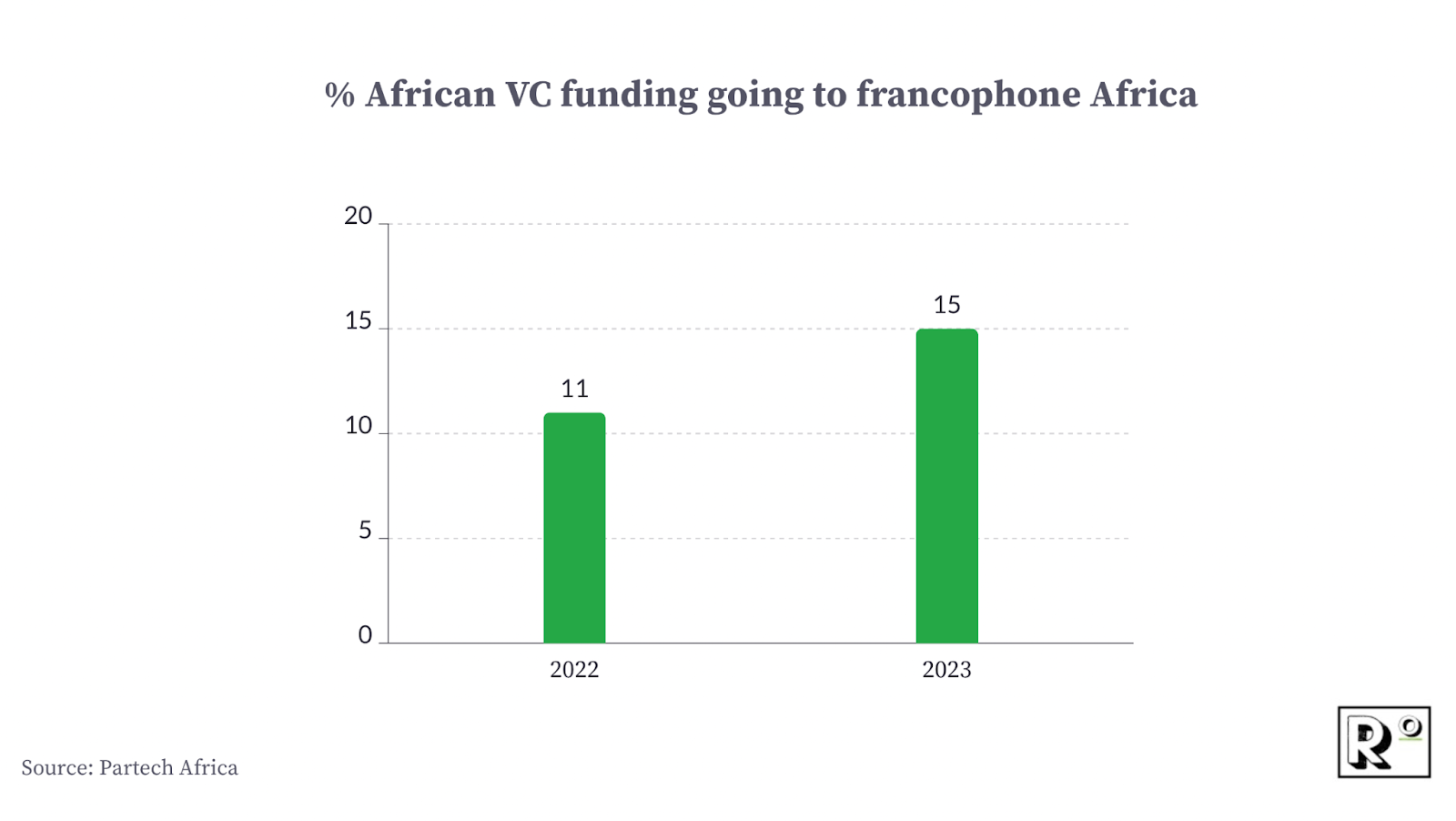

This initial lag domino-affected VC funding. In Africa, a group of countries known as the “Big Four” (Egypt, Kenya, Nigeria, and South Africa) received over 75% of the continent’s 2022 VC funding. As the astute observer will note, anglophone Africa boasts three members in that group, compared to francophone Africa’s zero.

These three linked reasons explain the logical, visible reasons for the lag. More subtle differences may have contributed as well.

Anglophone African countries tend to enjoy a more entrepreneurial culture compared to Francophone ones, owing to divergences between English and French economic dogma (laissez-faire vs dirigisme). With an important fraction of African VC funding coming from the United States, francophone founders also face a substantial linguistic challenge when pitching in their second or third language.

This overarching anglophone business culture led to the launch, as early as 2010, of formative tech hubs such as iHub and Co-Creation Hub in Nairobi and Lagos respectively. These encouraged knowledge sharing and skill building, crucial to exposing local talent to startups’ intricacies.

Trade is also easier in anglophone regions. Anglophone East Africa is a more auspicious cross-border expansion environment than francophone West Africa, for example. Cultural uniformity plays a role, with West Africa’s religious mix making it hard for an Ivorian fintech founder to onboard Muslim (and thus usury-free) users in neighbouring Mali. Trade agreements in East Africa also hold more weight than the ones in West Africa.

As for Nigeria, its crown as Africa’s most populous nation gives founders ample space to scale before even thinking of foreign forays.

Graph source: Partech

Ivory Coast: A smaller, francophone Nigeria?

Despite the challenges, the past couple of years have seen francophone ecosystems pick up speed and the jury is out for its most promising contenders. Ivory Coast ranks high on the list.

Compared to state-led peers such as Senegal, Côte d’Ivoire’s startup ecosystem was trail-blazed by the private sector. The CI20, a collective made up of early Ivorian founders, was instrumental in materializing an otherwise free-flowing ecosystem, including the implementation of the country’s Startup Act.

Côte d’Ivoire’s founders operate in an unequal albeit booming economy, clocking in Africa’s highest 2024 GDP growth forecast. Compared to some of its anglophone neighbours, Côte d’Ivoire enjoys a sturdier currency by virtue of its peg to the euro.

The digitalization of this growing economy is where the Ivorian startup opportunity lies. While the country’s ecosystem has witnessed an “Anglo-style” private-sector-led development, the country’s founders still face perennial “francophone” Africa problems.

This includes a lack of familiarity with the lingo, codes, and other quirks of the VC-backed startup world. As a result, many promising Ivorian companies end up as stable digital SMEs rather than the fast-growing startups they could aspire to be. This is less of a problem in anglophone Lagos, where startup culture is more widespread.

While orders of magnitude smaller than Nigeria (28 vs. 219 million people), parallels can be drawn between both ecosystems. Bottom-up development, a booming economy, and many industries to be tech-disrupted breed great potential.

To attain the next level, the Ivorian ecosystem could benefit from what made Nigeria tick: an inflow of returning diaspora talent, bringing with them capital and startup savviness.

Investors should view Côte d’Ivoire as a gateway to the 140 million people-strong francophone West Africa region, a vast and untapped greenfield for tech innovators.

No need to reinvent the wheel

One might wonder which business ideas Ivorian startups should pursue. The answer is not as complicated as many make it out to be.

So far, many African startup successes have been built on the back of an existing business model, something that had worked elsewhere but not on the continent. Think online payment gateways, peer-to-peer fintech, e-commerce marketplaces and ride-hailing. Where Africans can claim a pioneer position are mobile-money-related innovations.

The point is the following: if a business model is working in a socio-economically similar market to X African country, there’s an honest business case to launch it locally. This is especially true for startups digitizing the informal sector, a field where African founders can look to LATAM or South East Asia for inspiration.

While geographically distant, these continents share the similarity of having a large informal sector and all the challenges (and opportunities) that it brings. LATAM and Southeast Asia are a few steps ahead of Africa economically, so observing what worked there could be insightful.

For example, the thesis behind Frubana, a B2B marketplace connecting small restaurant owners to local producers, might’ve originated in Colombia but is pertinent to many African markets. With the right localization tweaks, such as enabling mobile money payments, the idea has the merit of at least being tested.

Sourcing startup business models from slightly more advanced markets is akin to a crystal ball, conferring the ability to predict what startups might or might not work locally. As African founders search for the next big idea, they should leverage this seemingly time-travelling hindsight.

That is the thesis the Abidjan-based venture studio I run (M-Studio) is built on.

Conclusion

“Pourquoi faire simple quand on peut faire compliqué ?” goes a French adage, sarcastically questioning, “Why do simple when you can do complicated?”

Despite small localization singularities, startup ecosystems tend to be very similar from Uzbekistan to Lithuania to Brazil. You have startups, VCs, incubators, universities, and a more or less cooperative government. Everyone is looking to do the same thing: disrupt antiquated industries through tech and financially bet on that disruption’s ability to hyper-scale.

Each startup idea is likely to have a comparable in another geography. If it does, it might be worth trying it locally. The reason for that is simple: people, regardless of where they live, generally want the same things: to live a less burdensome existence, take care of their loved ones, and offer their kids opportunities they never had.

The prioritization of those desires and the ability to pay for services that fulfil them varies, which is why business model replications are especially relevant across socio-economically similar geographies.

While adapting to local specificities, this approach can take off significant weight in finding and testing “the right idea”.

In a world as complex as ours, there’s no need to deeply reinvent stuff that works elsewhere.

—

Leslie is the co-founder of M-Studio, an Abidjan-based venture studio that launches startups serving francophone West Africa. Before founding M-Studio, Leslie was the growth lead at Wave and the regional operations manager at Bolt. Right out of university, she co-founded a startup (Buupass) in Kenya, which still operates today.

{kind=link}