Tech and TAM realities

ICYMI – On Monday 3rd of August 2020, 15 years after it first set up its first outlet in Nigeria, South African retail giant, ShopRite announced it is considering selling all or a majority stake of its business in Nigeria.

According to a CNN report the company said;

“[Its] South African

division grew by 8.7% while sales at its supermarkets outside South Africa (excluding Nigeria) fell by 1.4%.”

Of course, mixed reactions trailed this announcement, and this report does a decent job of summarising the whys: currency fluctuations, profit repatriation, logistics concerns, sundry issues, COVID-19 and purchasing power.

It is also important to remember that two months

earlier, in June, Mr. Price, another South African retail brand shuttered operations in Nigeria.

Considering that Woolworths, yet another South African company, left in 2013, are Mr. Price and ShopRite 7 years too late?

Maybe. Maybe not.

In a Financial Times report at the time, a representative from Woolworths said;

“High rental

costs and duties and complex supply chain processes made trading in Nigeria highly challenging. The Nigerian business was unable to sustain a compelling product and value proposition which represents the brand well, and meets the needs of the Nigerian customer in a climate that is hot throughout the year. Given that Woolworths could not see these circumstances changing in the medium term, the investment was deemed no longer viable.”

These problems still persist to a large extent; it’s still very hard to do business in Nigeria.

But, it is also very important to note that this is not primarily a Nigerian problem and or, considering recent xenophobic history, a South Africa vs Nigeria problem.

Last year, Choppies and TFG exited the Kenyan market, the latter also left Ghana. They mostly cited increased competition and high operating costs.

How do all these dots connect?

Tech and the TAM illusion

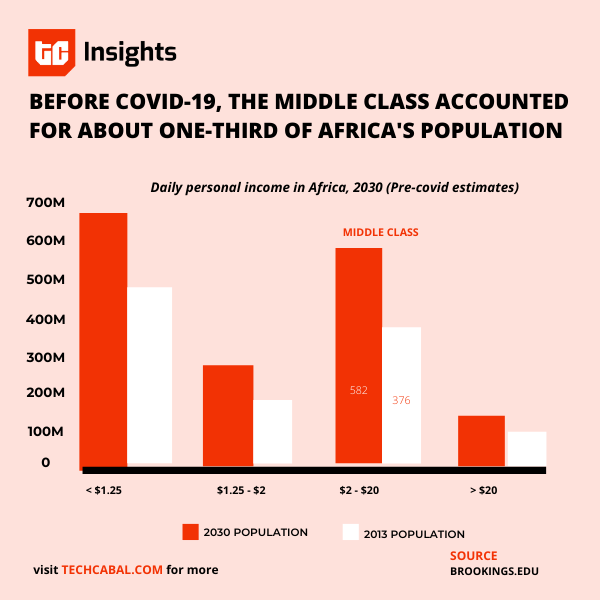

In Africa’s growing tech and innovation ecosystem, there is a huge overestimation of the number of people that are willing, and able to pay for product and services; the total addressable market (TAM).

Most startup founders have a slide in their pitch deck where one variation of population size is directly equated to market size.

The fact that these huge retail brands selling essential goods are shuffling in and out of struggling African markets is very instructional. Will consumer tech

products, largely considered luxury in this context, sell?

Africa’s middle class is growing exponentially, but that may not even matter eventually, and you’ll see why.

According to a 2011 report (PDF) from the Africa Development Bank;

“The number of middle class Africans has tripled over the last 30 years to 313 million people, or more than 34% of the continent’s population, according to a new report from the African Development Bank (AfDB). The reasons for the increase in size and purchasing power of the African middle class include strong economic growth, and a move towards a stable,

salaried job culture and away from traditional agricultural activities.”

However, these numbers are positive, but not necessarily exciting when checked against population growth rates in Africa, and other – less populated – continents in the world.

This World Bank’s 2019 ‘Accelerating Poverty Reduction in Africa’ report is a paradox that puts this into better

perspective;

“The share of Africans living in extreme poverty has fallen substantially—from 54% in 1990 to 41% in 2015—but due to high population growth during the same period, the number of poor people in Africa has actually increased from 278 million in 1990 to 413 million in 2015. If circumstances remain the same, the poverty rate is expected to decline to 23% only, by 2030 and global poverty will become increasingly African, rising from 55% in 2015 to 90% in 2030.”

TLDR: As more people are escaping poverty, more are being born into it.

In a now popular Medium article from August 2019, VC and entrepreneur, Dr. Ola Brown dissects the mystery of market size in Nigeria. And most importantly, why population size does not equal TAM.

Nigeria is arguably regarded as Africa’s largest economy, but these lessons can be extrapolated to other markets on the continent.