TechCabal Insights presents trends and events in African tech during the second quarter of the year: Sectoral funding, expansions, acquisitions, regulations, and more.

In our analysis of trends and events in Q2 2023, we provide a glimpse into the major moves and the occasional rocky road in the African tech ecosystem. Let’s dig deep into the data, as we explore the highs and lows, the triumphs and challenges that defined the ecosystem during the recently-concluded quarter.

Funding: A rollercoaster ride

Image source: Ayomide Agbaje/TechCabal Insights

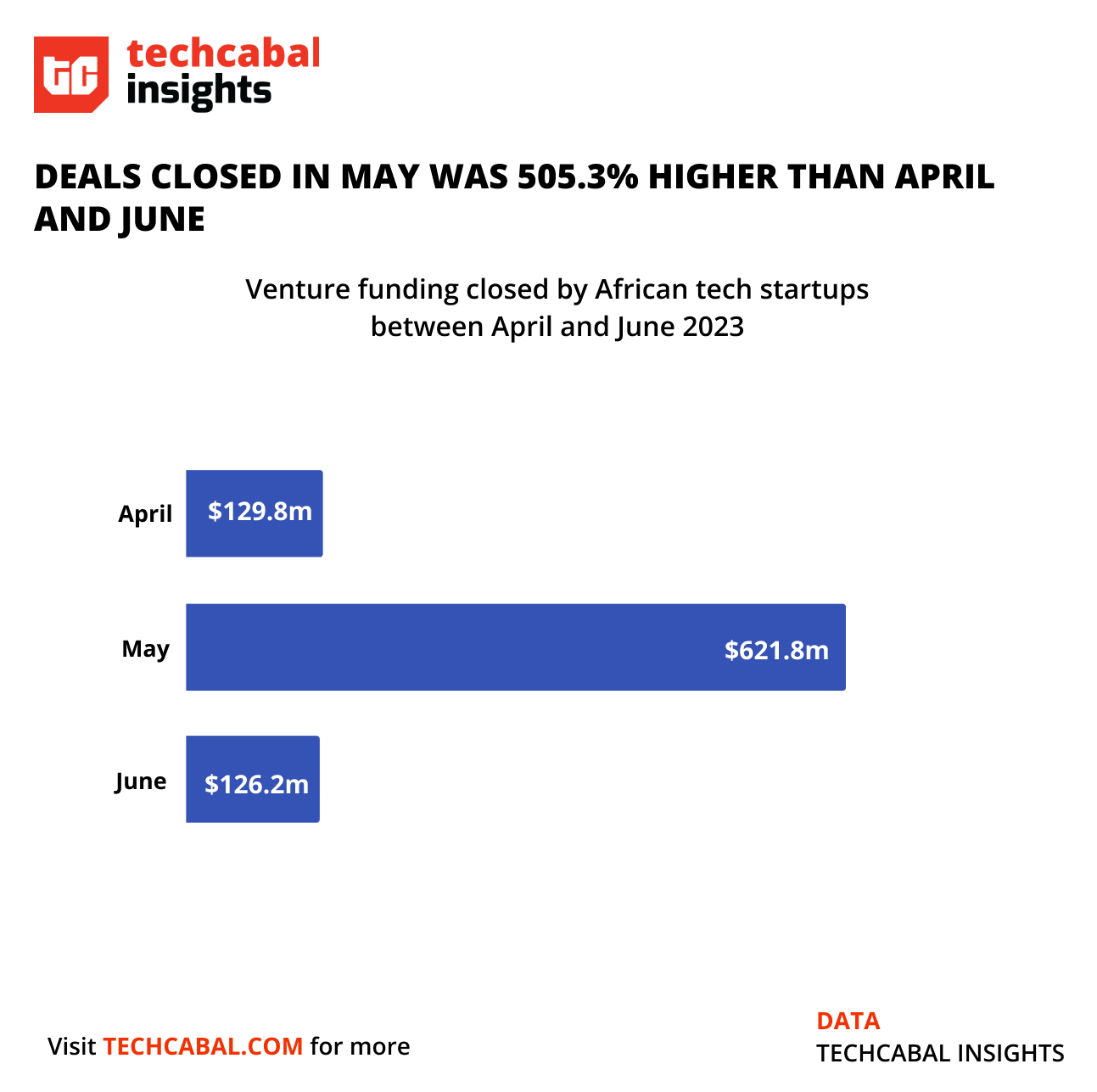

Notably, venture funding reached $621.8 million in May from 34 announced deals—a 42% year-on-year increase from May 2022. This was driven by two mega deals: M-Kopa securing $255 million in a debt-and-equity financing round and SunKing’s $130 million securitisation deal. This was unlike the momentum in April and June which had deals amounting to $129.8 million from 23 announced deals and $126.2 million from 25 announced deals respectively.

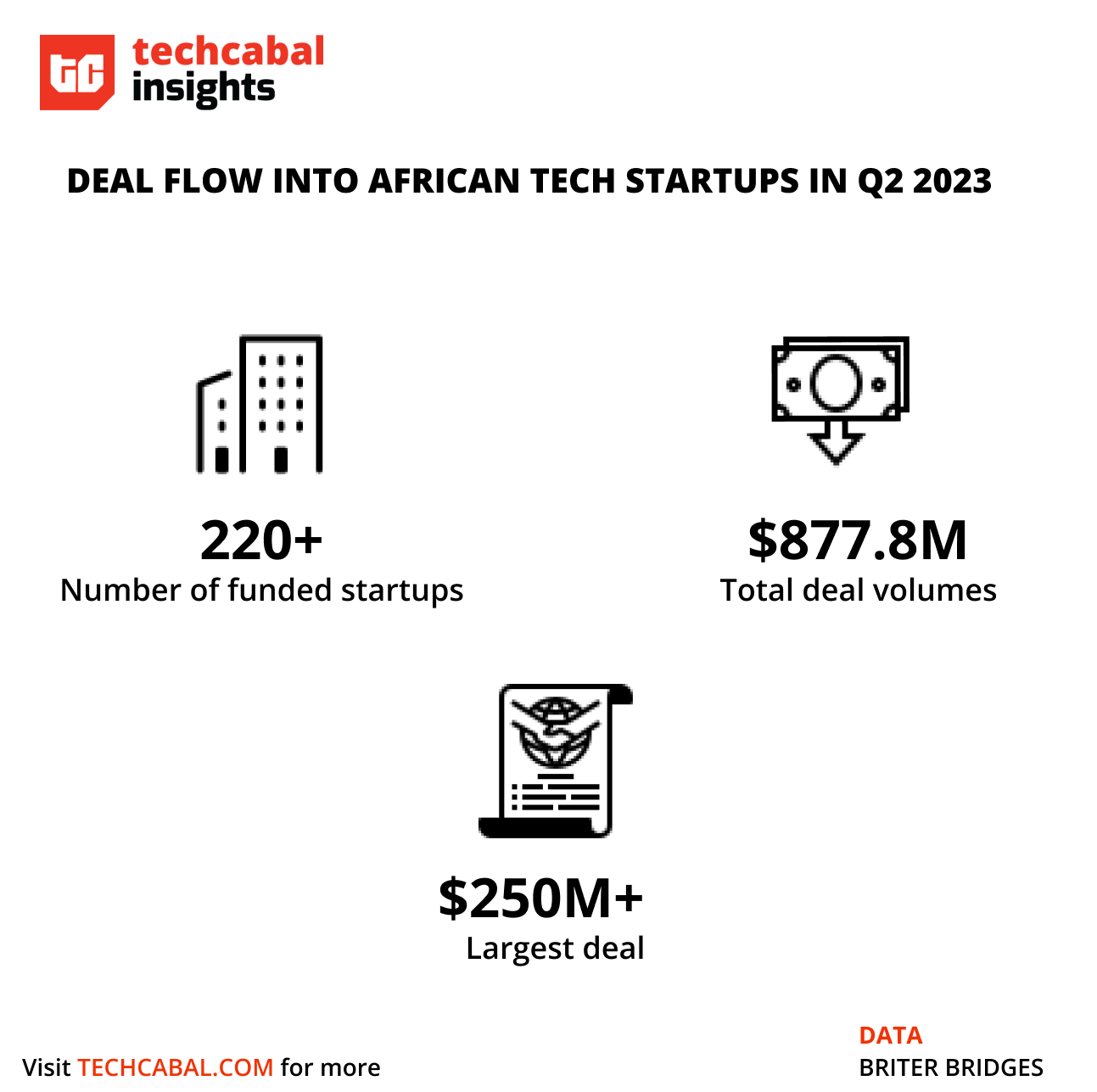

While the figures show a general slowdown in funding for African startups, the quarter still witnessed an impressive feat. A total of $877.8 million was raised across 220 startups, representing a 6.9% increase from Q1 2023. Although these numbers fall short of the $1.2 billion raised in the corresponding quarter of the previous year (Q2 2022) at a 23.63% decline.

Image source: Ayomide Agbaje/TechCabal Insights

Sectoral breakdown: Energy (cleantech) surpasses Fintech

Startups operating in the energy, fintech, and logistics sectors emerged as the frontrunners in Q2 2023. Unlike previous quarters, fintech startups didn’t receive the largest share of VC funding. Energy-focused startups replaced them, raising $486.9 million, which accounted for 53% of the total funding in the quarter. Contrary to expectations, the funding landscape for African fintech in the previous quarter did not live up to the anticipated levels of success. For example, the number of fintech startups securing funding in June 2023 was quite limited, resulting in a subpar performance in terms of capital investment from venture capitalists, angel investors, and accelerators. It is noteworthy that, thus far, no African fintech startups have managed to secure mega-equity deals (exceeding $100 million) solely through debt funding and grants.

Nigeria takes the lead

In the race for venture funding, Nigeria sprinted ahead in Q2 2023, leaving other Africa’s Big 4 countries Kenya, South Africa, and Egypt on the trail. Nigerian startups secured $462.4 million, while Kenya followed with $149.3 million. South Africa and Egypt received $214 million and $6.1 million respectively, experiencing a decline from their previous quarter’s highs. Notably, Kenya’s rise this quarter can be attributed to the mega deals that local startups in the country closed, which played a significant role in toppling Egypt from its previous position. These figures further highlight the dynamic nature of the startup landscape in Africa, with each quarter bringing new opportunities and challenges for both startups and investors.

Expansions: Broadening horizons

Expansion is the name of the game as African startups seek to deepen their market presence to drive both operational and revenue growth. This previous quarter, TechCabal Insights tracked four noteworthy expansion moves, a similar figure to Q1 2023’s but a sharp drop from the eight tracked in Q2 2022. Nigerian auto-financing startup, Autochek, took a major leap forward by acquiring a majority stake in Egyptian startup, AutoTager, effectively expanding its footprint across nine African countries. Also, Ghanaian agri-tech startup Farmerline spread its wings into Francophone Africa, launching its operations in Ivory Coast.

Ecosystem turbulence: Major moves and rocky events

Fintech fraud and cybersecurity concerns

In June, two South African companies witnessed cyberattacks. The first incident involved hackers gaining unauthorized access to MultiChoice’s streaming platform, Showmax, allegedly exposing more than 27,000 usernames and passwords. Meanwhile, Heritage Bank in Nigeria reported an insider hack worth ₦49 billion ($83 million) in customer funds. Also, Globus Bank, another Nigerian bank, disclosed a hack in 2022, in which hackers exploited a USSD glitch to withdraw over ₦1.75 billion ($2.9 million) from customer accounts. In Kenya, cybercriminals targeted Naivas, the country’s leading online retailer, with a ransomware attack, threatening to leak sensitive data. These incidents underscore the ongoing need for companies in the ecosystem to enhance their cybersecurity measures and address the ever-present risks of fraud.

Shutdowns: Copia Global and Lazerpay bid farewell

As Q2 2023 unfolded, the global trend of shutdowns also continued to make its mark in Africa’s tech ecosystem. Nigerian crypto startup, Lazerpay, announced its closure after struggling to secure the necessary funding. Meanwhile, Copia Global, a Kenyan e-commerce company, made the tough decision to shut down its Ugandan operations. These developments highlight the harsh realities of the tech business landscape, where even promising ventures on the continent face the pressures of sustainability.

Layoffs: Shaking the African tech ecosystem

In the ever-evolving African tech ecosystem, layoffs have become an unfortunate reality. What began with Swvl in May 2022 has continued to sweep across the continent, leaving a mark on some prominent startups.

June witnessed a wave of layoffs as five African startups collectively laid off over 238 employees. Twiga, a Kenyan agritech company, made a “cost-cutting” move by laying off 211 employees, including its entire sales team. Nigeria’s fintech Eyowo, amidst a pivot to a D2C model, also had to let go of 13 employees. Similarly, Smile Identity, a KYC startup that raised $20 million in February 2023, had to reduce its workforce by 8 employees due to challenging macroeconomic conditions. Fintech giant Chipper Cash executed its third round of layoffs, though the exact number remains undisclosed. Also, sources revealed that Mara, a Web3 startup that raised $23 million in 2022, had to make the difficult decision to lay off six employees in May.

Digital currencies by African countries

During the last quarter, Zimbabwe embarked on a new chapter by launching its digital currency. However, the International Monetary Fund (IMF) raised concerns, cautioning that the gold-backed currency might not solve the country’s fiat currency devaluation problems and could deplete its gold reserves. Despite the criticism, the Reserve Bank of Zimbabwe (RSV) sold an impressive 14 billion Zimbabwean dollars’ worth of gold-backed digital tokens, amounting to around $39 million.

The IMF also challenged Nigeria’s e-naira. Contrary to the Central Bank of Nigeria’s (CBN) claims, the IMF revealed that Nigeria’s digital currency, the e-naira, has fallen short of expectations. The IMF disclosed that an impressive 98.5% of the 14 million e-naira wallets created have never been used, even two years after their launch. With only around 860,000 retail e-naira wallets being active, equivalent to just 0.8% of Nigeria’s active bank accounts, the digital currency’s adoption appears to be underperforming.

Regulatory ripples: Nigeria revokes MFBs’ licenses

While Nigeria opened its doors to loan apps in April, May witnessed a different scenario as the Central Bank of Nigeria (CBN) revoked the licenses of 179 microfinance banks, four primary mortgage banks, and three finance companies. The regulatory crackdown was a response to non-compliance with regulatory requirements and unauthorized activities. Among the affected institutions was Eyowo, a Nigerian digital bank, which suspended all withdrawals pending the re-approval of its license, leaving customers seeking creative ways to access their funds.

The unpredictable terrain ahead: Expectations for the rest of 2023

It’s important to note that sectors experience funding slowdowns differently. This quarter saw fintech, historically the darling of the African ecosystem, take a backseat to energy startups. This indicates that investors are increasingly drawn to emerging sectors with high growth potential. While past performance isn’t always indicative of future success, we predict that fintech will reclaim its dominance by the end of 2023 based on historical trends. Only time will tell how the rest of the year unfolds.

Watch out to read more on our flagship State of Tech In Africa report, our bird’s eye view on African tech trends for Q2 2023 offering data, insights, and experts’ perspectives around funding, acquisitions, startup expansion, and regulations on the continent.