Fraud risks are rising in Nigeria’s financial system and are forcing commercial banks to devise stringent measures to rein it in, multiple industry sources told TechCabal. This follows a recent TechCabal report that Fidelity Bank, which holds ₦3.1 trillion ($3.9 billion) in consumer deposits, had restricted fund transfers to several challenger banks, including Kuda Bank, OPay, Moniepoint, and PalmPay.

With millions of customers across digital apps and offline payment channels, these four neobanks have become customer favourites and have entrenched themselves in the financial system in the past four years. But to win over customers, they have relied on flexible account verification processes while emphasising their push to improve financial inclusion in the country. These verification processes are at the heart of a clash between these neobanks and some of Nigeria’s biggest legacy banks.

Last week, Fidelity Bank blocked transfers to neobanks over lax anti-fraud and customer verification standards, sources with knowledge of the matter told TechCabal. The restrictions remained for two weeks, those sources said. News of the restrictions polarised users on social media with speculation that the bank was trying to slow down competition. The restrictions have since been removed by Friday, October 27, bank customers said.

Fidelity Bank did not respond to TechCabal’s request for comments regarding these actions.

Key Takeaways

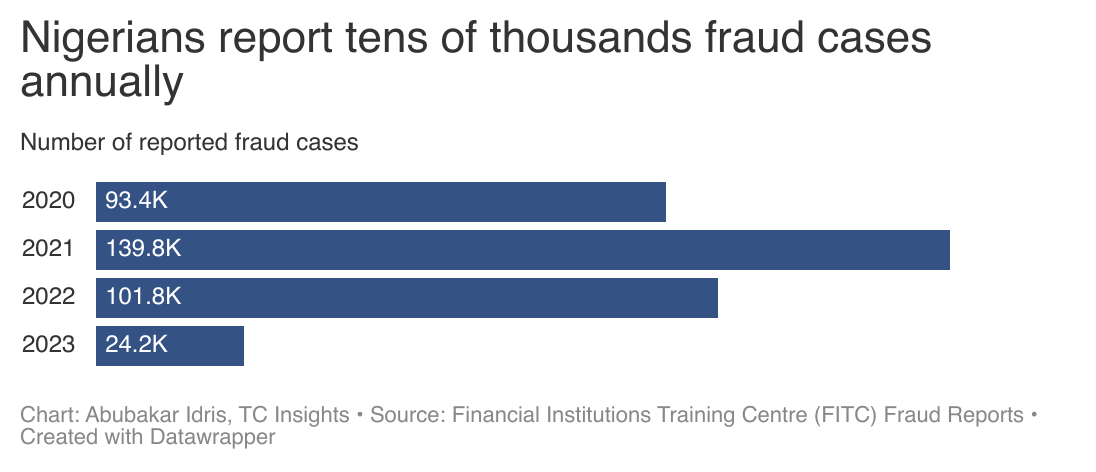

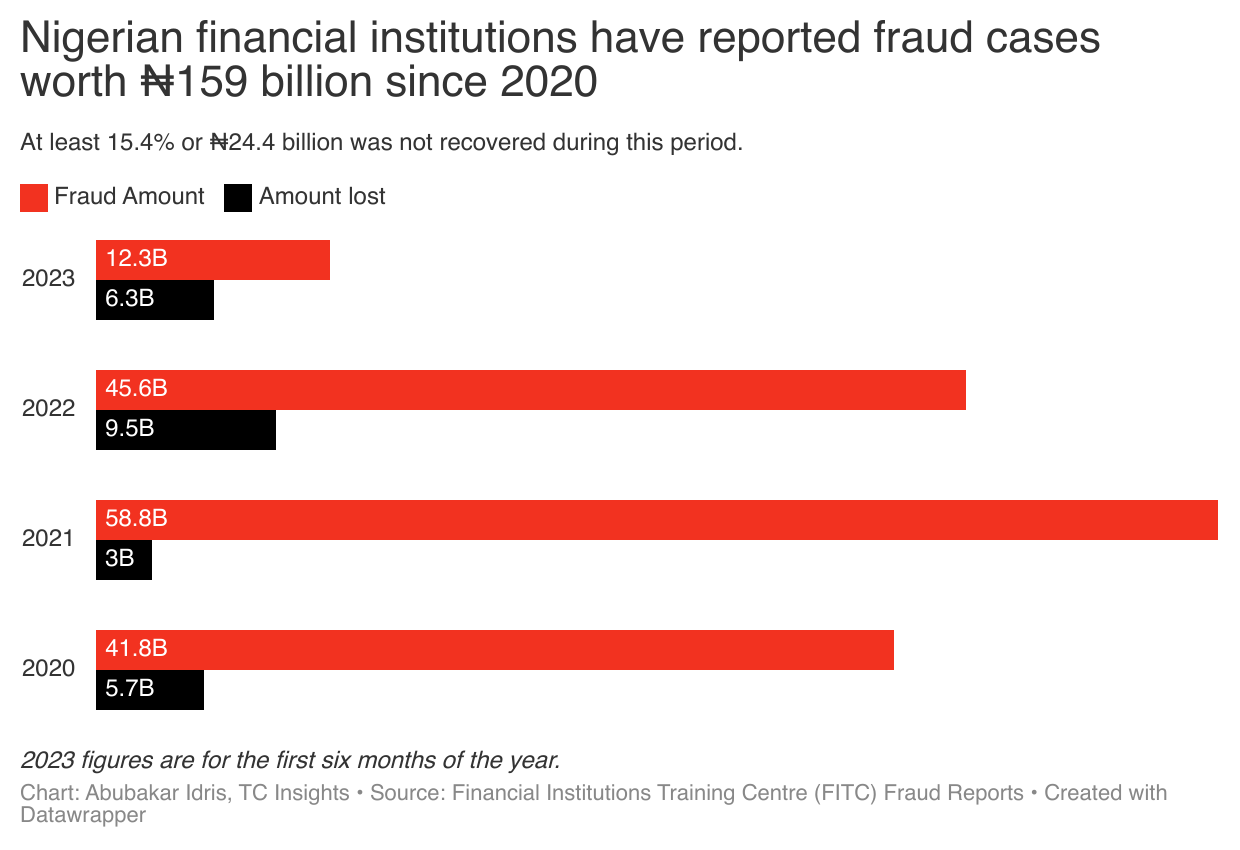

- Fraud is a growing problem in Nigeria’s financial system. Nigerian financial institutions have reported ₦159 billion ($201.5 million) lost to fraud since 2020.

- Relaxed transaction rules and flexible customer verification standards are making it easier for scammers to target victims.

- Nigeria’s financial system struggles with information sharing and lacks coordination on financial fraud investigations by local law enforcement agencies.

But Fidelity is not the only bank concerned about fraud related to neobanks. At least two other major Nigerian banks have had internal conversations about blocking these upstarts from their list of financial services for consumer fund transfers, two financial services insiders, who asked for anonymity so they could speak freely, told TechCabal.

Media reports have highlighted the scale of fraud challenges in the country. This week, BusinessDay reported that Fidelity Bank lost ₦2 billion ($2.5 million) in three attacks. Court documents posted on social media and verified by TechCabal showed that Access Bank, Nigeria’s largest bank by customer deposits, filed a lawsuit in June to recover ₦3 billion ($3.8 million) that was fraudulently withdrawn. In July, the bank filed a separate lawsuit to recover an additional ₦5 billion ($6.3 million) illegally transferred from its coffers by scammers.

Fintech startups have also been impacted. In March, Flutterwave, Africa’s most valuable startup, reportedly lost ₦2.9 billion ($3.7 million) to a cyber attack — the fintech continues to deny the incident. The mobile money service of Nigerian telecoms company MTN also lost over ₦10.5 billion ($13.3 million) in 2022 to unauthorised transfers caused by a glitch one month after it re-launched as a payment service bank.

Overall, Nigerian financial institutions have reported ₦159 billion ($201.5 million) lost to fraud cases since 2020, according to the Financial Institutions Training Centre (FITC), a financial research and advocacy organisation operated by the Central Bank of Nigeria (CBN). During this period, the industry lost around 15.4% or ₦24.4 billion ($30.9 million) to grafts, including fraudulent activity across point of sales devices, internet banking, ATMs, mobile apps, and malicious digital loan activities.

Fraud has long been a concern in Nigeria, Africa’s largest economy. Currency devaluations and large transaction volumes in developed markets like the US have meant that Nigerian-based scammers have historically targeted foreign companies, but that’s changing.

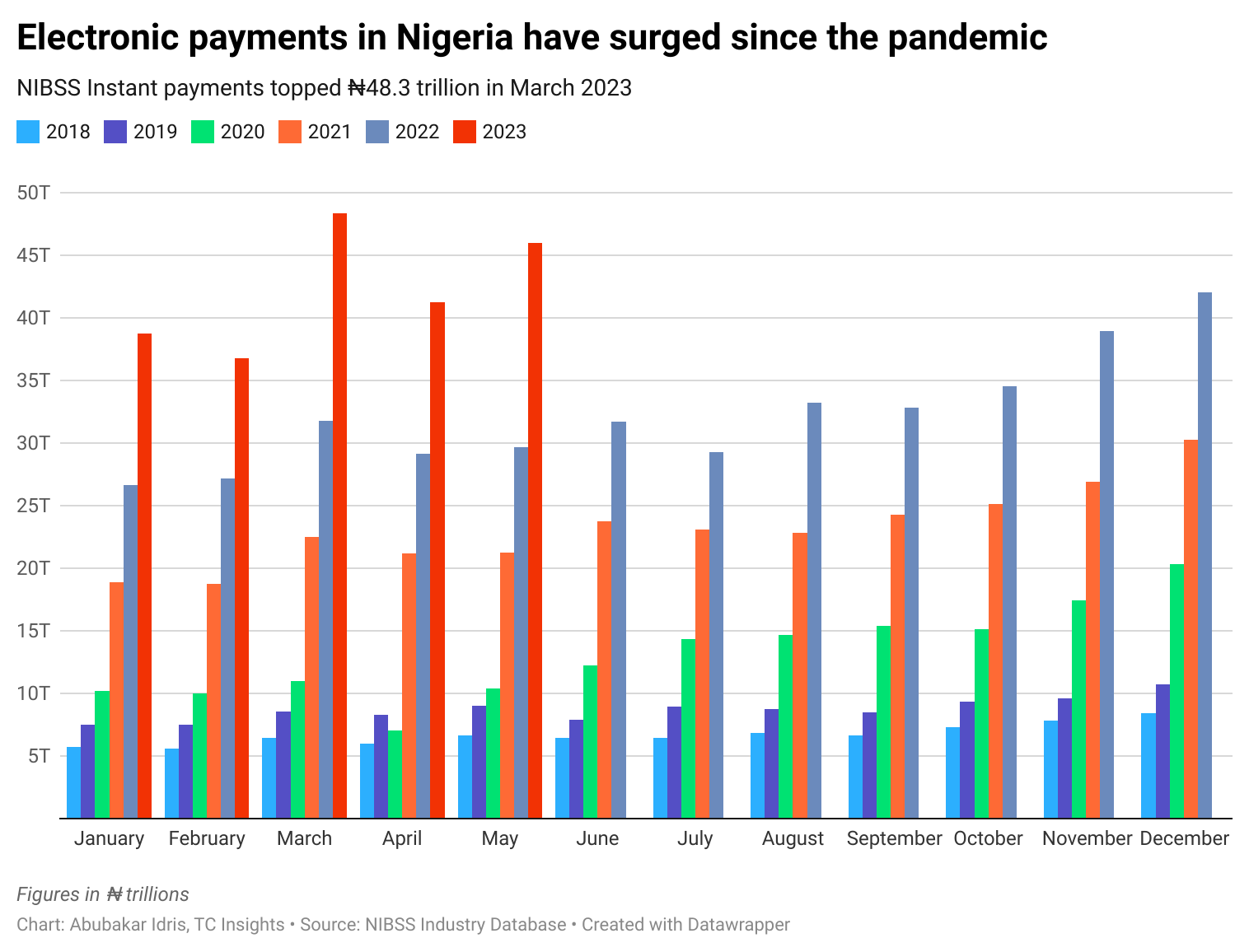

As the value of electronic payments in Nigeria has grown to ₦387.1 trillion ($490.7 billion) in 2022, up from ₦38.2 trillion ($48.4 billion) in 2016, scammers have increased their focus on the local market. That local market is mostly a mix of fintech startups and banking industry players working to improve financial inclusion. As part of the financial inclusion drive, transaction rules have been relaxed, and customer verification standards are now more flexible. Industry experts worry that this trend exposes customers and the industry to higher risks.

Phishing has become widespread, with fake social media handles posing as verified handles of local banks to collect customer information and fraudulently move monies from their accounts. It has forced GTBank, Nigeria’s most profitable bank, to fix a banner at the top of its website warning customers to “be mindful” of sites impersonating its brand.

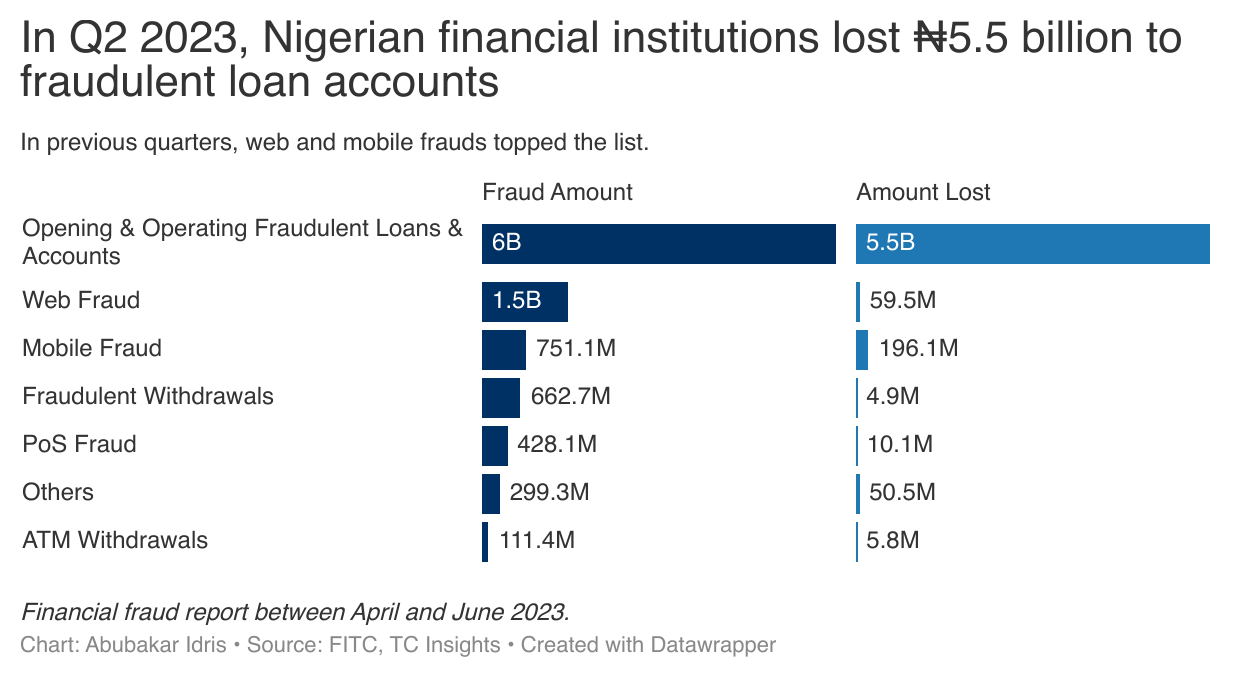

Two sources at traditional banks suggested that the verification and identity management process at banks and digital challengers was inadequate, making them susceptible to bad actors. Between April and June 2023, scammers created and operated several bank accounts, which defrauded the industry ₦5.5 billion ($6.9 million) in fraudulent loans, according to a FITC report.

A 2022 KPMG Nigeria study found that only 30% of local banks have fully implemented KYC and anti-fraud measures. “Banks do not investigate sudden inflows or outflows against accounts without prior notice. When issues become frauds, the banks claim not to be able to reach customers,” a KYC expert told TechCabal.

The country’s financial system continues to struggle with issues around information sharing, international collaborations and lack of coordination on financial fraud investigations by local law enforcement agencies, said the Financial Action Task Force (FATF), the Paris-based global anti-fraud watchdog group. In February, FATF placed Nigeria on its grey list over “identified strategic deficiencies.”

Although the country has moved swiftly to fix some of these deficiencies, Muhammed Jiya, a director at the Nigerian Financial Intelligence Unit (NFIU), warned that Nigeria could be placed on the FATF blacklist by January 2025. The black list risks cutting Nigeria from the global financial system, making it difficult for the West African country to do business with other economies or access international financing, Jiya explained on an industry webinar in March.

Policing fraud continues to face obstacles due to the uncooperative nature of several companies, industry sources explained. Traditional banks tend to work closely with one another to curtail illicit fund transfers and suspected accounts while fund recovery processes proceed. Startups are yet to catch up with such arrangements, the people claimed.

Companies have also historically been hesitant to share data on fraud activity and cyber breaches with other companies and the government despite a 2015 cybersecurity law mandating that they do so. Deposit-taking institutions are concerned about their reputation and how such timely disclosure could impact their business in Nigeria’s low-trust environment.

In March, fintech startups began talks to create a fraud database, codenamed Project Radar, to share data and other information on individuals and groups that had attempted or made fraudulent transactions. But these talks have stalled, said a source involved in those conversations.

As financial fraud increases, urgency is building for Nigerian financial services to move beyond various gaps and collaborate on a robust anti-fraud framework to protect the industry and customers.

Editor’s note: The exchange rate used in this article is $1 = ₦788.9.