A change in consumer behaviour and macroeconomic conditions are leading Nigerian banks to issue local cards like Verve to customers, dumping international card schemes like Visa and Mastercard.

Before the COVID-19 pandemic, Nigerian fintechs stumbled on an easy customer acquisition strategy: issuing foreign debit cards. These cards, often issued for free or next to nothing, ensured fintech customers could withdraw money at ATMs, or pay at supermarkets. Giving customers debit cards increased spending, allowing fintechs to earn more transaction fees.

“No regular Nigerian was going to spend [their] money from your bank if they did not have your card,” a former banker who asked not to be named told TechCabal.

However, COVID-19-related restrictions on in-person shopping, a cash crunch in Nigeria in 2023, and cash shortages at bank ATMs have changed those assumptions and reduced the reliance on card payments. They have also led to the growing popularity of bank transfers.

Fintech startups and banks are reevaluating their card operations in line with these new realities, and all Nigerian commercial banks, except Guaranty Trust Holding Company (GTCO), now issue Verve, a card scheme operated by Nigerian payments unicorn Interswitch.

First Bank, Nigeria’s oldest bank, has issued Verve cards to over half of its card customers, said one person with knowledge of the matter.

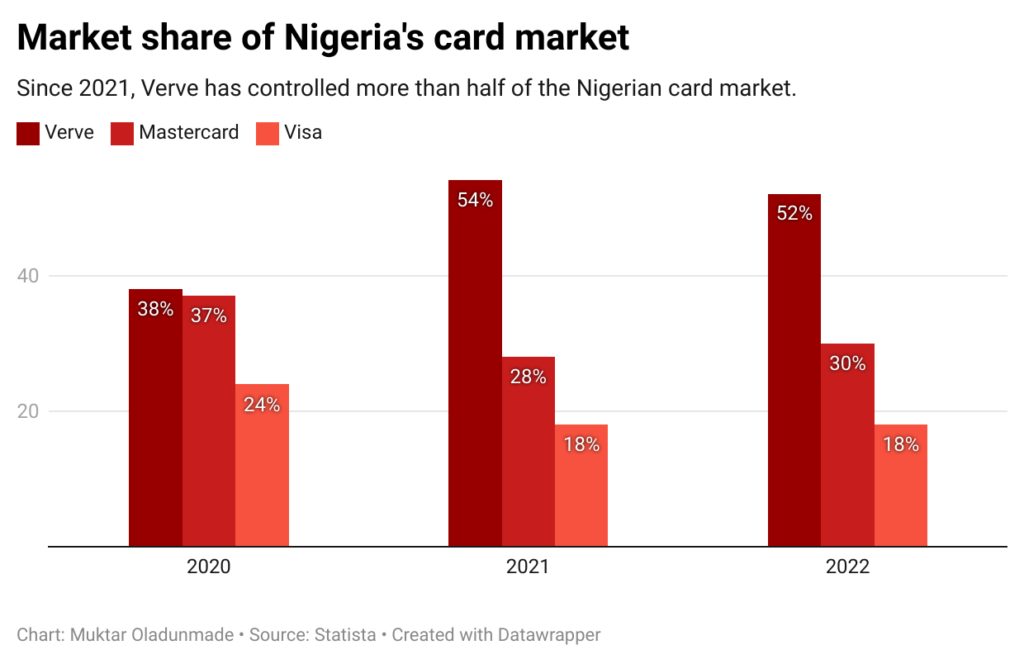

Chinese-backed fintech OPay has issued 13 million Verve cards, while Moniepoint has issued about 4 million. Since the Covid pandemic ended in 2021, Verve has controlled 54% of the Nigerian card market.

Moniepoint declined to comment on the figures.

Switching from the international card schemes — which charge in USD — has become popular following the naira’s devaluation, making FX-denominated bills more expensive.

Visa and Mastercard fees vary and depend on the financial institution’s size and region. The pricing strategy of these international card schemes is also complicated; Mastercard’s pricing guide is a 300-page document, said one financial industry expert.

Financial institutions must also meet requirements like a $2,000 monthly implementation charge, opening an offshore account, renewing their contracts annually, and collateral that runs into millions of dollars said three people with knowledge of card operations. International card schemes also charge Nigerian banks a fee for logging disputes on their resolution channels.

They also prevent non-banks from connecting directly to their card scheme, forcing fintechs to partner with commercial banks already on card schemes.

These complexities are driving the popularity of local alternatives like Verve and Afrigo despite heavy investment from Mastercard and Visa on the continent. Both companies have poured at least $700 million into the continent’s fintech industry to stay relevant.

Visa and Mastercard did not respond to a request for comments.

Besides the money, Verve and Afrigo make sense

The decision to switch to local card schemes is also connected to customers’ use of cards for local payments. With spending power under pressure because of inflation, the ability to make global payments, which the big card schemes offer, is useful to only a small percentage of customers.

“Majority of fintech customers use cards for POS transactions. They are not shopping on Amazon or online outside the country,” an employee at a Nigerian card scheme told TechCabal.

Nigeria is also facing its worst cost of living crisis in three decades, reducing customer spend and causing a drop in interchange — the fees merchants pay for card processing — a problem for fintechs that need a high volume of transactions to break even with cards.

Under Godwin Emefiele, the Central Bank launched Afrigo, a local card scheme, and said it could help banks save costs. Fintechs, now firmly in the scope of regulators after a six-week ban on onboarding new customers, are eager to get in the regulator’s good books and see this as an easy route, according to one person familiar with the talks.

The rise of the online transfer payment method has also meant that Nigerian fintechs are making products that facilitate bank transfers. Stripe-owned Paystack has launched two pay-by-transfer products in recent months as bank transfers represented 58% of its transactions in Nigeria in 2023, up from 28% reported in 2022. Those transfers offer better margins than card payments as the multiple processors involved in card payments are eliminated.

Besides the swing in customer behaviour, card operations require massive scale to become profitable due to logistics, manufacturing, technology, regulatory costs, and the risk of fraud.

These international card schemes have considered collecting their fees in naira, several people familiar with the talks told TechCabal.

But years of FX restrictions and $20 limits for global payments have made alternatives like virtual cards popular and may mean customers are indifferent about the switch. As long as the cards work at a store, restaurants, and POS stalls, it’s just another Monday.