Piggyvest has paid out over ₦1.1 trillion ($1.42 billion) to its customers since its inception in 2016. Its co-founder and CMO, Josh Chibueze, talked to TechCabal about how they did it and the challenges they faced.

Piggyvest, a Nigerian digital savings company, paid out over ₦400 billion ($519 million) in 2022, bringing the total amount of money it has paid out to customers since its inception in 2016 to ₦1.1 trillion ($1.42 billion). Josh Chibueze, a cofounder and chief marketing officer of Piggyvest, told TechCabal on a call that the disbursement represented only a fraction of the money saved with Piggyvest. “Our disbursement model means that this amount is money that people saved and requested. Only a few people withdraw their money. It represents the liquidity we had to return their money,” he said.

He added that the startup is now moving into the “money management phase,” where the company will offer credit to Nigerians. The startup would leverage its three licenses; a fund manager license from the SEC, a mobile money license from the Central Bank of Nigeria, and a microfinance bank license to achieve this, Chibueze said. “Right now, we have a savings and investments arm, which is Piggyvest, and a spending arm, which is Pocket app. So once we’re able to understand savings and investment patterns and spending, then we can build reliable data to be able to give you credit.” A mobile money license would allow Piggytech (the parent company) to issue account numbers through Pocket app and control a customer’s entire transaction flow.

Nigerians savings habit

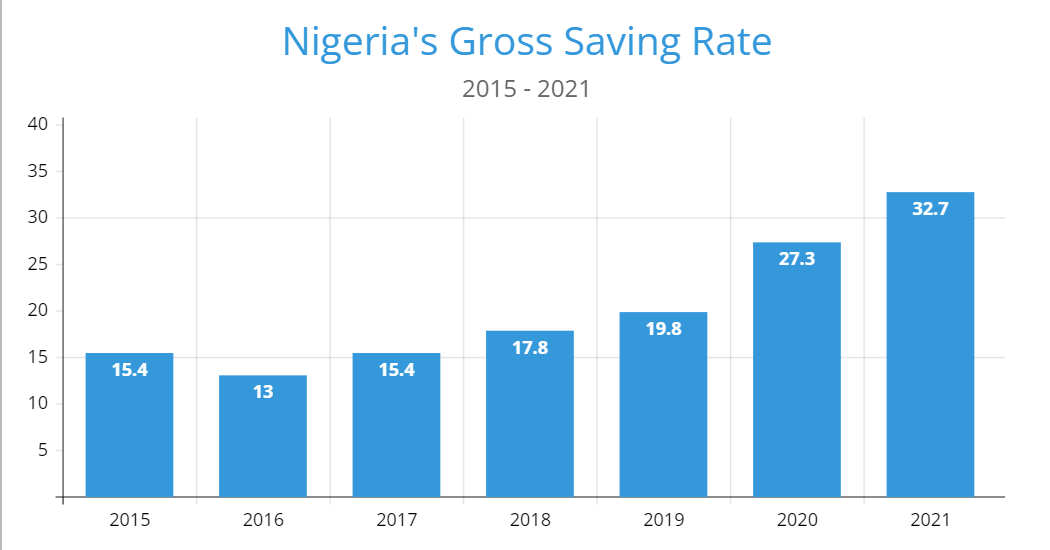

According to a report from the IMF, Nigeria ranks 11th in the sub-Saharan region for private savings. During the COVID pandemic, 42% of Nigerian households said their source of financing came from savings. However, for years, this saving culture was not incentivised, as Nigerian banks typically offered low interest rates of around 5%-7%. This led to Nigerians preferring to save their money in cash at home with piggybanks or opening bank accounts and not collecting cards to save money. To solve this, fintechs like Piggyvest and Cowryrise came onto the scene with a digital solution for saving money and higher interest rates. Their promise of higher rates made them appealing to Nigerians, quickly propelling these fintechs to prominence and creating a new business segment.

That business segment has since grown exponentially. Piggyvest, the market’s first entrant, now has 4.5 million customers, up from 53,000 in 2018, who trust their savings with the company rather than traditional banks. Chibueze said that the startup’s numbers can be attributed to a first-mover advantage, constant innovation, and fulfilling its business promise of instant access to funds on set withdrawal dates and interest. “It’s a simple rule in business, once you fulfil your business promise and you remain consistent, people will keep coming back and referring other people. We grew largely through word-of-mouth marketing. It was just in the last two years that we decided to do offline marketing. We only just incentivized referrals.”

Piggyvest’s path to profitability

According to Chibueze, Piggyvest became profitable “very early on” by being effective with capital and only relying on word of mouth and social media marketing to grow. He said that the startup only raised a $1.1 million seed round in 2018 to acquire its microfinance bank license and added that they were currently in fundraising mode.

For a fintech that specialises in savings, security has to be a prominent feature, but several media reports have detailed how Piggyvest customers have fallen victim to fraud. Chibueze told TechCabal that the startup has “one of the most robust internal tools for detecting fraud” and that with recent product and app upgrades, fraud would be a thing of the past. “We have also invested in cybersecurity awareness for our customers. I don’t think we’re going to have any of those issues anymore,” he said.

The co-founder also mentioned that operating in a low-trust environment like Nigeria and dealing with issues with third-party service providers and regulators were other problems that the startup faced. “We struggled with regulation because innovation was faster. We had to take time to explain to the regulators before we could get all of these licenses.”

This year, the Nigerian economy has been hit with the triple whammy of cash scarcity in the first quarter, a petrol subsidy removal and the floating of the exchange rate in the second quarter. When asked how this has affected Piggyvest’s users and their saving patterns, Chibueze told TechCabal that he had noticed an increase in the income capacity of Nigerians. “What is happening right now is that people are having to spend out of their savings, which reinforces the need for platforms like ours to exist. [Another thing] people are doing right now is increasing their income capacity to be able to earn more so that they can afford the expenses they already make,” Chibueze said.

Have you got your tickets to TechCabal’s Moonshot Conference? Click here to do so now!