With 2023 now behind us, we look back on a year marked by strong economic headwinds and market upheavals. A cursory look at funding numbers shows that 2023 was a mixed bag. Venture capital (VC) funding fell by 41.7%, quarter-on-quarter, going from $916m in Q2 to $499m in Q3.

In 2022, funding raised by African startups peaked at $5bn. As of November 30, 2023, this figure stood at $3.246bn, which, so far, shows a stark 36% dropoff from last year, highlighting the difficulty investors faced in raising funds in 2023. The number of $1m+ equity deals also waned significantly from a high of 125 in Q1 2021 to 42 in Q3 2023.

Despite the low numbers, 2023 had some positives. Notably, a new African unicorn emerged in the shape of MNT-Halan, the Egyptian fintech startup. Firms like Partech—via its Africa II fund—and M-Kopa raised money above their expectations, exceeding $250m each. Flutterwave made strides towards its goal of an initial public offering (IPO) after being cleared of financial misconduct in Kenya, and Nigeria’s central bank shifted its posture on crypto to adopt a crypto-friendly policy stance. So, what trends should we look out for heading into 2024?

- Funding downturn and cost-cutting measures likely to remain

In 2023, fintech, logistics, and e-commerce platforms, which traditionally attracted heavy funding, witnessed a slowdown marked by downsizing and, in some instances, shutdowns. In Q1 2024, startups will likely continue cost-cutting measures and refocus on unit economics in an uncertain funding environment. This could be anything from localizing costs and scaling back operations, raising funds in local currency, revising medium to long-term goals by prioritizing survival, and reducing exposure to markets susceptible to foreign exchange volatility. Recent trends point to this, as we have seen companies like Paystack scaling back its activities outside Africa and Jumia shutting down its food delivery business. Resilience will be the watchword.

- Consolidation via mergers and acquisitions

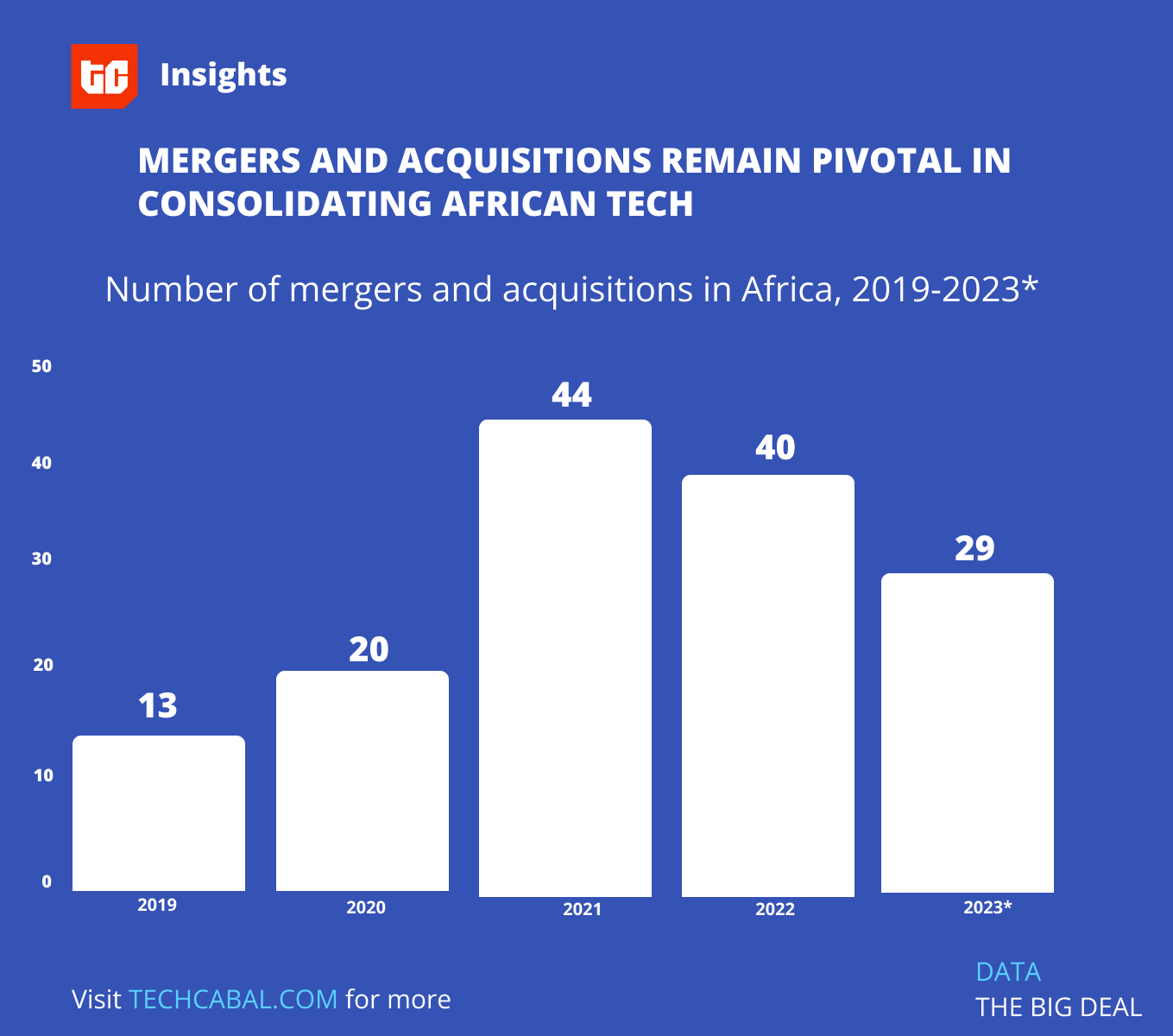

Seven mergers and acquisitions deals (M&A) led the way in African tech at the beginning of 2023, valued at ~$710m, with Biontech the pacesetter by acquiring AI firm Instadeep for $680m. More recently, there have been merger talks by B2B platforms Kenya’s Wasoko and Egypt’s MaxAB, which, if finalized, would make it the largest merger within the e-commerce subsector. So far, there have been at least 29 such deals, although most have been for undisclosed amounts.

Market dynamics, capital availability, and startup agility drive M&A in Africa, often initiated by larger companies looking to acquire earlier-stage companies on the path toward going public. The presence of numerous small and medium-sized companies operating across diverse regions and sectors creates a fragmented market. By coming together, they can be better equipped to compete in the global market and attract investments. Expect such collaborations in 2024.

- Artificial Intelligence to gain wider application

Beyond its widespread use in large language models (LLMs), there will be more integration of artificial intelligence (AI) across diverse sectors ranging from payments to health infrastructure. However, digital commerce platforms are likely to adopt AI tools using surgical precision rather than implementing them on a sweeping scale.

Africa’s AI market is projected to reach $6.9bn in 2024. Most of it will be powered by machine learning, natural language processing, and autonomous and sensor technology.

- African investors to maintain cautious optimism

A survey by the AVCA on the expectations of 88 African investors, including Limited Partners (LPs) and General Partners (GPs), noted that 85% of LPs plan to increase their allocation to private capital in Africa over the next two years, with impact (77%) and investment mandate (68%) identified as their primary reasons. Data from our Founders’ Outlook Survey revealed that 65% of investors maintain an optimistic outlook for the African startup ecosystem in 2024.

The optimism does not appear misplaced, as the Financial Derivatives Company projects that inflationary pressures will ease across Africa, falling from 18.6% in 2023 to 16.1% in 2024. The Economist Intelligence Unit (EIU) predicts that “Africa will be the second-fastest-growing major region in 2024, with most countries increasing economic growth compared with 2023. East Africa is expected to champion African growth.” However, the EIU also says many African countries will feel the weight of excessive debt and a heavy repayment burden in 2024.

- Possible shifts in regional preferences

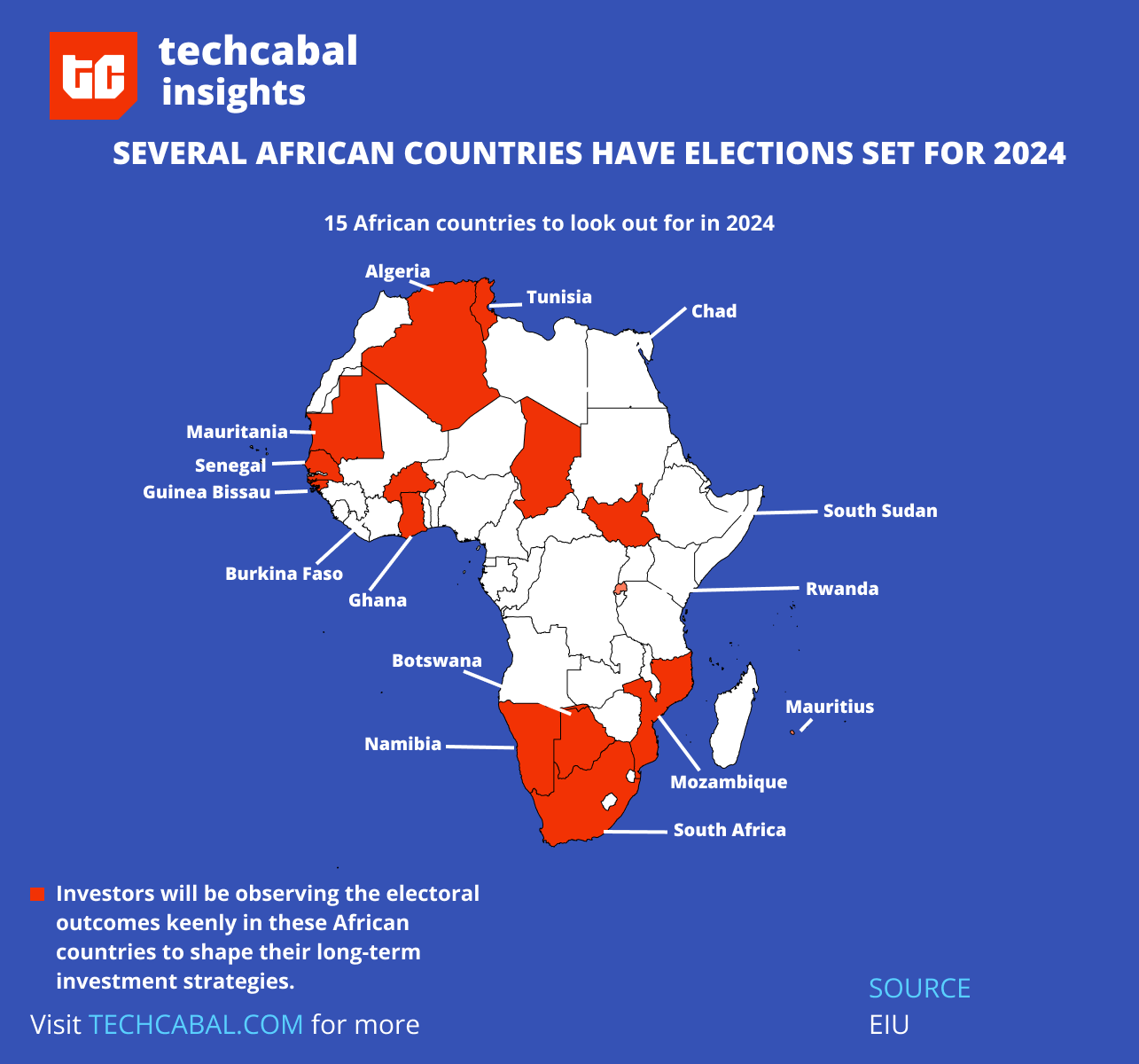

In 2024, investors could reevaluate their regional strategies in response to changing macroeconomic and political conditions. Per the EIU, fifteen African countries have elections next year, and investors will observe their outcomes keenly. Elections are fraught with risk, especially in regions where armed conflict is rampant. The EIU notes that elections in Algeria, Egypt, Ghana, and South Africa will add to political risk, which could have long-term implications on where investors put their money.

The AVCA survey revealed that LPs favored investing in West Africa while GPs leaned towards East Africa. The data aligns with this: between 2019 and 2023, per The Big Deal, there were over 700 recorded deals worth $1m or more. West Africa led the pack with 246, East Africa with 175, Northern Africa with 160, Southern Africa with 147, and Central Africa with 14. Depending on the degree of confidence, the numbers could realign with investors becoming more risk-averse. It’s all “wait and see” going into 2024.