Open banking, which allows banks to share customer data consensually with fintechs, is believed to be a game-changer for Nigeria’s financial space. Yet the country’s banking regulator, the Central Bank of Nigeria, is moving slowly on its adoption.

Three years ago, Nigeria’s Central Bank released the first draft of a regulatory framework for open banking. It was a pivotal moment, and Nigeria enjoyed the privilege of becoming the first African country to adopt the practice last year.

It was commendable work from a regulator that’s often on the receiving end of criticism from the public. Yet, months after moving quickly to adopt a framework, the apex bank has stalled on introducing a much-needed standard, keeping open banking in theory.

A standard will ideally create a uniform way of transferring data through APIs and a public register of all the participants in open banking. Standards are very important. For example, before the IBM standard, the personal computer industry operated multiple user interfaces, making PC parts very expensive and out of reach for most people.

The IBM standard helped create the uniformity that the modern PC industry was built on. Open banking needs this uniformity and the CBN’s apparent lack of urgency towards creating this standard risks delaying a pivotal step towards financial inclusion.

How can open banking change Nigeria?

Take lending as an example. Loans contribute significantly to the income of financial institutions, and to ensure that they are repaid, banks like to have data points on the customers to make informed lending decisions. So far, bank-led lending has resulted in low credit penetration, with as much as 70% of bank account holders locked out from accessible credit.

In the last few years, several fintechs have entered the credit market to fix this despite having limited data. The result has been a mixed bag of sub-prime loans and predatory collection methods.

With open banking, lending fintechs would receive data (transaction history, consumption patterns) from banks—there are at least 120 million bank customers in Nigeria—to assess creditworthiness and also help create a much-needed credit score for Nigerians.

Fintechs can also create new types of personalised financial products backed by data, as Nigerian banks are not incentivised to innovate given that the majority of their profits come from non-banking sources. In what was a record year for profits, most banks made money from the devaluation of the naira last year, with minimal income from core banking interests or new products.

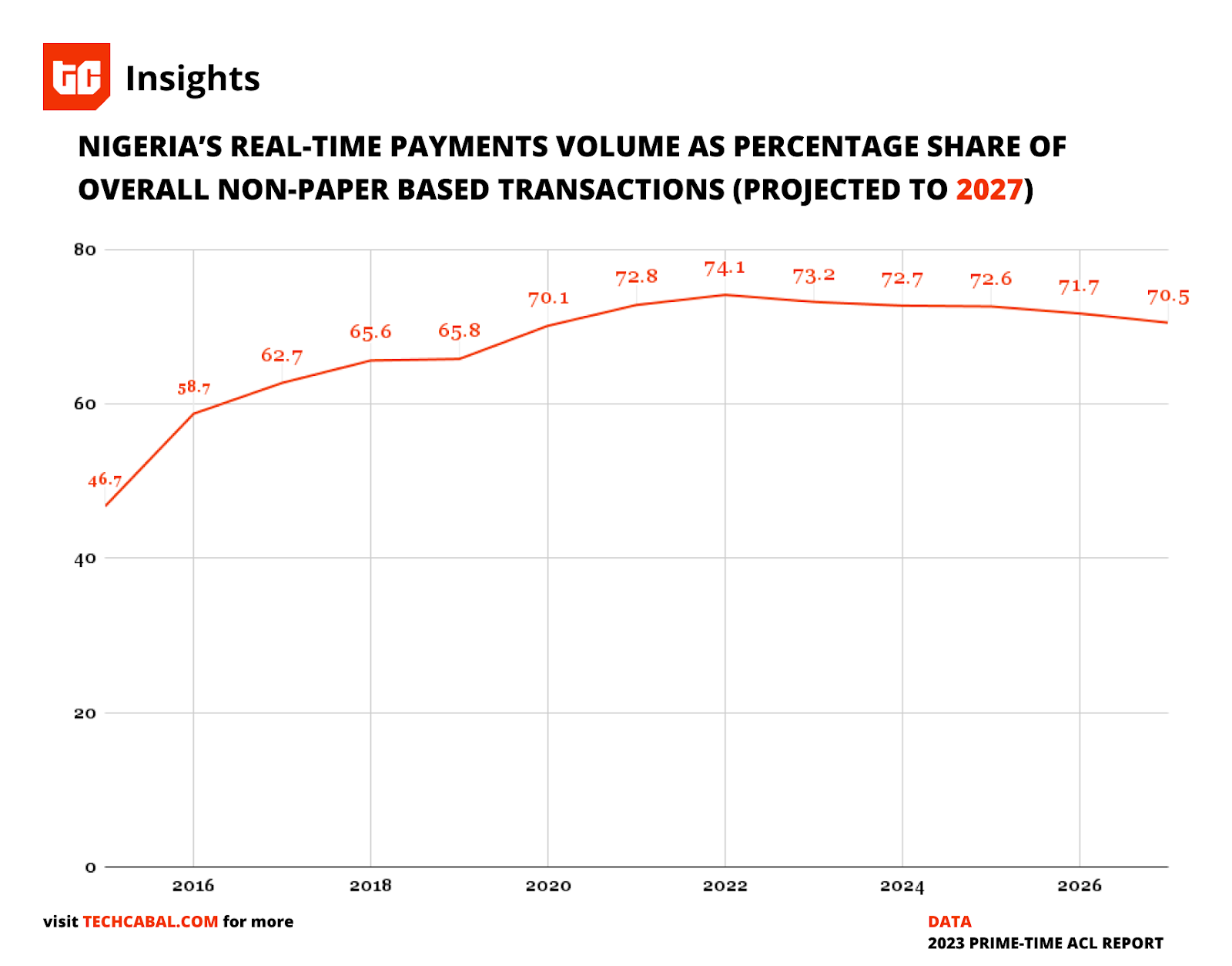

Nigeria is already a prime market, with startups like Okra, Mono and Stitch offering innovative solutions similar to open banking due to demand. Real-time payments, a crucial enabler, are booming. Last year, Nigeria’s largest real-time payment infrastructure processed 9.6 billion transactions, according to data seen by TechCabal.

Chart by Stephen Agwaibor/TC Insights

Should the CBN regulate open banking?

There are concerns that because open banking relies on technology, an ever-changing field, the CBN should not regulate it; instead, it should be regulated by Nigeria’s data protection agency, the Nigeria Data Protection Commission (NDPC), as data privacy is a foundational pillar of open banking.

“The central bank’s job is to implement policies, not technology,” said David Peterside, the co-founder of Okra, an open banking startup.

The CBN’s guidelines from last year focused on two main issues; availability of technology and security. Peterside added that the CBN should instead focus on making the banks and API providers partner because the CBN’s regulatory burden would require banks to build APIs, inflating costs for the banks. Large British banks have spent more than £500 million on implementing open banking. With startups already providing similar services, banks can forgo this bill.

But given the sensitivity of financial information that would be shared, there is no ideal way that the CBN would not be involved in a regulatory capacity, said Ikemesit Effiong, head of research at SBM Intelligence, a Lagos-based think tank.

“Nigeria is a bank-led financial system, so it will not be unusual for the CBN to give out the regulations. However, violations will be [the responsibility] of the data protection agency,” Babatunde Obrimah, chief operating officer of the Fintech Association of Nigeria, told TechCabal. He added that because banks, fintechs, and mobile money operators obtain licences from the CBN, it is the only body to regulate them properly, but interoperability must be ensured.

What’s in it for the banks?

Right now, there is fear in the banking industry that the implementation of open banking would inevitably lead to more competition. “It’s the same pie that everyone is eating out of, and you don’t want anyone to eat into your part,” is how an industry insider puts it.

This is, however, an unfounded fear because most Nigerians use legacy banks and fintechs, Effiong said. A similar example of user inertia is how the Nigerian Communications Commission (NCC) introduced SIM porting a decade ago, allowing customers to switch network providers easily, but less than 2% of customers have ported since.

Revenue sharing, the prospect of mergers and acquisitions, and the CBN’s backing are some of the ways banks can be incentivised to share their customer’s data, Nnamdi Ifechi-Fred, a digital economy analyst at Stears, told TechCabal.

Public awareness can spur the CBN

Public awareness of the benefits of open banking can spur the CBN to finalise open banking. The United Kingdom became one of Europe’s leaders in open banking by increasing awareness of the benefits of open banking. Within two years, 11% of British consumers were active users of open banking.

Since India’s apex bank introduced the Account Aggregator (AA) framework, which facilitates secure financial data sharing via APIs, about 60% of Indian businesses see open banking as a gateway to acquiring consumer-consented data. It has now become a staple in India and is powering the next stage of open banking—open finance.

This can be replicated in Nigeria, but the CBN’s lack of a uniform standard is severely halting this progress. Fintechs have already integrated and partnered with banks, but the current reality of open banking cannot power the scale that would bring change to Nigeria. Why is the CBN stalling?