The premise of a Venture Capital (VC) funding pitch is peculiar: two parties, usually meeting for the first time, sit down for coffee. The pitch maker clicks through a PowerPoint deck, building the promise of an under-construction, alpha-stage product. The pitch taker probes personality fit and leadership competency, all the while assessing the ‘it-factor:’ the secret sauce of successful partnerships, with thousands, or even millions, of dollars on the line. Talk about a stressful, high-stakes coffee.

As a Venture Capitalist, I’ve dedicated my career to getting promising technology funded in Africa. I’m bullish on the innovative solutions, young leaders, and multi-sector opportunities presented by African markets. However, there are misunderstandings keeping capital sidelined and promising startups unfunded – and part of my mission is to bridge the gap of understanding between the two parties. Sound relationships between investors and entrepreneurs are essential to ecosystem success: even secret sauce needs good suya.

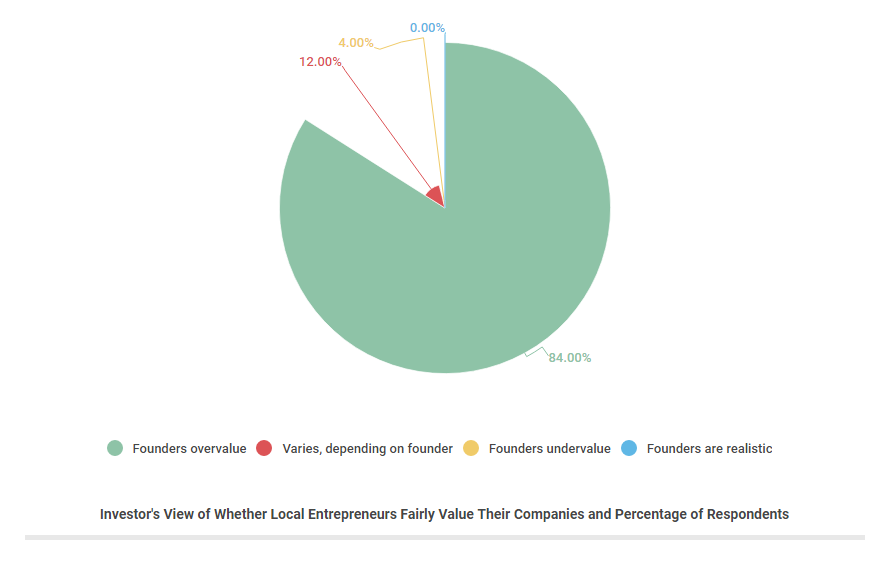

In early 2016, I sent surveys about valuation to 28 early-stage investors across Africa. Founders and funders win when transparency around appraisal expectations are mutually clear.

One look at the results and something was abundantly clear: Pan-Africa VCs universally believe that founders have “unrealistic valuation expectations and overvalue their companies”.

This post isn’t about taking sides in the investor versus founder valuation debate. These conversations are highly circumstantial and driven by the day’s market realities. Instead, this article is addressed to founders and aimed at raising awareness of VCs’ perspectives of valuations. With awareness comes an opportunity to ally funders’ valuation perspectives to the foundation of your negotiation.

VC Belief #1 – Your valuation is a reflection of you.

Valuation for early-stage startups is driven by defensible growth prospects, the go-to-market strategy to capture these opportunities. Too high and you make a statement about yourself; a pie-in-the-sky valuation reflects a lack of rigor, market intuition and experience. Nearly 60% of investors said their greatest fear in funding an African startup is the quality of management team. Valuation is a mechanism built on the investors’ market insighta and honed by their experiencea in witnessing the rise and fall of startups at various stages of life. Recognizing and incorporating this into your valuation to ensure alignment may assuage funders’ concerns about the reasonability of your management potential.

It will also be wise to understand the initial starting place where an investor may benchmark the valuation of your company. 50% of respondents admit they have targeted valuation bands depending on a startup’s stage of life. From the moment you sit down with an investor, your startup is being categorically shuffled and valuation assignment is happening in real-time. One West Africa VC stated unequivocally:

“…for idea stage (or pre-revenue, no traction), valuation is $0. Early traction [may be valued between] $100k – $500k; ability to show real topline growth [may put valuation at] $1M+…”

You should absolutely emphasize your value proposition and highlight the competitive differentiators of your company. However, be ready to accept the appropriate banded limitations of valuation assignment. And immediately, you will foster an immediate sense of trust within the essential founder-funder relationship moving forward.

VC Belief #2 – Bigger is not always better.

“Bigger is better” goes the mantra but with fundraising startups, the saying is less meaningful. Aggressively negotiating to the ceiling of a valuation conversation may feel like a win, but if subsequent rounds of funding are required, trouble lurks.

Over one-third of survey respondents called out encountering a down round or lack of comparable funding data as a major fear.

VCs recognize the disadvantages of raising capital at a lower valuation in a future fundraise: Investors buy momentum. Exit opportunities and funding from A-list VCs get compromised when growth (or that shameful word: hype) stalls. A VC that does invest will notice the vulnerabilities that uncompetitive positioning ushers in and make it their responsibility, and reward, to get the company back on track. Expect them to demand concessions, negotiate previous investors’ preferences and aggressively influence management or business model changes.

Down rounds also motivate your competition. Your susceptibility will be leveraged publically. Employees may be poached, stinging marketing campaigns could get launched and, in general, your target audience may second-guess your commercial viability.

Because valuation is art, not science, founders need to recognize that investors discount valuation based on the likelihood of their greatest fears coming true. Target valuation in-line with conservative, defensible expectations of profitability achievement, and raise what you need, when you need it.

VC Belief #3 – Activity is not achievement.

Recognizing where investors ascribe value, ensures focus on activities that upgrade valuation potential. For early-stage companies, traction is king.

More than 60% of surveyed investors responded that their primary means of establishing valuation is a market multiple approach – simply valuation multiple on revenue or profitability relative to what they have seen realized by companies (through successfully raised rounds or exits) comparable to yours based on industry, geography, and stage. 75% of answers referenced a market multiple and discounted-cash-flow methodology together.

A discounted-cash-flow methodology will take your company’s expected cash-based returns over a future period of time, including an expected exit event (typically again using a market multiple based on future financials), and discounting the sum of all of those by a required rate of return, to get a value today. This is more complicated, and I personally put less weight on this method for early-stage companies, as the growth trajectory, capital needed in the company, and potentially even the future business model is unknown – still, it’s good to understand how this works as it is clear it weighs heavily in many investors’ projections.

Fundamentally, this means that the investor’s view of value rests on your ability to generate cash – not having a brilliant idea on paper, a team of Ivy League MBAs, news headlines, or enterprise MOUs.

If you can demonstrate traction through affordable customer acquisition within large addressable-market, you’ll have VCs licking their lips. This requires a sound business model and a path to scale.

Investors are willing to pay in-line with the market, leading them to base their valuations on performance indicators influenced by the startup’s peers. Since absolute prices cannot be compared from company to company, investors will gravitate toward specific, logical and universally recognized data points. (I’ll address more on these specific data points in a future post.)

The net of the story is always the same: a maniacal focus on activities that generate sound financial results will set your company apart and drive a compelling valuation. As a founder, take note. It is not just the cordiality of your coffee conversation that is at risk but your company’s future.

VC Belief #4 – Make the unknown known.

72% of the investors I surveyed admit they apply a general discount to African companies.

For many investors, there might be an additional level of risk aversion coming from not understanding the intricacies of the market or having people on the ground to provide oversight. Yet even for those of us sold on the continent’s opportunity, we have to admit that even in Africa’s most promising markets, challenges around infrastructure, human resources, regulatory environment and exit opportunities remain.

As one notable investor reflected:

“In Africa, size of market or opportunity is not usually the issue. Execution is. Many people have good ideas but lack high quality execution. In fact it almost seems as if there is an inverse relationship between the ability to generate ideas and the ability to execute on ideas. […] Start up companies must show a good mix of people who have great / good ideas and people who are Thoroughbred executioners (for lack of a better word – but frankly as investor, that’s what I want – someone with a killer instinct on execution). “

And another:

“For local early-stage companies we use higher discount rates to factor in perceived risks […], based on factors such as the impact of inflation, customer default, industry risk, regulatory risk, etc.”

As you prepare to meet investors, can you obviously explain your execution plan around the risks inherent in your geography and within the business model you employ? As equally important as the narrative of how you’ll scale your company, is the narrative of how you’ll manage risk.

To close, let me leave you feedback from an East African angel investor. His words are a sweeping summary of what matters most:

“…my focus […] is finding a loyal, growing user base that needs and loves the product and is willing to use it or pay for it repeatedly. Also a strong management team that understands the customer, where they are, and how to get to them.”

What he is saying is simple. Attractive valuation is a byproduct of a valuable company. And a company is valuable when competent, strategic leadership gets a killer product or service in front of a large market that can’t get enough.

We will continue the valuation conversation from the entrepreneur’s perspective in our post next week Wednesday. Stay tuned!