M-Changa is a fundraising and crowd funding platform that seeks to enhance user experience and performance by providing secure and communication and record keeping capabilities for unprecedented end to end transparency. M-Changa has integrated mobile money and credit card payments, SMS, email, social networks and geo location.

M-Changa co-founders, Kyai Mullei and David Mark, are effectively enabling indigenous organized giving or ‘Harambee’ (Swahili for ‘fundraising’) via their mobile money crowdfunding platform. They are now looking for USD 1 million in investments to expand.

In an interview with VC4Africa, the entrepreneurs revealed the reason why they are now sourcing for investors and more. The founders think that M-Changa has reached the size where expansion is necessary and to expand they would need investors.

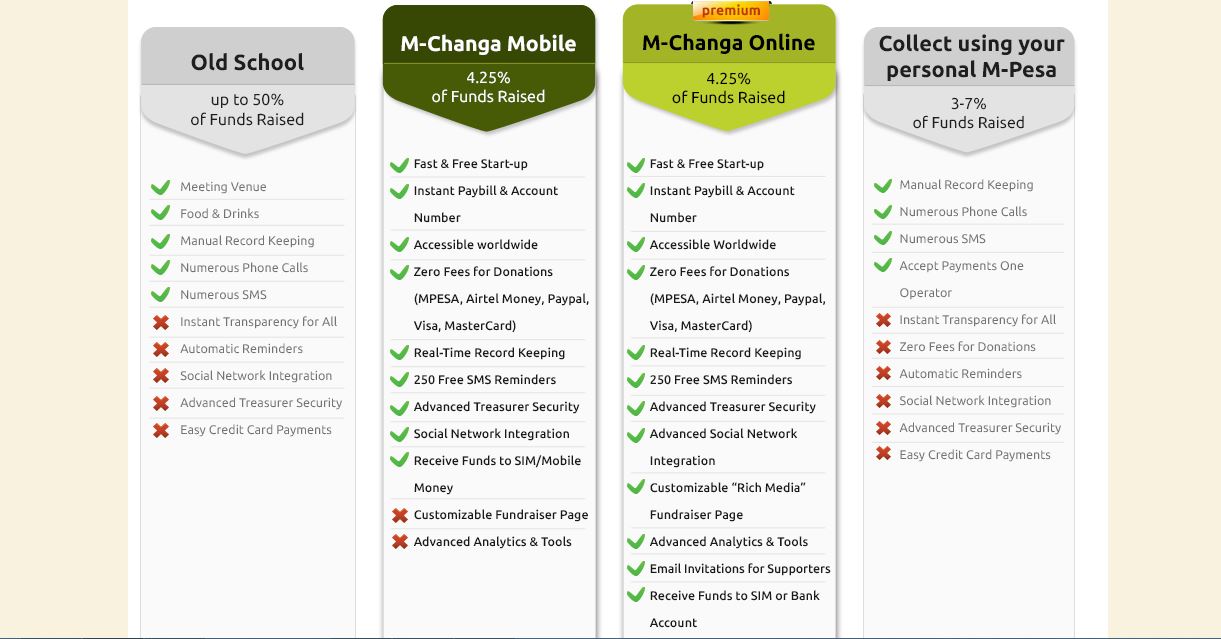

“M-Changa’s story is a growth story. With over 2,000 fundraising campaigns, over 13,000 supporters and close to 50,000 customer interactions, M-Changa is the biggest player in the digital Harambee space. The cross section of platform usage is extremely wide and mirrors trends demonstrated in all major research in the area of philanthropic giving in East Africa and Globally. This unique positioning allows us the potential to steer the national and regional dialog on transparency and digital fundraising. The evolution of M-Changa from launch a year and a half ago has been tremendous. Because of market demand M-Changa has evolved from a purely SMS based product to a hybrid one that allows you to start and manage a fundraiser online. M-Changa now gives a richer fundraising experience on both platforms and has significantly expanded its market potential. Our business model has also simplified tremendously as we opted for a direct monetization model (4.25% of funds collected) as opposed to client action-based charges.”

Last year, M-Changa participated in June Cohort, VC4Africa’s acceleration programme, 8 months into the launch of the product. They received positive feedback from several investors while they developed their product, and the exposure resulted in several invites to partake in and display their product in numerous forums and conferences across Africa and North America, and in several local and international partnerships being formed.

After running extensive marketing campaigns to figure out the best way to get the word out about M-Changa, partnership with the Microsoft 4Afrika Affordable device program has been their most recent success. M-Changa is one of two financing partners for the program that aims to give access to affordable educational devices to 100,000 students and teachers in Kenya. Students and teachers will be able to start fundraisers on M-Changa and buy subsidized devices at select dealers once they have raised the needed funds.

On the issue of how M-changa would compete with the international crowdfunding platforms, the founders expressed confidence in the distinction of culture, collection from family and friends, that forms the basis of their product, as well as the fact that unlike Kickstarter and co, M-Changa is also the only product combining mobile money transactions with smart SMS-based fundraising functionality.

“M-Changa is a culture-based product that reflects the Harambee-culture in Kenya and other countries in East Africa. The distinction is important. Harambees rely first and foremost on family networks and then friends. The general public (or anonymous crowdfunding as with Kickstarter and other platforms) is the last resort for anyone doing a Harambee. This difference greatly impacts the propensity to give, how often one gives, as well as the approach for requests for help. M-Changa is also the only product combining mobile money transactions with smart SMS-based fundraising functionality. The platform has been designed to mirror the real-life considerations of Harambees as closely as possible. For example, M-Changa has a treasurer feature that allows for multi-person custody of the funds raised in a campaign.”

For people who wonder why they are starting a fundraising campaign for their expansion at this moment, because it does seem like they have a lot going for them, the founders say that while they are a revenue generating company, they need growth capital from investors preferably with strong connections and experience in the mobile payments industry and banking or related financial sectors. Much of the past 6 months was spent on cultivating strong partnerships, but they recognise that M-Changa’s growth relies on strong public awareness, which can be created by top line advertising and client relationship managers. They pointed out that since the Angel investment of USD 35,000 they secured two years ago, they have self-funded the company since.

One of the payment platforms in use on M-Changa is MPesa. This would make one wonder if building their service on mobile provider, MPesa will not make them susceptible to competition from them, and others. But the founders maintain that their diverse usage story, which includes credit card payments, shields them from competition from mobile providers in general; not to mention the constant evolution of their product intelligence.

“We have an increasingly diverse usage story that we feel protects us from direct competition with mobile providers. Our service is built to straddle four different payment platforms; MPESA is only one payment solution out of the four. Credit card payments now constitute over half of all incoming payments – this has been a result of the high growth of our online product which is used to target diaspora and high value philanthropic transactions. Our product intelligence has evolved significantly since inception and the nuances based on market research and client usage and feedback is difficult to replicate. Finally, we are constantly evolving our product to stay ahead of the competition. In the mid-term, expect to see increased use of Geo-location, deeper social network integrations, and smart fundraiser network creation that relies on accumulated data on patterns of giving. With regard to Chamas, they typically involve transactions that require managing revolving financial kitties with periodic draw downs, interest charges, partial draw downs, and penalties.”

2016, they say,should see complete full scale piloting and launching of M-Changa in at least two East African countries. And by the end of 2017, the founders project that they will occupy 10-15% of the total estimated market size for philanthropic activity in Kenya alone, which is estimated at USD 1500 million.

Photocredit: VC4Africa