|

|

|

|

|

|

|

|

in partnership

with

FLUTTERWAVE & NET AFRICA |

29.10.2020 |

|

|

|

|

|

Good morning.

In today’s edition:

-Telecoms

-My Life In Tech

-A conversation with startups

|

|

|

|

|

|

|

|

|

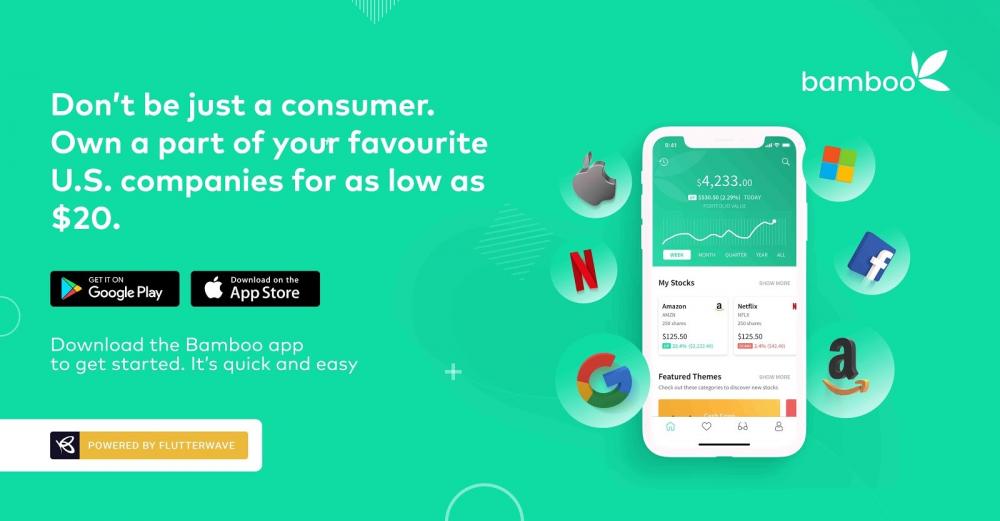

Bamboo, a Flutterwave merchant, gives you unrestricted access to over 3,000 stocks listed on the Nigerian stock exchange and U.S. stock exchanges, right from your mobile phone or computer. With as little as $20, you can create and fund your Bamboo account with your Dollar or Naira cards and through bank transfers. Start buying and selling shares or stock bundles (called Exchange Traded Funds) in just a few taps, begin here.

|

|

|

|

|

|

|

|

|

Two days after Airtel Africa released its H1 2020 results, MTN Nigeria has also released its unaudited results for the first nine months of 2020.Here are the metrics that matter: Income:

- Revenue grew by 13.9% to N975 billion

- Earnings before interest, tax, depreciation and amortisation (EBIDTA) grew by 9.1% to N497.9 billion

- Profit before tax declined by 0.6% to N211.6 billion

- Profit after tax declined 3.3% to N144 billion

What jumps out? The contribution of voice revenue to total service revenue

has dropped from 73% in 2019 to 67% in 2020. This isn’t surprising, given that voice revenue is expected to continue to reduce across Nigeria as more people use internet enabled options like Whatsapp calls.

Data is where it’s at: The contribution of data revenue to total service revenue jumped from 18% in 2019 to 25% in 2020. It is the

result of MTN’s investment in expanding its data service infrastructure within Nigeria.

Subscriber data (Q3 2020):

- Mobile subscribers increased by 3.9 million to 75 million

- Active data subscribers increased by 1.7 million to 30.7 million

- Fintech subscribers increased by 1.2 million to 3.4 million

The bottom line: While MTN

Nigeria’s revenue continued to grow, its profits declined because of Nigeria’s challenging business climate. In its outlook for full year 2020, MTN Nigeria says it will expand 4G coverage and broaden rural connectivity.

It is again a nod to industry realities about a future where data, not voice drives revenue.

|

|

|

|

|

|

|

|

|

|

|

My Life In Tech is putting human faces to some of the innovative startups, investments and policy formations driving the technology sector across Africa.

Who

did Kay speak to this week? Uzoma Dozie, the former CEO of Diamond Bank and the present CEO and co-founder of the fintech startup, Sparkle.

Sparkle’s mission is to help its customers connect their finances and lifestyle.

Here are some of Kay’s thoughts: “Digital and legacy banks have been in stiff competition since legacy financial institutions started showing interest in playing significantly in the fintech space.

“Asides mobile applications and USSD options, banks like Guaranty Trust Bank where Dozie began his banking career are aggressively pursuing their fintech development to rival fintech companies who do not come with the restrictions of legacy

institutions.”

What did Uzoma say? “The more digital transformation we have, the better it is for the end users and the economy,”

“How they [legacy institutions] get from point A to point B is where the story is. [But] Doing it is actually

harder than saying it. It took me 12 years to change people to retail.”

Where can I catch the full conversation? Here!

|

|

|

|

|

IN CONVERSATION WITH STARTUPS: OkHI

|

|

|

|

|

If like Timbo Drayson, you worked at Google and led the launch of Google Maps across emerging markets, you might have stumbled on an interesting problem.

Millions of people in Africa have no physical address.

In Liberia for instance, there is no functional address system. It makes getting deliveries difficult. For financial institutions, verifying the address of customers is hard work.

In response to this problem, Drayson founded OkHi, a digital addressing startup in 2014.

The solution: OkHi uses a combination of GPS, picture, text instructions as well as name and phone numbers to ensure that people can own their addresses.

Where Google Maps focuses on places, OkHi focuses on people. So its customised digital address becomes more accurate the more you use it to get a delivery done or verify your latest bank account.

It has interesting uses for businesses. If a delivery person makes a delivery to a residential high rise, an

OkHi digital address can tell that delivery person the recipient’s floor as well as his phone number.

It means it is pretty useful for bank verification, mobility services and logistics companies.

A timeline: Launched in Kenya in 2014, the startup raised $750k from investors in a seed round in 2015 and said it had mapped 100,000 locations in Nairobi. The startup has been out of the news cycle since then.

The Present: Last month, OkHi raised $1.7m from the UK Angel network, its first major appearance in the news cycle in a while. So I reached out to Galen Crawley, the company’s CCO to talk about what the new funding means for the business.

One of the most interesting

points in our conversation was hearing about a partnership with Interswitch helped influence OkHi’s decision to move to Nigeria.

In Nigeria, it will look to work with digital banks, mobile money agents, banking platforms and mobile lenders. It hopes to help them verify their agent network remotely, increase debt collection success and help with faster onboarding.

Opportunity: OkHi is looking for a Nigerian ex-founder of a tech startup to run its Nigerian operations. Look up them on LinkedIn.

|

|

|

|

|

SURVEY

Financing is a tough job for SMEs. In Nigeria, chances are it’s even tougher. TC Insights is trying to understand this financing problem, but more importantly, proffer a solution.

So, if you own a small business or startup in Nigeria, please fill this survey

|

|

|

|

|

SHARE THE TC DAILY!

Did you enjoy today’s newsletter? Then share it with your network and call it your good deed for the day!

We’re not trying to be like that band you discovered two years ago but you haven’t put anyone onto. Sharing is caring!

If this email was forwarded to you, subscribe here.

|

|

|

|

|

|

|

|

|

|

|

Share TC Daily with your friends!

|

|

|

|

|

|

|

Copyright © 2020 Big Cabal Media,

All rights reserved.

You are receiving this email because

you signed up on TechCabal.com

Our mailing address is:

Big Cabal Media

18, Nnobi Street, Animashaun, Surulere, Lagos

Surulere 100001

Nigeria

Add us to your address book

Want to change how you receive these emails? You can

|

|

|

|

|