|

|

DECEMBER 13, 2020

This newsletter is a weekly in-depth analysis of tech and innovation in Africa that will serve as a post-pandemic guide. Subscribe here to get it directly in your inbox every Sunday at 3 pm WAT

|

|

|

|

Traffic in Lagos was hellish this weekend. People spent six hours on trips that take one hour in normal times.

My theory is that IJGBs – our dear cousins and aunts returning briefly to Nigeria for the holidays – are overburdening our tiny roads by throwing their weights about town.

My theory is very baseless though and, honestly, we shouldn’t be picking fights with IJGBs knowing the crucial role they play in our economy.

Remittances from Nigerians in diaspora kept families and businesses liquid during the pandemic, and will be more indispensable as the country slips into a recession.

How do we get our faves to remit more please?

In this edition, we spotlight the Central Bank of Nigeria’s recent moves on diaspora remittances as a march towards harmonizing/tracking the inflow of dollars into the financial system.

But first, please subscribe to this newsletter if you are yet to. And find all previous editions here.

|

|

|

Make it rain, but in dollars

Three weeks ago, the Central Bank of Nigeria (CBN) published a two-page circular with a surprising update.

Basically, when someone abroad sends dollars to a beneficiary in Nigeria, the money will no longer be received in naira.

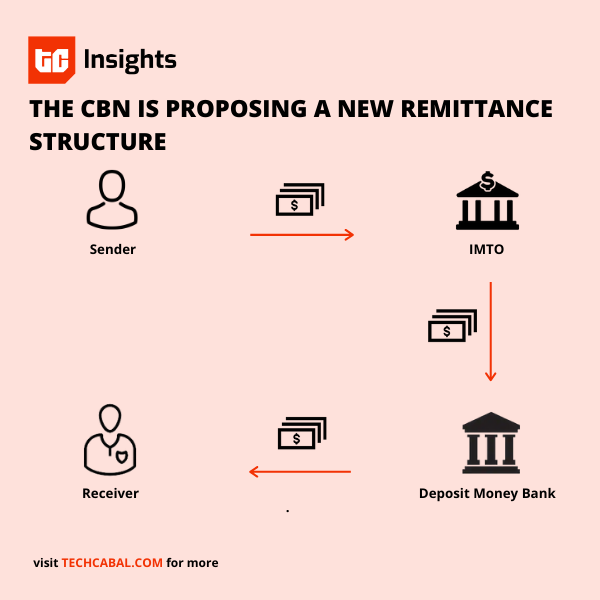

Beneficiaries are now to receive the remittance in dollars either in cash over the counter or in their domiciliary accounts. Each beneficiary decides what she prefers.

The notice was directly for CBN-licensed international money transfer operators – Flutterwave, Moneygram, RIA, Western Union, etc.

They are to ensure this new policy takes effect. International money transfer operators (IMTO) that keep paying beneficiaries in naira instead of dollars invite the wrath of the apex bank and may lose their license to operate.

Because a lot of the CBN’s recent announcements have appeared rushed and high-handed – for example, controversial punishments for failed direct debits – many people were uncertain what to make of this.

On December 16, CBN published a directive excluding mobile money operators from the remittance process. MoMo operators are to disable their wallets from receiving remittances from IMTOs.

The same document bars payment processors and payment service providers from integrating with IMTOs as far remittance is concerned.

The glue binding these two is in the update published on December 2. IMTOs are to make sure they pass the dollars meant to be remitted to beneficiaries through commercial banks. These banks have also been ordered to close all IMTOs naira accounts.

In other words, the CBN is trying to create a linear remittance architecture that looks something like this:

|

|

|

Why is the CBN rooting for the dollar in this way?

Aloy Chife who operates Sanaa Capital, an IMTO, says the CBN hopes to cut off arbitrage that happens when IMTOs cheaply convert dollars to naira before it gets to beneficiaries.

CBN says it wants users to receive “a market-reflective exchange rate for their inflows,” suggesting a willingness to float the naira.

Considering Nigeria’s large remittance market – $17.5 billion in diaspora remittances in 2019 according to the CBN – Chife believes this good move will level the playing field in the money transfer space.

He says the CBN has “recalibrated competition amongst the international money transfer organizations (IMTO). It’s now ground zero for all IMTO providers.”

Ensuring fairness in the market is probably a secondary goal for the CBN. The apex bank is on a long-term goal of setting up a structure that accounts for every dollar that enters the Nigerian financial system. As with most of the CBN’s projects, this structure will rest on the banking infrastructure.

Banks working with IMTOs will produce what the CBN calls a “central reporting portal for all foreign remittances

” that will

“improve visibility of foreign remittance flows.”

This portal, which will be managed by

the Nigerian Interbank Settlement System (NIBSS), is already being developed.

One can read this from a national security perspective, where the CBN is being vigilant about external funding of terrorism. The most obvious reason for cutting off mobile money operators and centering banks in the remittance process is to take advantage of the BVN which ties every bank account to an identity that can be verified.

But this MoMo exclusion raises one question; how financially inclusive is it to mandate people in rural areas to have bank accounts in order to receive money from their relatives abroad?

We don’t have the CBN’s response to this.

But this reminds us again that, regardless of MPesa’s prowess in Kenya or MFS Africa’s growing influence integrating cross-border transfers across 34 countries, Nigeria wants banks to take centre stage in shaping the future of Africa’s biggest economy’s financial system.

|

|

|

Africa’s wave

Wave, the Toronto-based accounting company, is leaving Africa. Since many businesses have come to depend on it for accounting infrastructure, who will come in to fill the gap it will leave? Daniel interrogates this dilemma and opportunity here.

Cooking for Nigeria

Parent cooks, household eats. That’s how food works in Africa.

Can a tech startup take advantage of this bug to relieve families of the cooking burden while serving healthy meals on time? Here’s what we found about

Choplife

, the food service product from Nigeria-based concierge service startup Eden.

|

|

|

THE CRYSTAL BALL

In the context of technology and innovation, what do you think Africa’s new normal will look like?

Every week, we ask our readers, stakeholders and operators in Africa’s tech ecosystem to share their thoughts on this. You can share yours with me, send an email to victor@bigcabal.com with ‘The Crystal Ball’ in the subject line.

|

|

|

Bit by Bitcoin

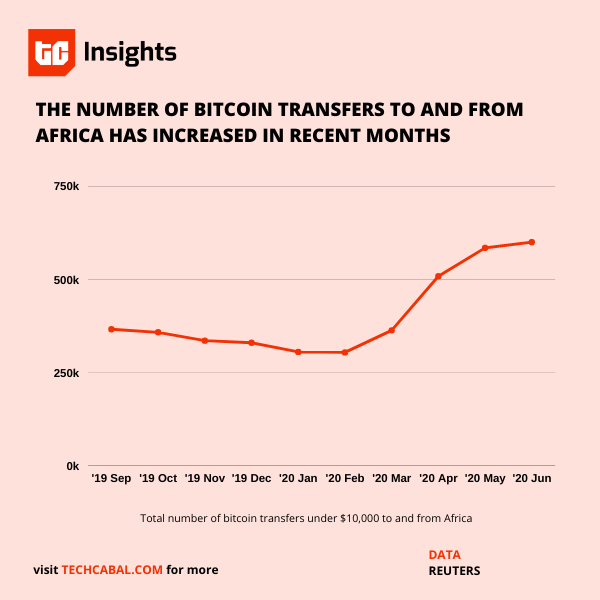

Bitcoin is reinventing a number of things in Africa; one of them is remittances. Usually, to send $200 to anywhere in Africa, you would have to spend an average of 9.4% ($18.8) in transfer cost. With bitcoin, however, you get to save on as much as 90% of the cost.

|

|

|

Since the onset of the pandemic in Africa, bitcoin-based transfer has been gaining much ground, and it’s not just because of cheaper rates. It’s also faster than bank transfers and other transfer channels, requiring mostly a stable internet connection.

Apart from the ease of remittances, bitcoin is a great way to hedge against inflation. Although as of 2019, the average inflation rate in Sub-saharan African countries was 8.38%, countries like Nigeria, Ghana, and Zimbabwe have seen double-digit inflation rates, and unsurprisingly, these countries are among the top countries using bitcoin in Africa.

However, cryptocurrencies may not be having such a smooth sail when it comes to payments. As of 2018, only 2% of digital platforms in African countries allowed their customers pay via crypto, with 80% and 40% opting for card and cash payments respectively.

It is also important to note that in countries like Nigeria, there are no regulations regarding virtual currencies, so the use of cryptocurrency is still enshrouded in some level of wariness; there’s the tendency for people to easily associate crypto with fraud, especially when they aren’t well informed.

Still, the price of bitcoin keeps increasing, and the June 2020 Crypto Research report estimates that it could go over $397,000 by 2030. It’s safe to say that the currency may not be leaving the scene for a while; startups like BuyCoins, BitPesa, and Bitsika are making sure.

|

|

|

This the last episode of

The

Next Wave for 2020, publising will resume January 10th 2021. Thank you for sticking with us, stay safe.

You can subscribe to our TC Daily Newsletter; the most comprehensive roundup of technology news on the continent, and have it delivered to your inbox every weekday at 7 am WAT.

Follow TechCabal on Twitter, Instagram, Facebook, and LinkedIn to stay updated on tech and innovation in Africa.

– Alexander Onukwue, Editor, TechCabal

|

|

|

Sign up for The Next Wave

by TechCabal

|

|

|

|

|

|

|

|

|

|

| | | | | |

|

|

|

|

|

|