|

FEBRUARY 28, 2021

This newsletter is a weekly in-depth analysis of tech and innovation in Africa that will serve as a post-pandemic guide. Subscribe here to get it directly in your inbox every Sunday at 3 pm WAT |

|

|

|

One Direction was a pretty good band, weren’t they? Five hit albums from pubescent teens with diverse upbringings, cobbled together by chance and Cowell. They haven’t officially broken up but their solo careers seem to be flourishing, although 1D die-hards swear it’s not the same.

As with boy bands, getting any group of people or organizations to unite their collective under one roof, for a long time, can be a steep mountain.

You might have a convincing profit motive but the ambition needs an x-factor – something dazzling – to drive sustained interest. If the talents are banks and other financial institutions, what is needed to make this band pop?

Let’s talk about that — about what it takes to unite financial institutions in Africa by APIs and open banking standards. Ready?

|

|

|

Stitches and uniform pipes

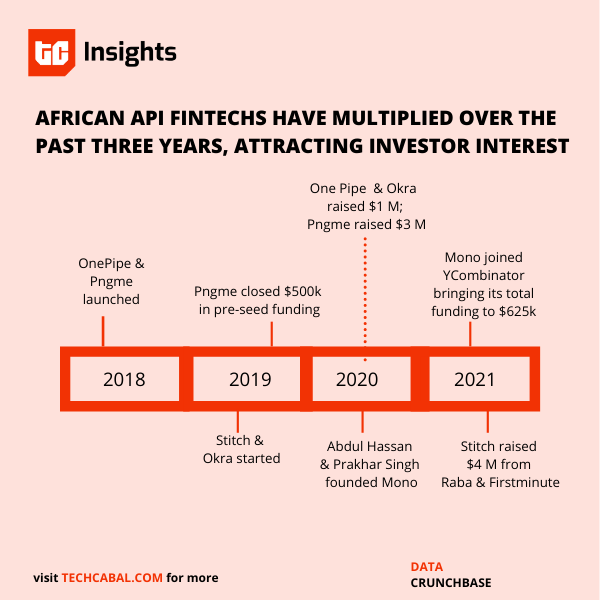

Stitch is a company based in South Africa. As described in TechCrunch last week, they have come out of stealth mode with $4m in seed financing.

The money is for building a kind of product that is on the rise in Africa: fintech APIs.

Mono, OnePipe, Pngme, Okra, Chenosis, and others yet to gain media attention. Call them the new cool of fintech, the “banking-as-a-service” innovators unbundling and re-bundling financial services for Africa.

“The goal is to make building fintech easy and accessible to African developers,” says Kiaan Pillay, Stitch’s co-founder and CEO in an email.

“Since there’s a lot of interest in how we relate to Mono’s ambitions, I’d add that we are definitely pushing in the same direction. We think the Mono guys are great and we’re excited to see what’s next from them.”

So that’s at least two startups building

Plaid for Africa. Are all API fintechs doing the same thing?

|

|

|

The space is new and we could see them converge more with time, but there are basically two buckets of API fintechs right now.

The likes of Stitch and Mono focus on making customer financial data available to individuals and businesses building features that require such data. In the other bucket, startups like OnePipe engage banks directly to pull their APIs under some uniform standard that makes banking services easy to access for especially non-fintech companies.

[ Read: Why Mono is in YCombinator’s W2021 batch ]

“Banks like it when you give them customers,” Ope Adeoye, founder and CEO of OnePipe tells me.

They focus on non-tech companies that cannot afford to be distracted by the tedium of building backend technologies and having weekly meetings/zoom calls with banks to ensure the APIs do what they are configured to do.

Adeoye’s team is guided by the Open Banking Nigeria group.

As with other open banking initiatives around the world, Open Banking Nigeria wants to develop common API standards for the financial services industry and spur more innovation. The Central Bank of Nigeria wants this too and has published guidance documents on why and how banks should embrace the movement.

The model for Nigeria’s open banking aspirations is the UK’s PSD2. It requires banks – whether Barclays, HSBC, Santander or Royal Bank of Scotland – to give non-bank rivals access to customer payment accounts in a secure and standardised form.

No African country has started enforcing API standards in the way the UK currently does. In Nigeria, the CBN is still trying to sell it to banks as a proposal that will work in everyone’s best interest.

For an African rockstar fintech band, these standards will have to exist in enough countries with enough banks stitched together by a uniform set of pipes. Given the nascent state of affairs in most countries, it may be a while before this future emerges.

But the ball is rolling. At least 40 organisations are onboard the Open Banking Nigeria train. They are companies of different types, from different backgrounds, hoping to create the kind of magic that inspires Africa in one direction.

|

|

|

Jumia’s earning report for Q4 2020 throws up a couple of interesting numbers: €41 million in revenues, operational losses of €40 million, and grand merchandise volume of €231.1 million. What to make of these numbers? Muyiwa got you covered.

Ghana received 600,000 doses of the Oxford-AstraZeneca COVID-19 vaccine from COVAX (COVID-19 Vaccines Global Access), the first country in the world to do so. Sorry Nigeria but that giant of Africa claim seems to be drifting more to Ghana these days.

Speaking of Nigeria, can you guess who made this comment about cryptocurrency? “They are black. They are not white. They are not visible and they are not transparent.”

Answer: him.

|

|

|

A working alliance

When you try to define a consumer-facing startup, the quicker example that comes to mind is an investment platform like Cowrywise, a digital lender like Tala, or a payment company like Paystack.

But API fintechs like OnePipe that enable banks to collaborate with fintechs to provide better services to their large customer base are in a way consumer-serving too.

|

|

|

OnePipe is a Nigeria-based API fintech startup working to enable more collaboration between fintech companies and banks. OnePipe believes that fintechs and banks are stronger when collaborating; this is one of their big motivations for providing API services.

API fintech startups are generally a novelty in Africa’s fintech space, but strictly business-facing startups like OnePipe are even more so. Still, their end objective is to provide a seamless experience for customers.

OnePipe refers to itself as a super-aggregator, and what this means is simple – the company combines multiple financial services, in the form of APIs, from banks and fintech into a standardised gateway for service providers to use.

There are some impediments to the work that OnePipe does. Banks are becoming more open to the idea of collaboration, especially as they recognize the importance of technology in providing a better customer experience.

However, this collaboration has not reached its fullest extent. In many African countries, this collaboration is almost non-existent, which may be why the continent’s purely API fintech startups are concentrated in Nigeria.

Another problem is cybersecurity risk. According to ImmunoWeb, 98% of fintech startups face the risk of phishing, web, and mobile application security attacks. More than $3.5 billion was lost to cyber crime attacks globally in 2019. Some observers expect that by 2022, API attacks are going to be a major attack vector.

Still, the consumer-fintech space is becoming a hive of innovative activity, and the entry of startups like OnePipe providing a different yet essential service may increase investor interest and more global limelight.

While OnePipe is focused on Nigerian financial institutions, there’s nothing stopping the company from expanding to other parts of the continent, but the question is if the regulatory and collaborative environment in these countries will be a facilitator or hindrance.

Get

TechCabal’s reports here

and send us your custom research requests via tcinsights@bigcabal.com.

Written by Boluwatife Sanwo

|

|

|

Thank you for taking the time to read today’s edition of The Next Wave. Remember to stay safe when you are out in public places– protect others by wearing your mask and sanitizing your hands.

Looking for the most comprehensive roundup of technology, life and business stories on the continent? Subscribe to our TC Daily Newsletter and have leading news delivered to your inbox every weekday at 7 AM (WAT).

Follow TechCabal on Twitter, Instagram, Facebook, and LinkedIn to stay updated on tech and innovation in Africa.

– Alexander O. Onukwue, Staff Writer, TechCabal

|

|

|

Sign up for The Next Wave

by TechCabal

|

|

|

| |

| |

|

| | | | | |

|  |

|

|

|

|