By Omoaregba Jolomi

Zenith posts ₦1tn profit, doubles dividend

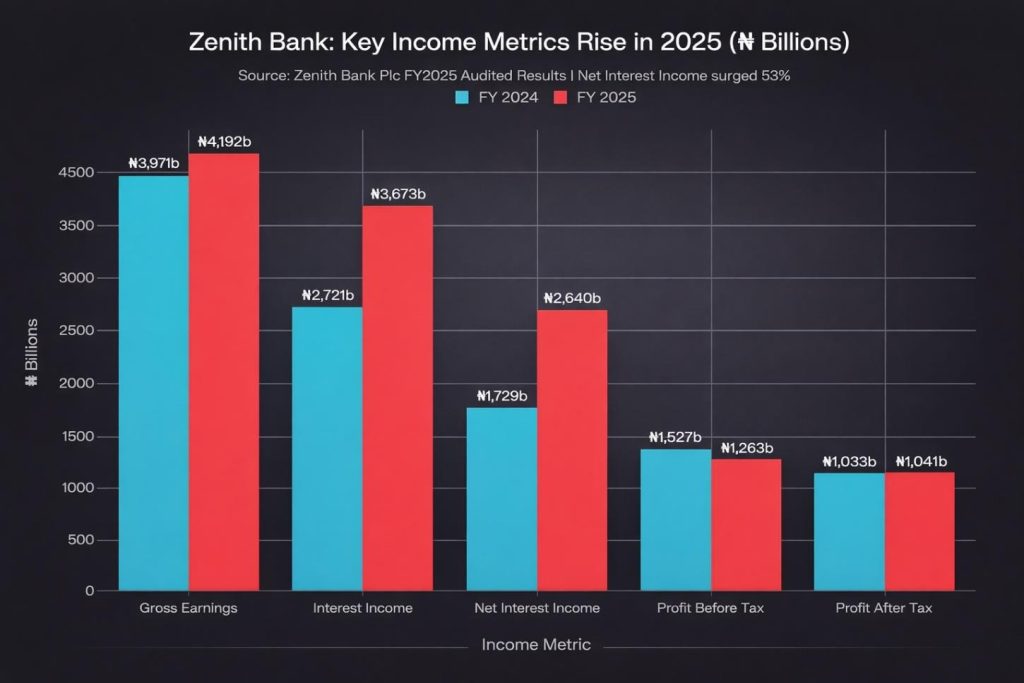

Zenith Bank Plc has released its audited full-year 2025 results, posting gross earnings of ₦4.19 trillion and profit after tax of ₦1.04 trillion, even as the Group executed a deliberate cleanup of regulatory forbearance-linked exposures. The Board has proposed a total dividend of ₦10 per ordinary share, twice the 2024 payout.

With Nigeria’s banking sector under mounting capital and macroeconomic pressure, Zenith’s 2025 scorecard signals disciplined execution, strengthened asset quality, and confidence in long-term growth, as the continent’s financial markets demand more from their anchor institutions.

Resilience, Reset, and Record Returns

On 7 April 2026, Zenith Bank Plc, Nigeria’s financial flagship and one of sub-Saharan Africa’s most closely watched lenders, released its audited Group results for the year ended 31 December 2025.

The headline numbers tell a story of resilience: gross earnings of ₦4.19 trillion, profit after tax of ₦1.04 trillion, and total assets crossing ₦31 trillion. The more telling story lies beneath, in the strategic choices that shaped those outcomes.

For African markets, where the banking sector’s health is a barometer of broader economic stability, Zenith’s results carry weight beyond shareholder returns.

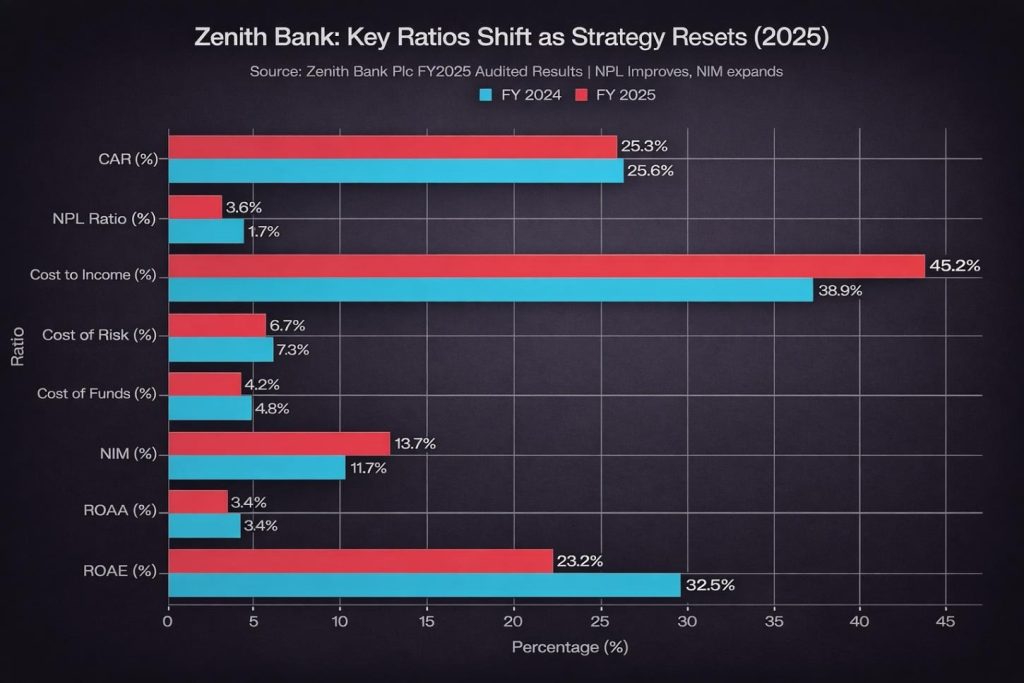

The bank’s deliberate write-off of forbearance-linked facilities reduced earnings per share by 23% to ₦25.32; however, the bank simultaneously improved its asset quality, reducing its Non-Performing Loan (NPL) ratio from 4.7% to 3.8% and signalling a clean slate for 2026.

The results arrive at a pivotal moment for Nigerian and African banking, marked by a high-interest-rate environment, persistent inflation, shifting capital requirements, and growing investor scrutiny on governance quality.

Zenith’s 2025 performance must be read against that landscape: not merely as a financial statement, but as a strategic declaration.

One trillion reasons to pay attention

Here is the number that commands the room:

- ₦4.19 trillion in gross earnings, a 6% increase year-on-year from ₦3.97 trillion in 2024.

- A milestone that cements Zenith’s position among the continent’s most capitalised financial institutions.

- Growth has rarely come without trade-offs. Profits before tax fell 5% to ₦1.26 trillion.

- A direct consequence of the bank’s decision to clean out regulatory forbearance-linked loan exposures that had accumulated across prior cycles.

- This was not a failure of performance; it was, by the bank’s own framing, a strategic reset, one that cost the bank in the short term but significantly strengthened the quality of its balance sheet.

- Non-interest income contracted sharply by 63%, from ₦1.10 trillion to ₦404.9 billion, signalling a shift in revenue composition toward interest-driven earnings in a high-rate environment.

The message from Dame Dr Adaora Umeoji, Group Managing Director/CEO, was unequivocal:

“Our 2025 results are a reflection of the discipline and focus with which we executed our strategy. We successfully strengthened our asset quality, optimised our balance sheet, and invested in the capabilities that will propel our next phase of growth.”

Behind the numbers: What the data really says

Zenith’s 2025 results are a study in how strategic priorities shape financial outcomes.

- Net interest income surged 53% to ₦2.64 trillion.

- Anchored by a 35% rise in interest income to ₦3.67 trillion, powered by high asset yields, expanded interest-earning assets, and disciplined liability pricing.

- Net Interest Margin (NIM) expanded from 11.7% to 13.7%, a 17% improvement that underscores the bank’s ability to maintain healthy spreads between lending and funding costs.

- Cost of funds declined from 4.8% to 4.2%

- Cost of risk improved from 7.3% to 6.7%

- Indicating efficiency in the bank’s risk and liability management.

- Customer deposits grew 11% to N24.33 trillion, fuelled by increases in both corporate and retail deposits, a critical vote of confidence from Zenith’s expanding customer base.

- Shareholders’ funds expanded by 22% to ₦4.92 trillion

- Capital Adequacy Ratio (CAR) stood at 25.3% above the regulatory minimum.

The 13% rise in impairment charges to ₦741.6 billion reflects the bank’s deliberate and prudent provisioning posture; notably, the coverage ratio remains robust at 172.6%, providing a substantial buffer against future credit stress.

Source: Zenith Bank Plc — Audited Group Results, FY2025

What this means for investors, markets, and Africa

For investors and analysts tracking Zenith Bank, the most attention-grabbing signal in the 2025 results is the dividend. The Board has proposed a final dividend of ₦8.75 per ordinary share, bringing the full-year total, including the ₦1.25 interim dividend already paid, to ₦10.00 per share. This is a 100% increase over the ₦5.00 total dividend paid for 2024, signalling the board’s conviction in the bank’s earnings resilience and forward trajectory.

For Nigeria’s capital markets and African equities more broadly, a dividend of this scale from one of the continent’s most-watched lenders is a significant signal.

It demonstrates that African banks with strong governance frameworks and disciplined capital management can consistently reward shareholders even through challenging macroeconomic cycles.

The bank’s growing international footprint, spanning Ghana, Sierra Leone, Gambia, Côte d’Ivoire, the UK (with branches in London and Manchester), Dubai, Paris, and a representative office in Beijing, reinforces its position as a pan-African institution with global ambitions.

With over 800,000 shareholders and over 400 branches across Nigeria, Zenith’s physical and institutional reach into communities across the continent represents a tangible infrastructure for financial inclusion at scale, one that carries real sustainability and development significance.

What must happen next

The 2025 results present specific signals for policymakers, regulators, investors, and bank leadership alike. Zenith’s successful exit from forbearance-linked exposures offers a model for how Nigerian Tier-1 lenders can navigate the recently concluded Central Bank of Nigeria’s (CBN) recapitalisation demands without sacrificing profitability, but execution discipline will be critical.

For the CBN and sector regulators, these results reinforce the case for consistent, predictable capital policy frameworks: as lenders absorb higher capital requirements, their ability to maintain lending quality, particularly for SMEs and underserved communities, will depend on clear regulatory signalling and coordinated supervisory engagement.

For ESG-focused and institutional investors globally, Zenith’s improving asset quality metrics and robust capital position present a compelling case. The 25.3% CAR and 71.1% group liquidity ratio, both well above regulatory minimums, provide the risk buffers that sustainability-aligned, long-term investors increasingly require.

Dame Umeoji’s reference to Zenith’s “unicorn workforce” and commitment to long-term stakeholder value, including customers, shareholders, communities, and regulators, reflects a governance culture that goes beyond compliance into purposeful sustainability intent.

Source: Zenith Bank Plc — Audited Group Results, FY2025[1]

Rebuilding for the long game

Zenith Bank enters 2026 having absorbed the costs of a deliberate balance sheet reset and emerged with stronger capital, improved asset quality, and a doubled dividend commitment.

Growth priorities now centre on expanding core deposits, deepening digital financial services, and accelerating cross-border lending across its pan-African network.

The broader imperative belongs to Nigeria’s banking sector and Africa’s capital markets ecosystem: to build on institutions that demonstrate ESG discipline, governance transparency, and consistent shareholder returns, to anchor Africa’s financial deepening, mobilising institutional capital, and powering the inclusive growth the continent urgently needs.