After a dazzling January debut that saw Africa-focused tech startups raise over $430 million from roughly 60 announced deals, fundraising in February was similarly feverish. The shortest month of the year witnessed approximately 60 announced tech deals across the continent comprising ~$600 million in disclosed funding, according to Afridigest’s weekly tracker.

This story was contributed to TechCabal by Emeka Ajene.

So far, Africa-focused startups are on pace to raise ~$6 billion in disclosed funding and over $7 billion in total funding this year—assuming disclosed funding stays at ~85% of total funding. (In 2021, according to Partech Partners, fully disclosed deals represented 85% of total funding.)

In terms of the number of deals, Nigeria led the way with 18—~31% of the total number of deals announced in February across the continent. But these Nigerian deals represented ~57% of the ~$600 million raised in the month, thanks largely to Flutterwave’s $250 million Series D (the continent’s second mega-round of 2022); it alone accounted for ~42% of February’s total disclosed funding.

Regional spotlight

February saw a return to fundraising dominance by the “Big Four” countries (i.e., Nigeria, South Africa, Kenya, and Egypt). Unlike January which saw the four countries account for just about half of disclosed funding, the Big Four accounted for a whopping 95% of disclosed funding raised in February.

Sector breakout

Sector-wise, fintech unsurprisingly led the way again, attracting 52% of disclosed funding in the month (up significantly from January’s 29%), followed by software’s 16%, thanks largely to chat commerce software provider Clickatell’s $91M Series C.

The top 5 sectors that attracted funding in February were fintech, software, e-commerce, healthtech, and mobility. And rounding out the top 10 were logistics, connectivity, crypto, proptech, and insurtech.

Trends and developments

While fintech, overall, continues to be ascendant, developments in February emphasised one broad theme in the sector:

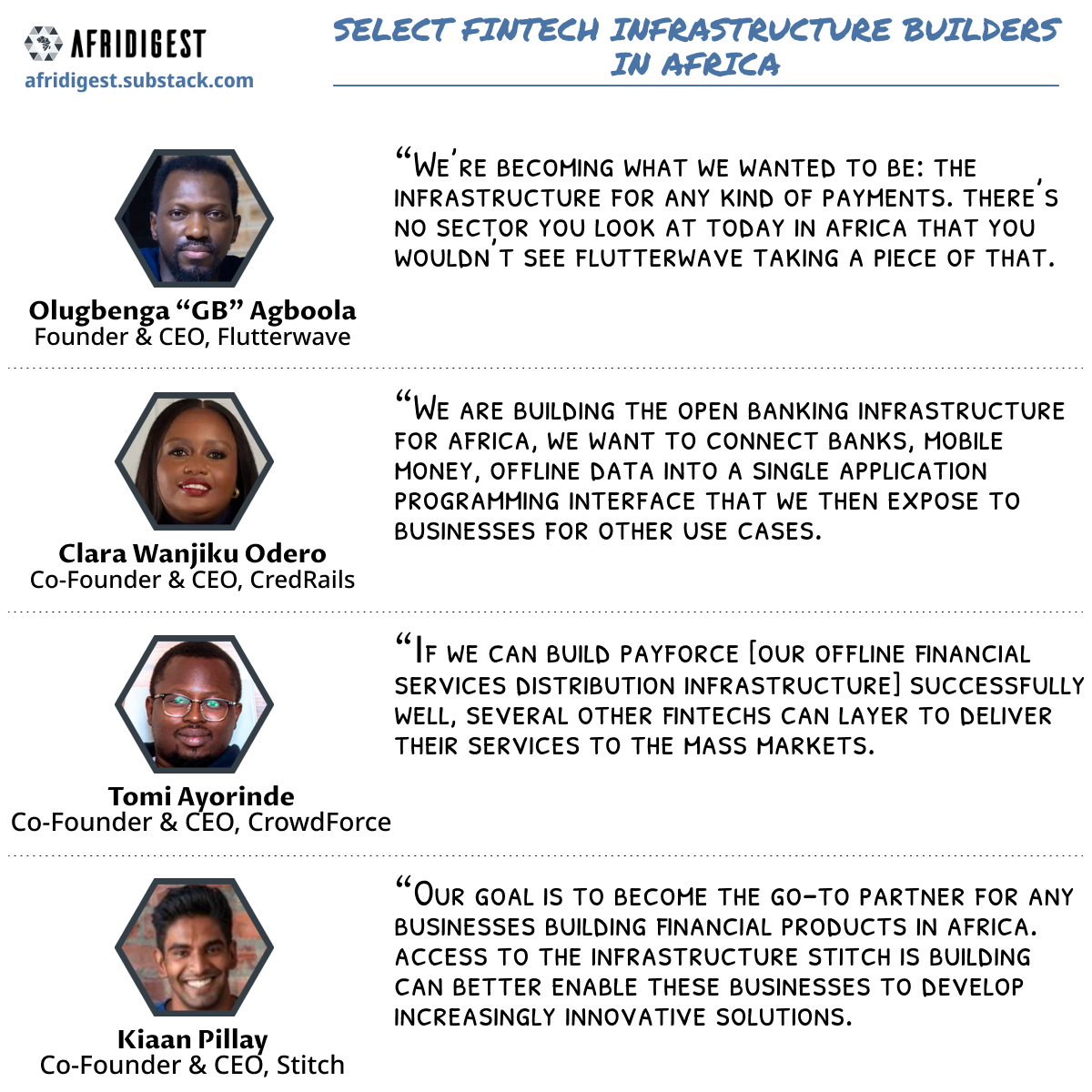

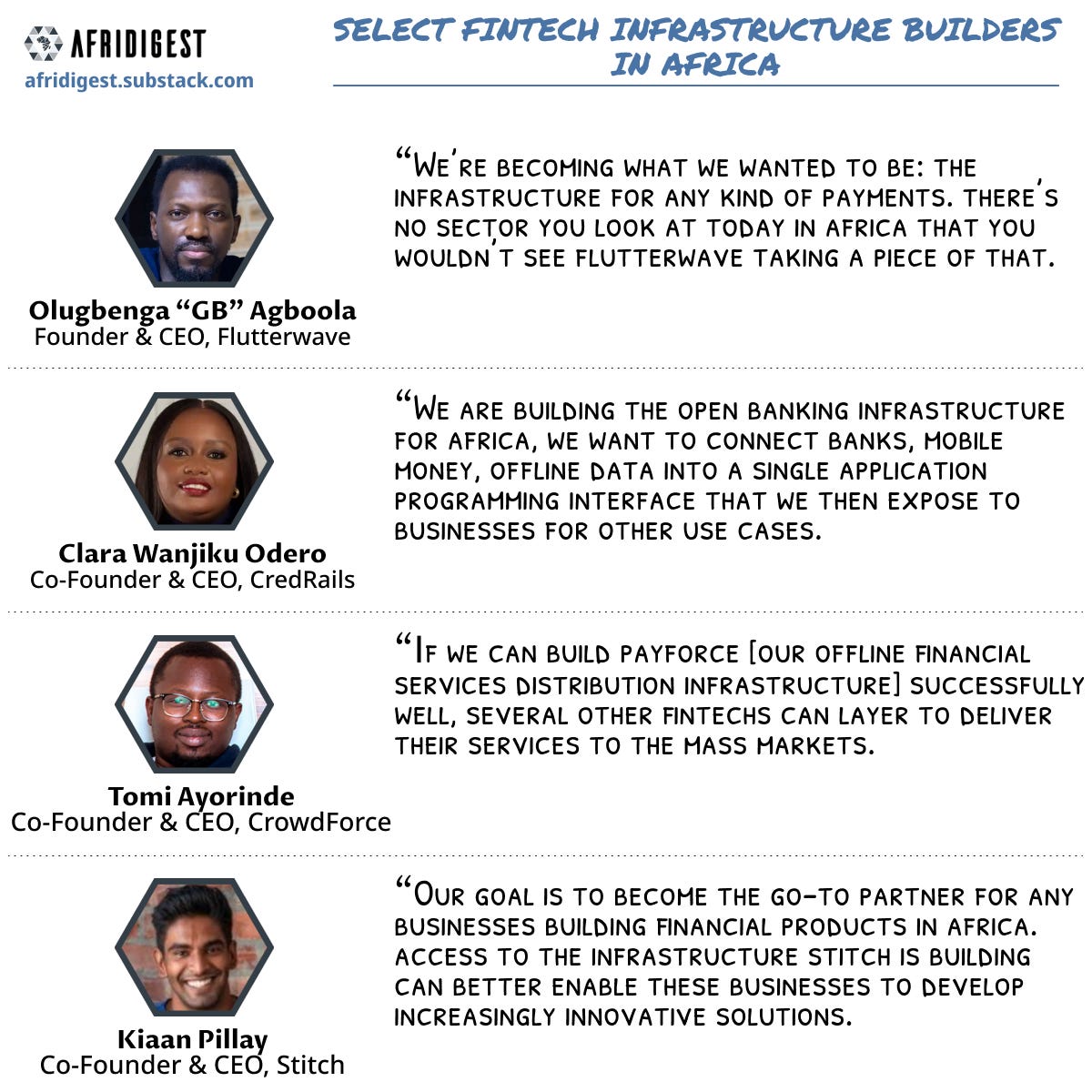

- There’s still a massive opportunity in financial infrastructure. In 2020, I wrote that “in an ecosystem, the pre-potent layer is infrastructure [and] there generally remain robust opportunities to create ventures that introduce basic or alternative infrastructure that can underpin the entire ecosystem”. This still rings true today, and February brought with it a strong reminder of the opportunity in building fintech infrastructure across the continent.

Nigeria’s Flutterwave is now the most valuable startup in Africa, thanks largely to its initial focus on and success with building prized payments infrastructure. Other payments infrastructure providers like Nigeria’s TeamApt and Kenya’s Ubawa raised rounds in February; Egypt’s MoneyHash raised a pre-seed to build payments orchestration infrastructure that integrates and sits on top of payment providers like Flutterwave; South Africa’s Stitch and Kenya’s CredRails raised rounds to build open finance API infrastructure; and CrowdForce raised a round to grow its last-mile financial services distribution infrastructure.

While it’s appropriate to lead with fintech, given its dominance in February, perhaps it’s a well-worn theme for regular observers of ecosystem trends. That said, February also saw interesting, fresh developments relative to strategic acquisitions and investments across the continent:

- M&A in African tech is heating up. At the start of the year, I put forth that an increase in strategic bolt-on and tuck-in acquisitions is among 5 major trends to expect across Africa’s startup ecosystem in 2022. And thanks to a very acquisitive February, this now seems prescient; at least eight acquisitions were announced in February alone. (This trend also continues into March with a number of additional acquisitions already announced, just halfway through the month.)

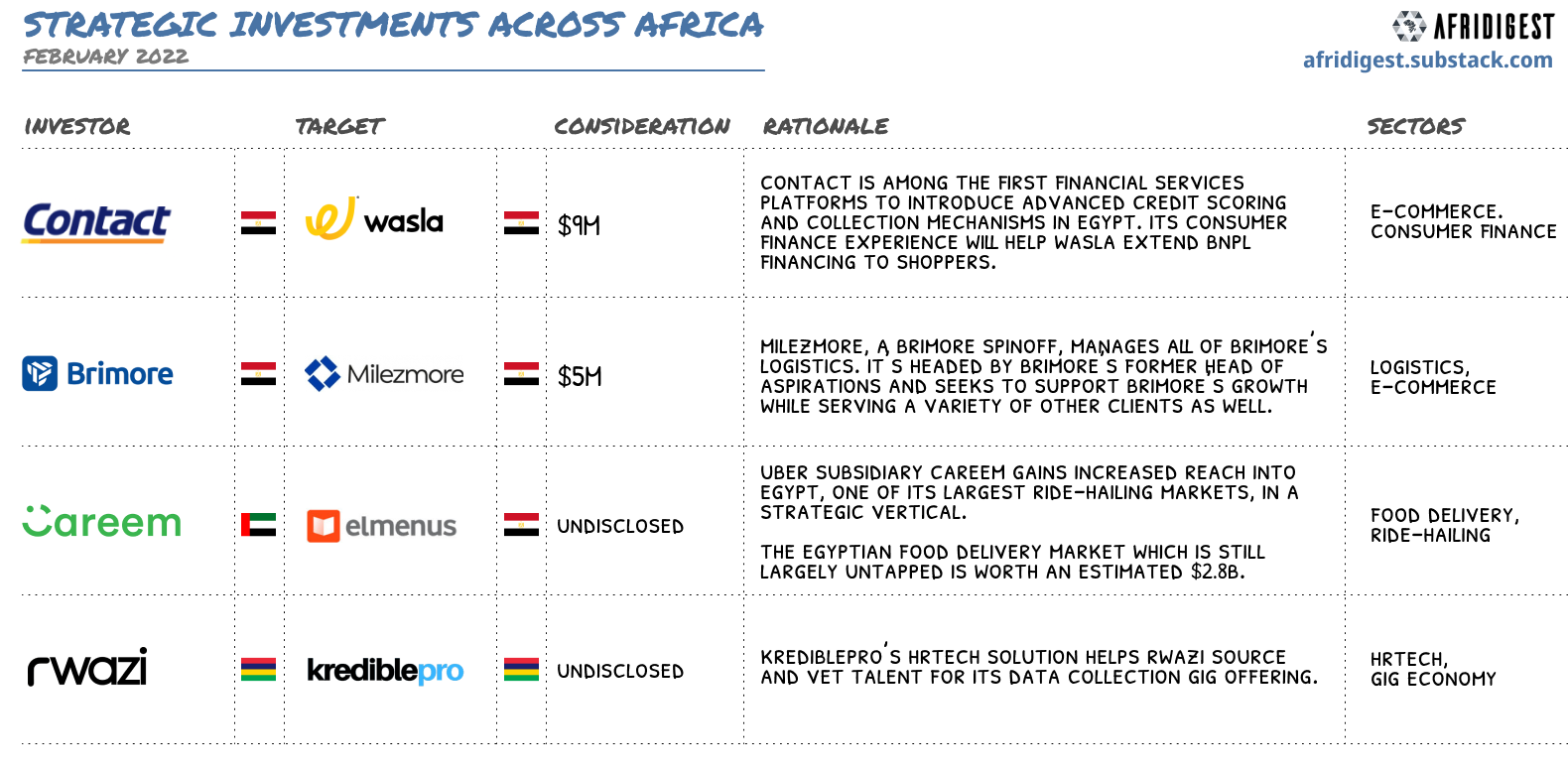

- Strategic minority investments are on the rise. Coupled with the uptick in outright and majority acquisitions, February also saw an increasing number of companies take strategic minority positions in various startups (in Egypt mostly, but elsewhere too).

Egyptian non-bank consumer finance provider Contact Financial invested $9 million in Egyptian shopping browser Wasla to help it deploy BNPL offerings, Egypt’s Brimore invested $5 million in its logistics spinoff Milezmore, the UAE’s super app (& Uber subsidiary) Careem took a stake in Egyptian food delivery platform Elmenus to gain more exposure to a strategic vertical in a high-potential market, and Mauritian survey-focused gig economy platform Rwazi invested in Mauritian HR tech platform KrediblePro which helps it source talent.

Switching gears and looking back to the article, “Key trends & themes to look for across Africa in 2022“, I offered there that “2022 could see the rise of crypto/blockchain/web3 projects deployed across the African continent as it increasingly becomes the global centre of utility-driven ‘web3’.” And February brought good tidings for web3 in Africa:

- The race to onboard African users to web3 is on. In early February, Nigeria’s Nestcoin, a builder, operator, and investor in web3 applications (in the mold of the US’s Digital Currency Group) raised a sizeable pre-seed backed by a mix of globally-recognised web3 VC firms and local investors in order to accelerate crypto and web3 adoption in Africa.

And later on in the month, the Democratic Republic of Congo’s Jambo Technology raised a seed round of its own backed by Tiger Global, Coinbase, & other names that the global crypto community would easily recognise in order to build the “web3 onboarding portal of Africa”.

Also in the month, Canza Finance raised a seed round for its DeFi neobank play that acts as a crypto on/off-ramp, enabling a variety of services including staking, P2P transfers, and cross-border settlements. (And, notably, this trend has continued at least through the first few days of March, with announced fundraises from crypto exchange VALR and airtime-based crypto onramp Fonbnk.)

While the crypto or “web3” sector heats up, other sectors worth watching include healthtech, foodtech, “vehicle tech”, and logistics.

- Healthtech is warming up. In my piece on the Africa tech trends to watch for this year, the fourth prediction began: “2022 could see significant developments in non-fintech sectors like healthtech.” So far so good in February as the month saw the $40 million Series B of Nigerian health insurance & telemedicine platform Reliance Health, Kenyan digital health record and healthcare management platform Afya Rekod’s seed round, Nigerian health (and job loss) insurance platform Casava’s pre-seed, and Nigerian pharmacy-focused procurement & management platform Remedial Health’s pre-seed and acceptance into Y Combinator’s W22 batch.

- Foodtech is experiencing a renaissance of sorts. January saw Orda, a Nigerian restaurant management platform, raise a pre-seed round to build digital infrastructure for restaurants. And the momentum in the sector carried over into February with fundraises from Egyptian B2B restaurant supply chain platform OneOrder, Egyptian B2B cold-chain logistics and agri-goods storage platform Freshsource, Nigerian food delivery platform HeyFood (also a participant in Y Combinator’s W22 batch), Kenyan tech-enabled B2B food distribution andlogistics platform Kwanza Tukule, and Egyptian food delivery platform Elmenus’ strategic investment from Careem.

It’s still the early stages of foodtech in Africa but entrepreneurs and investors seem to increasingly see a sizeable opportunity here. Everybody’s gotta eat after all. - Vehicle access and maintenance are attracting increased attention. February saw fundraises from: Nigerian mobility platform MAX, which is increasingly focused on providing access to low emission vehicles via collateral-free subscription packages; Kenyan electric mobility startup Basigo, which provides locally assembled mass transit electric buses; Nigerian vehicle management platform Mecho Autotech, which offers vehicle insurance & maintenance subscription packages; South African digital vehicle identity platform CarScan; and Tunisian automotive claims digitization platform Avidea.

Mobility is an everyday need, and in the African context, the sector faces a number of challenges, from insufficient public transport infrastructure to low vehicle affordability to the ubiquity of older, barely roadworthy vehicles “dumped” across African markets to a lack of trust and transparency in various processes (from purchase to insurance claims), and more. It’s with this lens that one should view the traction and variety of approaches within the continent’s “vehicle tech” sector. - There’s still lots of love for logistics. In addition to fintech, tech-enabled logistics has been among the sectors receiving significant investor attention in recent years—trucking logistics in particular.

From the $30 million Series A of Nigeria’s Kobo360, the $23 million Series A of Egypt and MENA-focused Trukker, and the purported $20-$30 million Series A of Kenya’s Lori Systems, all in 2019, to the $20 million Series B of Kenya’s Sendy in 2020 to the $42 million Series A of Egypt’s Trella in 2021, there’s been a lot that investors have loved when it comes to logistics.

This love was kept alive in February with fundraises from Kenyan trucking logistics platform Amitruck; Egyptian instant delivery and quick-commerce specialist logistics platform Yalla Fel Sekka; Egyptian cloud fulfillment, last-mile delivery, and customisable operations platform Milezmore; and Moroccan logistics management platform Freterium.

Final word

All in all, it was a fantastic February across Africa’s startup ecosystem, which bodes well for 2022 and beyond. And early returns in March, including fundraises from M-KOPA and VALR, suggest that the pace won’t slow anytime soon.

While an increasingly common refrain is that there’s too much focus across the ecosystem on fundraising news and figures, one thing it allows for is connecting dots, synthesising and contextualising developments, and sense-making as done here. What matters isn’t (just) the numbers, but the narratives behind them.

Emeka Ajene has nearly a decade of diverse experience across the African startup ecosystem as a founder, operator, angel investor, strategic advisor, mentor, speaker, and writer. His background includes leading teams at Konga and Uber in Nigeria and co-founding francophone Africa-focused super app Gozem. He is also a senior advisor at thought leadership agency intellence and writes regularly at Afridigest where a version of this post first appeared. Follow him on Twitter @eajene.

{kind=link}

{kind=link}

{kind=link}