This essay is a contribution from Chernay Johnson (director of research, DFS Lab).

Africa’s $1.4 trillion retail market is a massive opportunity. The largest raw economic opportunity in serving consumers are those earning $4–$8 per day; back in 2020 we called this the fortune at the middle of the pyramid. But we’re learning that it is extremely challenging for digital platforms to profitably serve this segment. Once you factor in acquisition and distribution costs, these models break and are forced back to serving those living on $10/day or more, which are only 5% of the continent’s population. Unless you’re able to fundamentally innovate around your cost structure, B2C marketplace models selling food and necessities potentially break under this logic. At DFS Lab, we think B2B models that aggregate consumers through small businesses probably have a stronger chance.

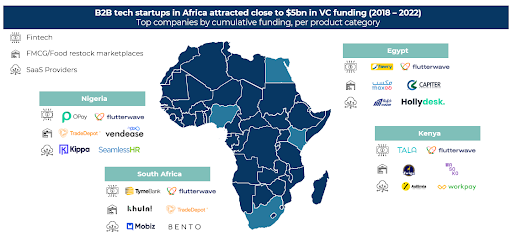

New retail models are seeking to move the small retailer (duka, spaza, kiosk, and mom-and-pop shop), from a world of opaque supply scarcity to one of predictable supply abundance. A tech-enabled solution stack has emerged across the retail value chain, spanning solutions which are addressing inefficient sourcing and distribution systems, payments, inventory management, discovery functions, and a whole lot more. These startup players—spanning across fintech, SaaS, and restocking for FMCG/Food retailers “B2B restock”—have attracted close to $5 billion in funding flows since 2018.

Source: DFS Lab research based on funding data retrieved from Briter Intelligence, The Big Deal database, and media releases. Note: Some of these companies are headquartered in the United States and serve multiple African markets; our country classification refers to the major market of operations

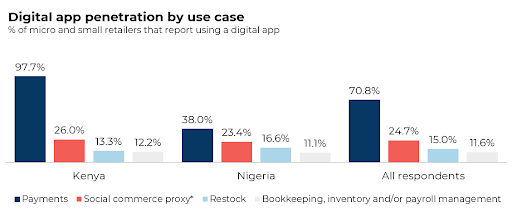

One model we’ve been watching closely are B2B restock platforms in the FMCG/food sectors. At scale, they are able to aggregate suppliers and retail stores while compressing the supply chain between them for a potential cost savings of 33% to 66%. Data from our DFS Lab Retail Digitisation Tracker suggests that 1 in 5 micro and small retailers across Nigeria and Kenya are already using these marketplaces to restock on inventory (see figure below).

Source: DFS Lab. (2022). Retail Digitisation Tracker Survey. N > 1,800 across all retail outlet types, which include: wholesalers, restaurants, resellers, pharmacies, modern supermarkets, general grocers, open market traders, as well as mom-and-pop shops (better known as dukas and kiosks). * These are surveyed respondents who report using social media apps (e.g., WhatsApp, Facebook and/or Instagram) to market goods and services to customers.

However, we’ve seen the space become ever more crowded, with key players, such as Wasoko, TradeDepot and MaxAB turning on a firehose of FMCG products aimed at small retail across Africa. This has introduced a problem into the mix: their hoses are all connected to the same hydrant, and there is little differentiation in the current product mix. The bulk of these products are commodities supplied by one of a few multi-national and local corporations (e.g., Unilever and Dangote) who have little incentive to share a bigger cut of the margin with new platforms.

We estimate gross margins for the restock model have settled at 2–5% in the FMCG sector, with the biggest startups approaching $250 million to $500 million and growing in annualised GMV. Those that distribute food to restaurants specifically are generally at an earlier stage and so are so far reaching low double-digit margins, given perishable food is a much harder problem to solve for.

Engineering tells us nothing works in isolation, but which gear you push the hardest, and when, matters for the rest of the flywheel. In line with our thesis on the B-side of African Tech, startups are now gearing up to go beyond sourcing and distribution in the retail sector, and this is where the real experimentation with unit economics is happening.

There is a lot of experimentation happening with layers such as bookkeeping and inventory management tools, which are typically offered under some type of freemium pricing structure. Alongside being a value-added service to retailers, for tackling stock out and overstocking issues, they are a useful strategy for customer acquisition. These tools also add a layer of stickiness which, in time, could add to the life-time value of the customer (there’s potential for these layers to be monetised at scale). Kippa, a startup serving retailers in Nigeria, bypassed restock and started out with a bookkeeping app. Now, the startup is pivoting to agency banking: the company acquired a Super-Agent banking licence in Nigeria. Since its launch in mid-2021, Kippa claims to have served over 500,000 merchants with an annualised transaction value of over $3 billion recorded on its platform, though it’s yet to be seen if and how they evolve beyond fintech.

Platform-enabled wallets are another trend; there’s an assumption out there that if you can cut out the card processors, some 2% in margin is ripe for the picking. However, regulations around card acquirers and payment providers in Africa are known to be tough, ever-changing and fragmented across borders. So, in the near term, many startups will still need to use intermediaries such as licensed financial services’ partners to get transactions cleared and settled (at best, we think they could achieve an additional 0.5%–1% after processing fees, depending on volume).

Embedded credit is almost always on the feature set pathway. Lines of credit could include invoice factoring, traditional working capital loans, or even BNPL (with returns somewhere between 3%–6% on gross interest). Samora Kariuki offered an opinion on the profitability of the embedded finance route in Frontier Fintech: “Basically, a leviathan B2B digital vendor needs to emerge that is of sizable scale such that most FMCG are distributing exclusively through them.”

At the marketing and discovery layer, platforms are utilising vast lakes of data to catalyse features such as product recommendations, sales conversions, basket upsells and repeat purchasing. Not only do marketplaces have the potential to uplift their own sales, they are starting to offer these services to their upstream suppliers and producers. TradeDepot, for instance, offers a Trade Insights platform which allows suppliers to track their performance against peers, run targeted promotions and messaging campaigns, as well as optimise distribution based on real-time demand analytics broken down by product, channel and/or location. The pricing structures of these types of products are still being tested, and from what we know, they currently contribute small but potentially important additions to the revenue pool of existing players. As Africa’s retail value chain continues to move from a world of scarce distribution to abundance, discovery functions will be of increasing importance for B2B marketplaces to scale to maturity.

What all these experimental layers have in common, are data monetisation plays built around the fundamental network effects of marketplace models. Feedback loops across the stack layers will most certainly drive down the CAC and even layers which currently have near zero margin, i.e., freemium, could become highly monetisable.

That said, the hard limits of retail digitalisation will remain hard to break. As major B2B e-commerce platforms move to preserve runway, in the wake of a global market downturn, we’ve seen several rounds of layoffs, including by major players such as MarketForce, Capiter and Alerzo.

Our view is that no one B2B market player is near maturity in Africa’s retail sector. At full scale, the dynamics around unit economics could (and will) look a lot different as strong network effects multiply the profitability of a few market leaders. This is only starting to happen in the race to digitise retail in Africa, and we’ll continue to patiently keep an eye on emerging trends. Some careful combination of experimentation will no doubt bring progress, on a continent for which there is no tried and tested formula. But we think this will take more time than the pitch decks predict.

Beyond investing in founders who are building the future of digital commerce in Africa, DFS Lab supports the ecosystem through our deep research and industry intelligence. Our goal is to continue to collect primary data across multiple African markets and track digitization trends over time. For more information and to partner with us, get in touch with Chernay Johnson.

We’d love to hear from you

Psst! Down here!

Thanks for reading The Next Wave. Subscribe here for free to get fresh perspectives on the progress of digital innovation in Africa every Sunday.

Please share today’s edition with your network on WhatsApp, Telegram and other platforms, and feel free to send a reply to let us know if you enjoyed this essay

Subscribe to our TC Daily newsletter to receive all the technology and business stories you need each weekday at 7 AM (WAT).

Follow TechCabal on Twitter, Instagram, Facebook, and LinkedIn to stay engaged in our real-time conversations on tech and innovation in Africa.

Abraham Augustine,

Senior Writer, TechCabal.

|

|

|

|

|

18, Nnobi Street, Surulere, Lagos, Nigeria |

View in Map |

| You received this email because you signed up on our website or made purchase from us.If you know longer wish to recieve these emails, please unsubscribe |