Paystack, the Nigerian fintech giant, is launching a direct debit product in partnership with NIBSS, which operates Nigeria’s instant payments infrastructure.

Paystack, the Stripe-owned fintech, is launching a direct debit product that will allow Nigerian businesses to charge customers’ bank accounts directly. Direct debits are useful for recurring payment activities, like a DStv, Tizeti, Netflix, or Spotify subscription, allowing these services, with the user’s consent, to debit the consumer’s bank account without requiring debit card information. This approach helps merchants and other services reduce costs related to card transactions and reduce other frictions related to card payments. Direct debits are also useful for lending services, enabling them to automate loan repayments on their due dates with the approval of customers instead of waiting for a manual bank transfer process.

Direct debits have existed in the Nigerian financial services industry for years, but they require an in-person visit to the bank to manage the process. Several companies have long talked about how a digital alternative could help boost recurrent revenue while ensuring that customers don’t suffer service disruption if they miss their subscription payment due to forgetfulness or card network challenges.

Paystack says it worked with the Nigeria Inter-Bank Settlement Scheme (NIBSS)—which operates the country’s instant payments infrastructure—to connect nearly two dozen banks for direct debits. The partnership allowed Paystack to leapfrog the hurdles and time it takes to manually integrate with each bank and will help reduce the processing time to set up each consumer to mere seconds.

“Everything from the acquisition of a switching license to infrastructure improvements to deep product investments in bank transfers all laid the groundwork for us to finally be able to offer a robust direct debit experience,” Paystack told TechCabal.

Paystack’s direct debit feature ties closely to the company’s recent push to develop fintech products on top of consumers’ bank accounts. This approach cuts out debit cards, which have long played the role of middleman between merchants and consumer payments. Outside of cash, debit cards, provided by card networks in partnership with banks, allow merchants to universally collect payments from customers and complete the final settlement on the backend. However, card transactions, with its pool of fintech participants, carry additional costs to merchants and users, causing the final transaction amount to rise slightly above the original price of the service.

In recent months, Paystack has been looking to go direct to help businesses and consumers complete payments solely from a bank account or an equivalent mobile money wallet. And this move beyond web-only collection is paying off, the fintech explained.

In 2017, Paystack introduced “pay with bank transfer,” which allows customers to complete transactions without using a debit card. This method of payment has ballooned, rising from under 13% of the company’s total transaction activity in 2021 to 34% since the start of 2023. This growth in the bank transfer payment channel is driving Paystack’s broader focus on non-card alternatives.

The company rolled out a new virtual account partnership with Titan Trust Bank to reduce the latency of bank transfers. In October, it followed this up with the launch of virtual POS terminals, a new web product that allows merchants to accept payments with bank transfers for multi-person businesses. The direct debit feature, with a focus on bank accounts, ties closely with Paystack’s recent strategy.

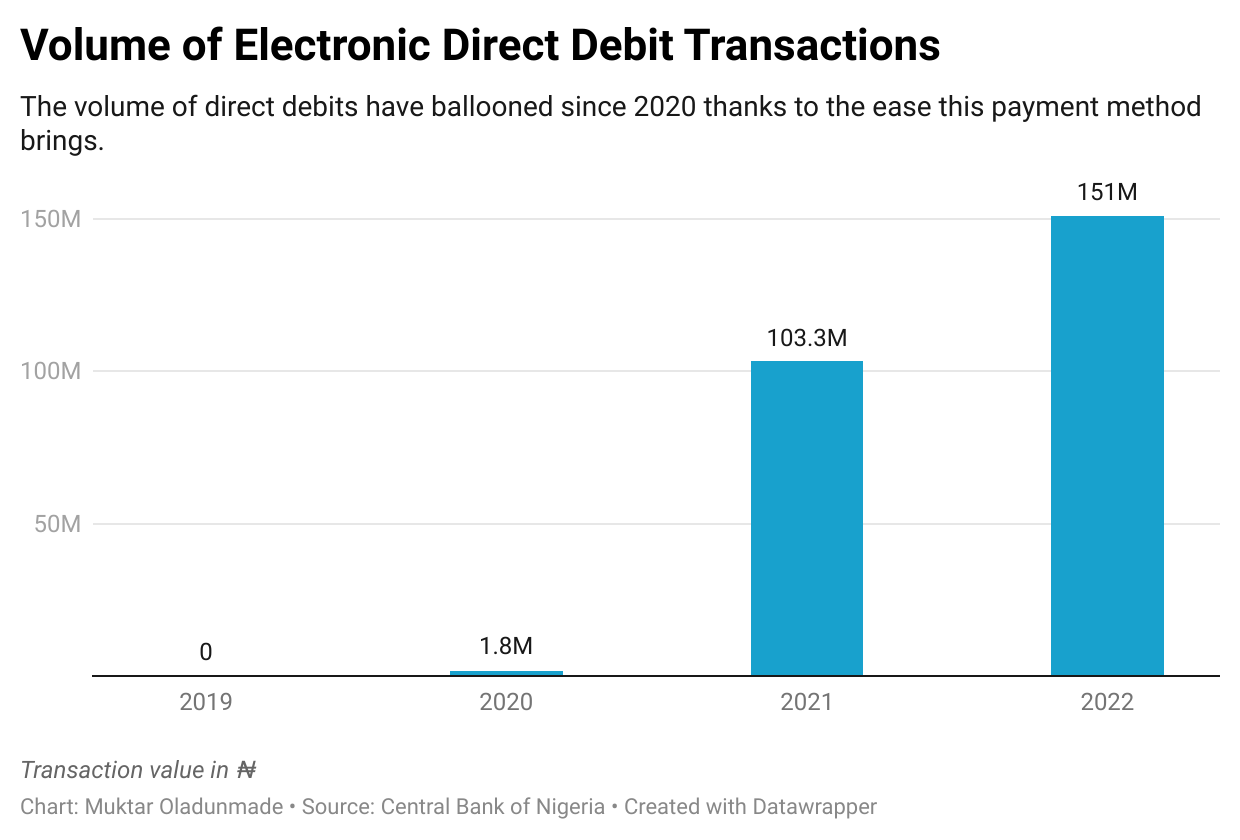

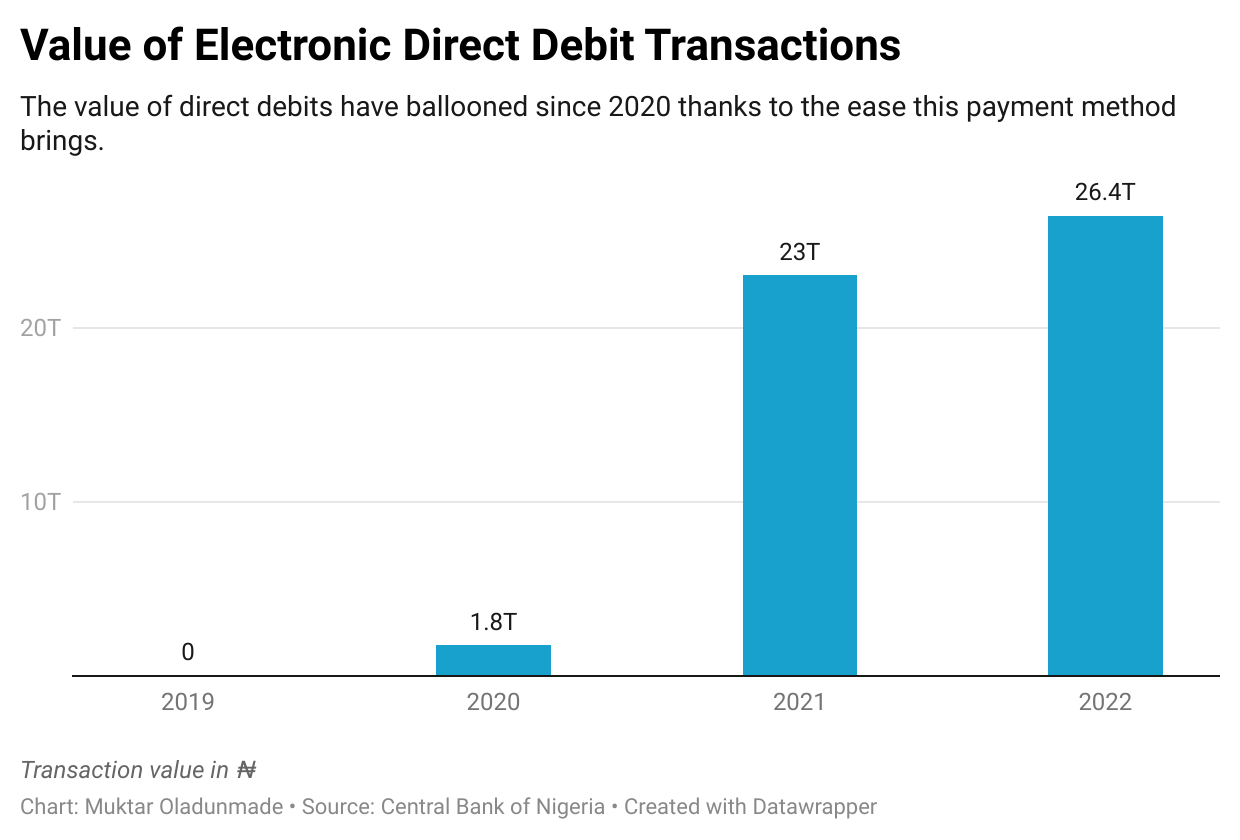

Meanwhile, direct debit services have been gaining adoption in Nigeria in the last few years. The total value of direct debits has grown to N26.4 trillion, an exponential growth compared to N1.8 trillion in 2020, one year after the Central Bank of Nigeria (CBN) started tracking data on these transactions.

Paystack, which was acquired by Stripe in 2020 for $200 million, says Nigerian users can link their bank accounts to a merchant’s business upon request. The fintech will complete a one-time transaction to authenticate the bank account and secure consent from customers. After the bank transfer is confirmed, a merchant can begin to process payments, either recurring or one-time.

Users will also have access to an online portal through which they can manage all their direct debit mandates with Paystack merchants. This is only the second time that Paystack has built an end user-facing product after a portal where customers could complain about failed transactions was released.