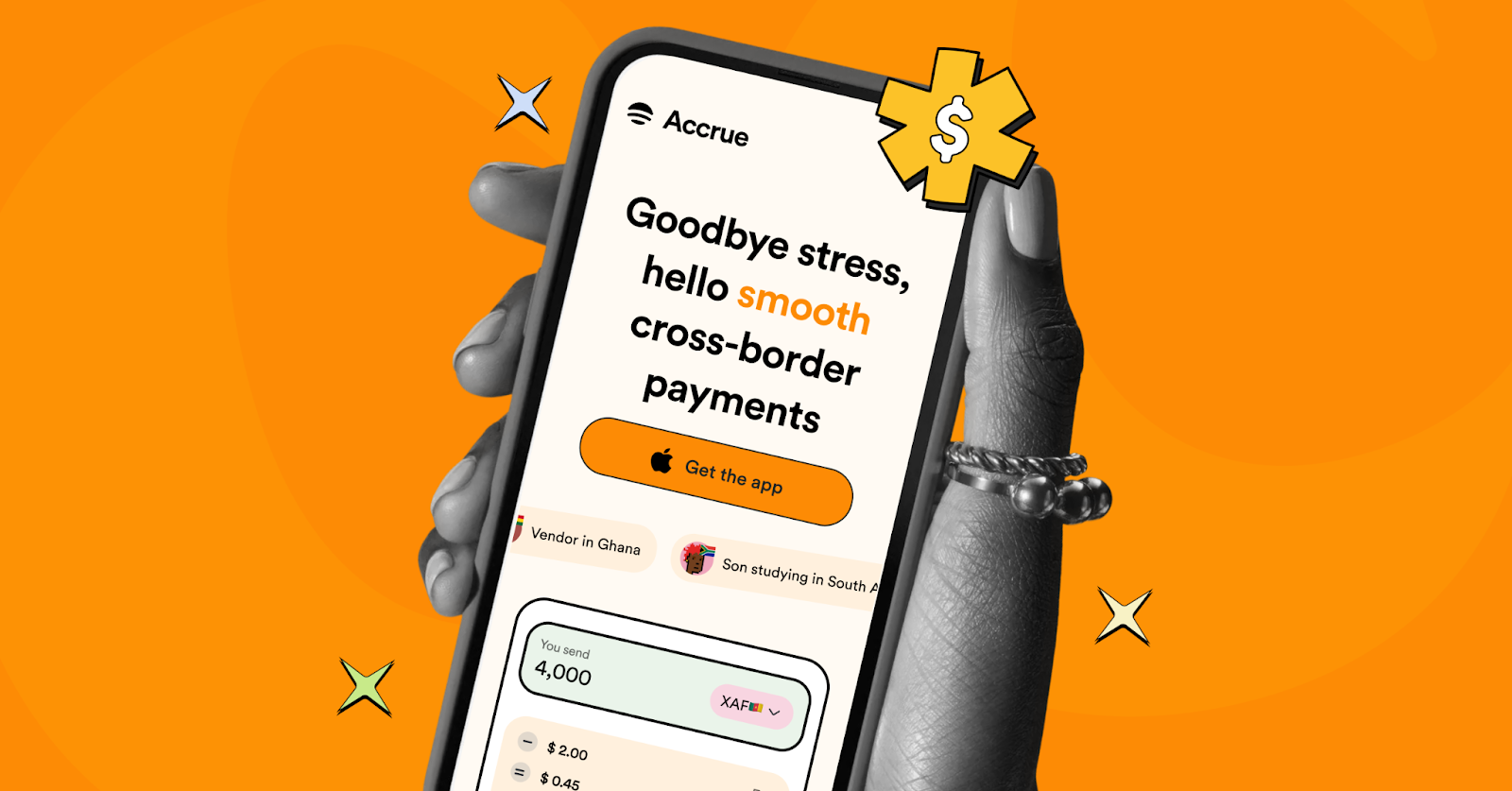

Cross-border payments in Africa have long been broken. More people are choosing Accrue because the fees are low and the transaction is fast; recipients get their funds in less than five minutes.

Different people. Different borders. One shared frustration.

Saliu runs a fabric business in Ibadan. He sources kente materials from suppliers in Ghana, high-quality textiles that his customers love. By all measures, the business is thriving, but every time Saliu needs to pay his suppliers across the border, things fall apart. He has tried multiple payment apps, but the result is almost always the same: delayed transactions, fees that quietly eat into his margins, and the constant anxiety of not knowing whether his money will arrive or when it will. Each failed payment risks a relationship he has spent years building. Each delay means stock he cannot order, and customers he cannot serve.

Jolie made the journey from Cameroon to Nigeria in search of better opportunities. She found them. She works as a nanny for a wealthy family in Ikoyi, one of Lagos’ wealthy neighbouroods, her employers pay her well, in dollars, no less, but Jolie carries a persistent worry: getting money back home to her family in Cameroon is far harder than earning it. Every attempt to send money across that border comes with friction, delays, and uncertainty.

Then there is Johnson. He recently relocated from the Benin Republic to Nigeria, where he drives haulage trucks for a living. He promised his family he would send money every month, but keeping that promise has been hard. Formal channels are slow and unreliable, and in moments of desperation, he has resorted to handing cash to people travelling back to the Benin Republic, a solution that is risky, informal, and entirely out of his control. Once the money leaves his hands, he can only hope.

Three people. Three different lives, three different borders, three different currencies, but one shared, grinding frustration: sending money across African borders is unnecessarily difficult. And it does not have to be.

Africa and its diverse remittance corridors

Africa is home to over 1.4 billion people and 54 countries, each with its own currency, banking infrastructure, and preferred way of transacting. In Ghana, mobile money dominates. In Nigeria, bank transfers are king. In South Africa, cards and formal banking lead the way. In Francophone West Africa, entirely different systems operate. This patchwork of payment ecosystems means that moving money between African countries is often harder, slower, and more expensive than sending it to Europe or North America.

The numbers are stark. Sending money within Africa costs an average of 8% in fees, among the highest remittance corridors in the world. Settlement times can stretch from days to weeks. Exchange rates are unfavourable, and the difference between the rate a sender sees and the rate a recipient actually receives is rarely explained. It is a system that consistently fails the very people it is supposed to serve: ordinary Africans trading with one another, supporting their families, and building businesses across borders.

Accrue’s solution: Cashramp, A stablecoin-powered agent network

The product at the heart of Accrue’s solution is Cashramp, a stablecoin-powered agent network now operating across eleven African countries. The concept is elegantly simple, even if the infrastructure behind it is anything but.

How Cashramp helps you, including users like Saliu, Jolie, and Johnson

A user in Ghana who wants to send money to Nigeria is linked up to a Cashramp agent, someone who can exchange their cedis, and the agent converts the funds into stablecoins, digital currencies pegged to stable assets at the prevailing market rate. Those stablecoins travel digitally to a Cashramp agent in Nigeria in seconds. The Nigerian agent converts them into naira and delivers the money directly into the recipient’s bank account or mobile wallet.

The whole process, from the moment a sender hands over cash to the moment a recipient gets their funds, takes less than five minutes.

Here is the number that changes everything for users like Saliu, Jolie, and Johnson: Accrue charges a flat $2 withdrawal fee for funds over $200.

Consider what that means in practice. If Johnson sends the equivalent of $100 to his family in Benin, he pays 1% of the funds, but once it exceeds $200, he pays a $2 flat fee. If Saliu pays a $500 to his kente supplier in Ghana, he pays $2. If Jolie sends $250 home to Cameroon, she pays $2 in fees. Compare that to the industry average of 8%, where a $200 transfer would cost $16 in fees alone! This difference is transformative and indeed, cost-effective.

For individuals sending money monthly to support families, those saved fees compound quickly. For small business owners like Saliu, where margins matter enormously and supplier relationships depend on timely payment, the ability to send money reliably and cheaply is not a convenience; it is a competitive advantage.

This is what financial ease that actually works for Africans looks like: fast, affordable, and honest about what it costs.

Africa’s intra-continental trade is worth hundreds of billions of dollars annually. The people driving that commerce, the Salius, the Jolies, the Johnsons, deserve a payments system that works as hard as they do. For too long, they have been forced to improvise: navigating broken banking systems, absorbing punishing fees, and taking risks that no one should have to take simply to move money from one African country to another.

Sign up and join hundreds of thousands of people sending and receiving money across Africa and the US, in less than 5 minutes.