You are reading Factsheet, our series of specific guides on experiencing and using technology platforms in Africa. Whether you are looking for knowledge on getting your African film on Netflix, raising a seed round or finishing an online design course, we are covering all that.

—

OPay’s payments product is supposedly growing. It has been responsible for more than 60% of mobile money transactions in Nigeria, according to the company.

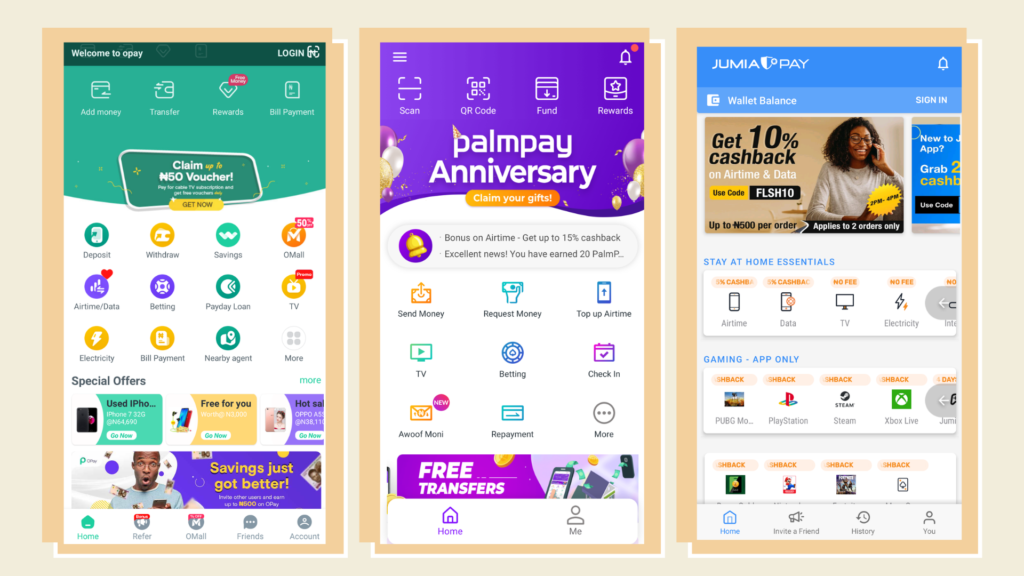

But OPay the super app is in hibernation, if not completely shut down. As of this publication, the app only supports savings, bill payments, loans and betting functionalities. OMall, the online shopping vertical, is active with some “50% off” deals.

Meanwhile in South Africa, Moya Messenger appears to be picking up steam.

Launched in 2018, the app does not cost users mobile data or airtime.

Moya’s foundational feature is instant messaging, with an interface similar to WhatsApp and Telegram. A ‘Discover’ button launches the user into a bunch of local and international news, health and educational features depending on your geographical location.

A user’s mobile data must be switched on to use these services for free. The app’s model relies on advertisers paying for users’ data.

The app has gone from about 200,000 monthly active users in March 2019 to more than 2 million this August, according to data shared by Gour Lentell, co-founder and CEO of biNu, the company behind the app.

Lentell says 24,000 users on average are signing up daily on Moya.

To be sure, the app is at a very rudimentary stage of super-app-ness compared to OPay’s ambitions. The latter had and still has services users would pay money for, making it a platform for enterprise not just for OPay but for a variety of third-party merchants – which is kind of the exciting point about super apps.

On the other hand, Moya’s present iteration seems to be part of a company’s broader campaign to provide data-free internet services for emerging market consumers.

There are other Africa-focused companies at different stages of the super app business, with varying potentials for success. We take a glance of the landscape to see what five of them have been up to in recent months.

MTN’s Ayoba

Susan Kayemba, senior manager for digital and online services at MTN Uganda, was excited to introduce Ayoba in the East African country in July.

“It has many features which are not available on other instant messaging apps,” Kayemba says.

Launched in March 2019 and currently available to only Android users, Ayoba is primarily an instant messaging app plus news readers and games. It works on multiple mobile networks but MTN users have free data every month (ranging from 1GB in Uganda to 600MB in Nigeria) to use the multimedia features – voice notes, video chats, etc.

MTN is promoting the app as a pan-African platform created by and for Africans. Djibril Ouattara, CEO of MTN Cote D’Ivoire, describes it as “a bit like the African WhatsApp adapted to local needs.”

Ugandans can use it in Swahili, Rwandans in Kinyarwanda and Ghanaians in Twi. 16 other languages are supported in addition to English, French and Portuguese.

MTN says there are half a million Nigerians on the app, but it is unclear how active these users are if the app’s main function – chat and news – are easily accessible and arguably more interactive on other platforms.

Also, half a million users represent 0.006% of its subscriber base in the country.

A puzzle about Ayoba is why it is a separate app from MTN’s other value adding products like Music+ and why there seems to be no integration for its 36 million mobile money users.

It appears bundling these is the eventual goal. Yolanda Cuba, MTN Group’s chief digital and fintech officer, says mobile commerce and interactive entertainment are in the pipeline.

Palmpay

They have stayed under the radar since we heard of their $40 million seed funding and a VISA partnership in November 2019. One promotional discount has followed another in the period since but the expected OPay-like push to rollout verticals has yet to materialise.

On the Palmpay app, banners commemorating their one-year anniversary are front and centre. But the features are mostly unchanged from November: send and request money, buy airtime, place bets.

They continue to emphasize “Palmpay points” but that hasn’t seemed to take off with users. 1 point = ₦1 which is no big deal.

However, they are not doing nothing. As TechCabal has reported, Palmpay has been pitching its app to merchants and businesses as a payments platform of choice.

The plan is to have the app pre-installed on 20 million units of Tecno, Infinix and itel phones – the most popular phone brands in Nigeria used by the SME segment being targeted with the app.

These low-cost phones are manufactured by Transsion Holdings, the Chinese company. (Palmpay is developed by Transsnet Financial, a joint-venture company of Transsion and NetEase Group, another Chinese internet tech company).

As of February, the app had 100,000 active users, according to the company.

Considering the integration with phones was a pre-COVID plan that has suffered setbacks due to production shortages in China in the first quarter of the year, it may be too soon to expect Palmpay to append any new features on its app, or announce something crazy exciting.

For the rest of the year, the company could lean into broadening appeal with consumers using commemorative giveaways on social media, with all of that splashy purpleness.

Safeboda

Safeboda went against the grain in Nigeria by launching its motorcycle-taxi outside of Lagos and it’s proved an inspired choice so far. They have completed 250,000 rides in five months since March. They are leading the bike-hailing wars.

Ibadan, where it launched in Nigeria, is Nigeria’s largest city and is underserved technology-wise relative to Lagos. They are relying on loyalty programs and creative personalised messaging to attract and retain customers, hoping they create a base to discourage any new entrants.

Founded in Uganda and also present in Kenya, Safeboda is on a visible path to being a super app, permeating its target markets one product at a time.

Food, shopping and package delivery are available on the app in both countries, in addition to the original digitized boda boda idea that lifted the company into the top bracket of Uganda’s startup ecosystem.

Safeboda has more than 1 million users across its three markets. We don’t know how many are active and they have to find solutions to check fraudulent schemes – like drivers registering with multiple accounts to ride themselves and get paid. But the company appears to have a steady stream of business and could become a contender in Africa’s super app race.

Gozem

The best known majority-francophone ride-hailing brand in Africa, Gozem has taken a few interesting steps to register its continental and inter-sectoral ambitions.

In May, it enabled a mobile money facility on the app in partnership with Etisalat Bénin (Moov). The mobile money is used in a digital wallet launched this year, adding another in-app payments feature that could be an easy port for other services.

On the strength of its ride-hailing drivers, Gozem began offering e-commerce delivery in Togo and Bénin in July. It may or may not have been a rollout induced by the urgency of COVID-19 but that’s one more product to enable CEO Emeka Ajene’s big plans.

He and co-founder Raphael Dana set out to build an Africa-focused super app from the company’s inception in 2018. With Ajene’s lessons from stints at Konga and Uber Nigeria, and Dana’s Singaporean upbringing, they hope to replicate the models operated by Grab and Indonesia-based Gojek.

It remains to be seen whether the francophone region can be a better take-off environment than West and East Africa.

JumiaPay

Has a change of brand name started reaping benefits?

JumiaOne was launched in 2018 as a lifestyle app for payments and shopping. It was to be the one-stop shop to “bring every online service in one place and make them easier.”

This shop now combines the features of Jumia Pay, created in 2016 and modeled after Alipay, with gaming, loans, insurance and investment to become an early-stage super app.

It has been one of the fastest-growing components in the Jumia portfolio over the past year.

2.3 million transactions worth $39 million were processed on JumiaPay in the first quarter of this year. Payment volumes rose 106% on the back of 2.4 million transactions in the second quarter.

With progressively better metrics, Jumia could become the continent’s breakout super app possibly buoyed by Jumia prime, its loyalty program.

But like other players on this list, Jumia will be looking over their shoulders for the approach of ambitious fintech companies like Paystack and Flutterwave, whose entry into e-commerce infrastructure space could accelerate and differentiate the super app race in Africa.